Write something

Pinned

3d •

⭐ cloudresidents.ai ⭐

What Is Cloud Residents AI, And What Is It Built On? Cloud Residents AI is an assistant built to answer your US credit card and banking questions from real, lived experience, not from a generic AI guess. It is built on: 135,000+ curated data points from nearly five years of real activity, from 2021 to 2026, refreshed monthly. That includes approvals, denials, reconsideration scripts, Financial Review survival stories, and step-by-step walkthroughs from people who already did this as non-residents, with an ITIN and no SSN. Every answer is built from real outcomes and real walkthroughs from people who already did it. So this is not another chatbot that guesses and invents. The intelligence you feel is the curated, cited, real-experience library behind it. Now In Public Beta For the last 3 weeks, this was quietly in private beta with a small group of you. Today, it opens to everyone at cloudresidents.ai, free to use. A real thank you to everyone who tested it in private beta and sent feedback, screenshots, and bug reports. You shaped this, and it is sharper because of you. How It Works Ask in your own words. Type or speak, in 19+ languages. It searches by meaning. Your question is matched against every one of the 135,000+ data points based on what you actually mean, not just keywords. It keeps only the best sources. Hundreds of matches are filtered down to the 10 to 20 most proven, most recent, and most relevant sources. It writes a cited answer. You get a clear, structured answer in your language, with a Sources panel behind every claim. Use Fast for quick answers. Use Pro for deeper, multi-step problems. What You Can Actually Ask This is where it gets useful. You can attach a file or screenshot and ask in plain language. For example: Attach a screenshot of your credit history and ask what to clean up before you apply. Attach your credit file or report and ask which card to try next for your profile. Attach a bank letter, denial, or 4506-T request and ask how to respond and clear it.

Poll

38 members have voted

2d •

Does it constitute tax fraud?

I am a Non-Resident Alien (NRA) currently holding accounts with IBKR and Charles Schwab; I have submitted Form W-8 and received Form 1042-S. I plan to use an ITIN to open a bank account, but since almost all banks require a U.S. address, I intend to use a service like Anytime Mailbox to address this. Does this mean the bank will view me as a resident rather than an NRA? Will the tax forms I receive for income—such as bank interest—be the same as those issued to U.S. residents? Does this result in me having a "dual" tax status with the IRS? Wouldn't this be illegal?

2d •

NY DMV-experience for Non-Driver ID application

Went to Manhattan Midtown DMV for the Standard Non-Driver ID. Was really smooth. Made an appointment a month before and already filled out the application online. When I went there my appointment barcode was scanned and I got a number. First I was called for taking the picture, second to go to the "real" counter. I had to give the application, the passport, I-94 admission number and my drivers license or two credit cards. After half an hour I was out of the building with an Interim Document in my hands. It really was as easy as it reads.

3d •

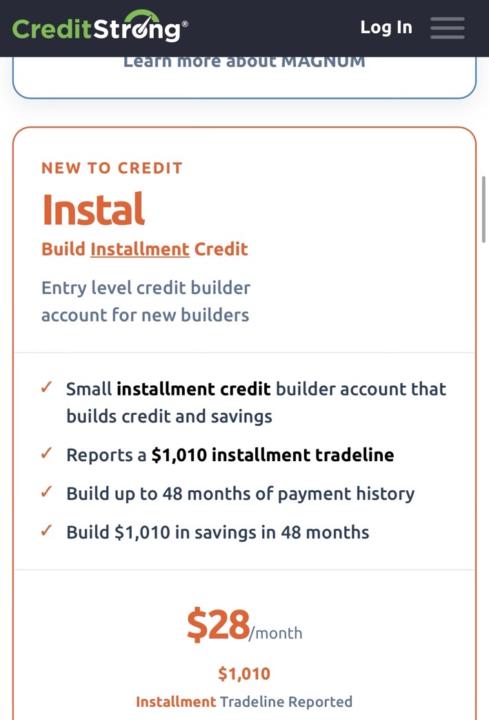

For those currently using CreditStrong, which plan did you choose and why?

I’m looking at: • Revolv ($15+/month)• Magnum ($16+/month)• Instal ($28/month) For those who have used any of these: - Which plan did you start with? - How long did it take to report to the bureaus? - Did you see a meaningful FICO score increase? - If you were starting over today, would you choose the same plan? I’m especially interested in feedback from ITIN holders and non-U.S. residents. I’m leaning toward Revolv because of the revolving tradeline, but I’d love to hear from people who compared it with Magnum or Instal. Thanks in advance for sharing your experience and data points!

Mar 25 •

Getting Amex is easy. Surviving Amex is the real game

Getting approved for Amex is easy. Staying with Amex… is the real game. --- A lot of people get their first Amex and stop there. They think: “I made it” --- But now your entire profile is: 1 card 1 bank 0 depth --- That’s exactly what makes you risky. --- Because from Amex’s side: There’s no comparison No external history No context --- So even normal behavior looks suspicious: - spending too fast - high utilization - mismatch with income --- And that’s how you get hit with Financial Review. --- Here’s what I personally recommend: **Before increasing spend on Amex, open at least ONE non-Amex tradeline** - Visa / Mastercard from another bank - a credit union account --- Then use Amex normally. --- This way: You’re not dependent You look more “real” And your profile has depth --- Don’t just get approved. Build a profile that doesn’t get questioned.

1-30 of 924

skool.com/itin

Helping non-US residents and business owners access US banking, credit cards, and ITIN - from anywhere.

Leaderboard (30-day)

1

+184

2

+178

3

+98

4

+96

5

+88

Powered by