Activity

Mon

Wed

Fri

Sun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Memberships

50 contributions to Cloud Residents · US Credit

15d •

Navy Fed Pledge Loan Approved on Second Attempt

Morning All! Further to my earlier post about my pledge loan going under review, NFCU requesting employment details and then declining the application, I decided to reapply last night after seeing several recent success stories. This time, I was approved. After a call to submit the new application, it remained pending for around three hours before the promissory note arrived. I think the original decline was probably a mixture of applying too early and some confusion around my residency. My ITIN was issued in February and delivered in March, with my first US credit card also opened then, so I had just one statement cycle showing on my credit file at the time. Original post: https://www.skool.com/itin/navy-fed-pledge-loan-under-review Thanks to everyone who helped

1 like • 8d

Awesome. Congrats @John Flack !!

May 7 •

How I Pulled All 3 Credit Bureau Reports Online using an ITIN

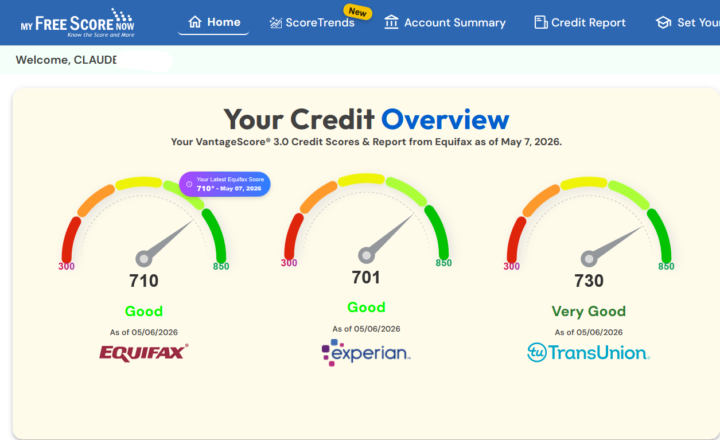

Just pulled my tri-bureau scores this week — actually. My ITIN was issued in December and my first CC with ITIN was 2 month ago in March. Quick note on the numbers: VantageScore 3.0, not FICO 8 or 9 (what most banks actually use). The underlying report is accurate; just a different scoring model. The point of pulling these is knowing where you stand at each bureau so you can apply with intent and avoid unnecessary denials. And being able to pull Experian and TU instantly online is a game changer. Here's the playbook that's actually worked for me: • MyFreeScoreNow — accepts ITIN, refreshes all 3 bureaus daily. Heads-up: $1 non-refundable activation fee for a 7-day trial, then it converts to paid if you don't cancel. Best single tool I've found even with the cost. • Nav.com — how I get my Experian report online with an ITIN (Experian.com doesn't accept ITIN at signup; their only direct route is calling for a paper report). • MyEquifax — pulls all 3, but only Equifax refreshes daily. Experian and TU update once a year there. Pro tip: if equifax.com rejects you online, message them on X — they sort it fast. - Some other tools that pulls Equifax report/score are: Tru, CreditKarma, MyFicoScore (Free plan) What doesn't work: MyFico's 2/3-bureau products (can't authenticate ITIN against Experian or TransUnion), and AnnualCreditReport.com online (mail-in only). Curious what others here are using — has anyone found a way to get Experian or TransUnion online without going through Nav, or MyFreeScoreNow?

0 likes • May 8

@Aaron Ng Yeah., I think @Ain - Cloud Resident documented the $1 process if you search. I personally wanted to test the other methods and see how far I could get

1 like • May 12

@Jonathan Mas I don't think AnnualCreditReport.com supports ITIN. Their FAQ recommends those with ITIN reach out to the Credit Bureau directly for their free credit report. https://www.annualcreditreport.com/generalQuestions.action

May 8 •

Navy Fed Pledge Loan - Under Review

I’m fairly new to Navy Federal and recently opened membership/checking/savings. I deposited funds into savings and applied for a small share pledge loan The application went under review, which I expected as I’m a new member. Navy then requested either an employment contract or a “letter from command”. Like a lot of us I’m self-employed/freelance, so I don’t have an employment contract, and I’m not military. I’m also very early in my US credit/banking journey, so I don’t have a long US income paper trail yet. I’ve replied saying: I am self-employed/freelance and do not have an employment contract or military letter from command. This is a share pledge loan secured by funds already held in my Navy Federal savings account. If employment documentation is still required, please let me know what alternative documentation is acceptable…. Has anyone else had Navy request employment documentation for a pledge loan? Any experience with this? 1. Am I just too early! 2. Am I best to just cancel the it down and reapply later 3. Does cancelling a pending pledge loan application cause any issue with Navy internally? Thanks all [Update here - https://www.skool.com/itin/navy-fed-pledge-loan-approved-on-second-attempt]

0 likes • May 9

following

May 7 •

Got into Navy Fed; what should I open with them?

I just got into Navy Federal. I'm wondering what I should open with them—like a pledge loan, secured card, business account, personal account, etc. If there's an area in the classroom on this, please let me know. I could do something like a $20,000 pledge loan if that will help me.

1 like • May 7

Speical Easy Start Certificate is a great idea!!

1 like • May 8

@Sable Rivers i believe you can leverage the 90 days while building the relationship with NFCU independently from a CC. Building a relationship with a bank (credit union) like dating. In a normal dating, you would show interest and give first before you make an ask. I would take it the same way. Use the 90 days of relationship to actual build the relationship before you make an ask for Credit.

May 7 •

Penfed Approval?

Has anyone got approved for penfed in the last 60-90 days? I got my penfed account a year ago and they asked for US ID. Thankfully I had a US Visa and they accepted the application with that. Now I have another friend that applied and they are asking again for US ID again and asking weird questions like "how many days did you live in the US last year". etc

0 likes • May 7

The "how many days did you live in the US last year" is more of an IRS question than a bank one. It is asked to determine the tax residency of the applicant. It's quite normal actually. Every banks I have applied to (physically (eg. Chase) or online, including PenFed) have asked that question in different format. And to answer your original question: Yes, I opened a PenFed account in the past 60 days with same day approval {I had to send them address + ID verification document}

1-10 of 50

@claude-t-9543

I'm Claude and am passionate about real estate and am here to learn and be with like minded-people

Active 5d ago

Joined Feb 7, 2026

Powered by