Pinned

26d •

🧠 Why NEAR’s Cross-Chain Architecture Crushes the Competition

Most blockchains force you to choose between massive hardware barriers or security risks. NEAR takes a different approach: it swaps heavy hardware for mathematically rigorous, dynamic cryptographic security. By securing a high-throughput internal state, NEAR unlocks the ultimate application layer: autonomous, cross-chain commerce. Here is exactly how it works, why it's a game-changer, and why it absolutely beats competitors like ThorChain and ICP. ⚡ The Power of "Intents" Instead of forcing users to execute a rigid, sequential path across bridges, NEAR relies on intents. What is an intent? A user signs an off-chain cryptographic instruction specifying a desired outcome (e.g., "Exchange exactly 100 USDC for 99 USDT"), rather than the exact technical route to get there. These intents are managed by the Intents.Near verifier contract, which acts as a trustless internal ledger. This allows cross-chain outcomes to settle without relying on centralized bridge custodians. 🔄 The 3-Phase Execution Flow By settling trades entirely within the internal state of a highly scalable ledger, users completely bypass the latency, security risks, and exorbitant gas fees of live cross-chain trading. The process breaks down into three distinct phases: 1. The Deposit Phase: Users lock supported assets into the verifier contract, which registers those balances onto its internal state ledger. The user's intent is then broadcast off-chain to a message bus. 2. The Atomic Execution Phase: Independent market makers (known as solvers) compete to provide the most efficient route and exchange rate. Once a match is found, the verifier contract validates signatures, ensures inputs/outputs match perfectly, and executes the trade atomically within its own internal state. 3. The Withdrawal Phase: The internal ledger balance is burned. The contract triggers a cross-contract call to a token bridge, delivering the native assets directly to the user on their destination chain. 🛠️ The Core Primitive: Additive Key Derivation + MPC

Pinned

Jul '25 •

Welcome to DeFi U!

Hello everyone and welcome. As we begin building out DeFi University together, please know that any ideas you may have for a new tool, a new live call, a new course, anything that you'd like to build or incorporate in to add more value for us, the community members, that is 100% a yes here. This community is AI first, which simply means that we learn together how to use AI tools to build what will generate more value for us, the community members. We hope to foster an environment of learning and growth in many different areas of life within our DeFi University community, and now with these new AI tools any suggestion that any member has which will add value can quickly be built out and incorporated in. It's a very exciting and transformative time that we live in. To foster a sense of community spirit, please introduce yourself in the general chat as you join, and share a bit about yourself so that we can all get to know one another better. Live calls in the community take place every day Monday through Friday and they are open to all members. See you on the next live call and in the DeFi U chats! -David

11d •

Polymarket drama

Anyone have thoughts on the latest Polymarket resolution drama? There seems to be a pattern of behavior here, can they continue to be successful with all these issues?

May 20 •

Independent AI agent?

Hello team, Have you guys seen this? An AI agent doing your investing for you? Alex Walch from UIG fame created an ai bot that does independent market and chart analysis and manages it's own portfolio, that generated over 10% profits in fees in two weeks, while suffering only mild IL? What do you guys think? https://youtu.be/HjuYTKK_9zw?is=1Sr9CUvKrfLUqJcw

Apr 2 •

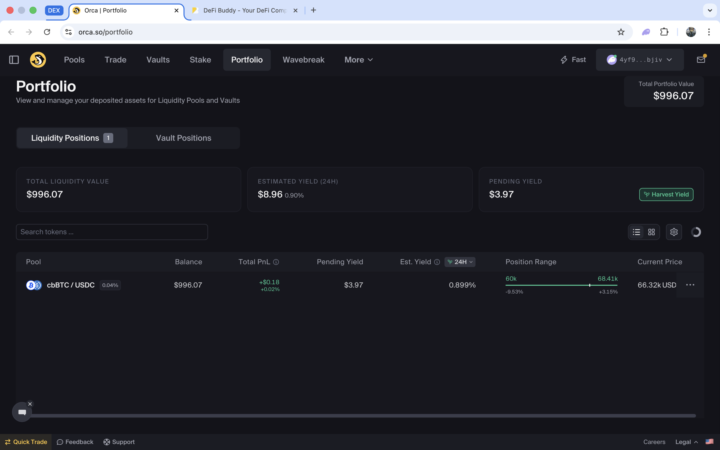

Public Portfolio

Yesterday, I started a Public Portfolio (no joke). I will show every step I make. I opened a single sided LP $1000 cbBTC/USDC and I will document every step on X.

1-30 of 495

skool.com/defiuniversity

Master DeFi from beginner to advanced. Security-first curriculum, live mentorship, gamified learning. Join us and build DeFi expertise safely.

Leaderboard (30-day)

1

+4

2

+2

3

+2

4

+1

5

+1

Powered by