Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Owned by Options

STOP trading market direction. Start using options strategies to turn volatility into steady income. We sell premium, and think in probabilities.

Memberships

AI Options Trading Lab

26 members • Free

Options Made Simple Webinar

1.4k members • Free

Options Auto Trader

578 members • Free

Trading 101: Stock Options

111 members • Free

Options Trader Network

8 members • $97/month

TRADING MADE SIMPLE by Ali

1k members • Free

OptionMasters

27 members • Free

Option4All

59 members • Free

Imperium Academy™

70.7k members • Free

16 contributions to PainlessTrader

7d •

I simulated TQQQ back to QQQ's 1999 launch

Many people here trade options on leveraged ETFs. I simulated TQQQ back to QQQ's inception in March 1999, with financing costs and the fund's expense ratio built into the model. Almost every leveraged ETF discussion eventually runs into assumption 3x daily leverage should produce something close to 3x the long-term return. The pre-2010 series models 3x daily exposure to QQQ, with financing costs on the borrowed notional and the fund's expense ratio subtracted daily. Starting in 2010, the simulated series is spliced directly into TQQQ's real, traded adjusted price history, so everything after that point comes from actual market data. The results, $10,000 invested in March 1999: - QQQ: $10,000 → $167,265 (11% annualized) - TQQQ (simulated pre-2010, real data after): $10,000 → $24,569 (3.4% annualized) Maximum drawdown over the same 27 years: - QQQ: -82.96% - TQQQ: -99.98% A -99.98% drawdown means every $10,000 fell to $2. TQQQ carried far more risk the entire way and still finished with $14,569 in total profit against QQQ's $157,265, under 10% of the unleveraged return. The volatility drag (beta slippage) scales with the square of the leverage multiple. So double the leverage and the drag roughly quadruples, triple it and the drag runs close to nine times larger. That is why I don't trade options on leveraged ETFs. You would be layering theta and IV risk on top of an instrument that is already decaying by design and has never been tested by the environment that would break it.

1

0

10d •

Using This Week's Earnings Volatility to Buy REITs for Retirement

Since 1991, REITs and the S&P 500 have delivered almost the same total return, but the engine was completely different. Most options traders never notice this. REITs are boring. Theta is not. I used this week's earnings-volatility spike to get paid extra for buying real estate at my price, instead of whatever price the market hands me on a random Wednesday. Active trading builds the war chest. Boring trades like this help build your net worth. You need both.

1

0

17d •

It's Just Sector Rotation

Hi, something happened over the last 24 hours that's such a clean example of rotation, I wanted to write it down while it's still fresh. Yesterday, money crowded into the biggest tech names in the market. The Nasdaq still closed red on the day, but the mega-cap tech ETF finished up close to 2%. Defensive sectors like healthcare and utilities actually lost ground. Even on a day that closed red, capital was clearly picking favorites inside the selloff. Then today flipped the entire script, Trump told NATO the ceasefire with Iran is over, oil jumped more than 6%, almost every sector turned red (except energy and consumer staples), even yesterday's tech winners gave it all back. That's rotation in its purest form: capital finding whatever feels safest at that exact moment, sitting there, and moving again the second the story changes. Anyone else watching this play out today? What you're doing differently because of it?

1

0

Jun 22 •

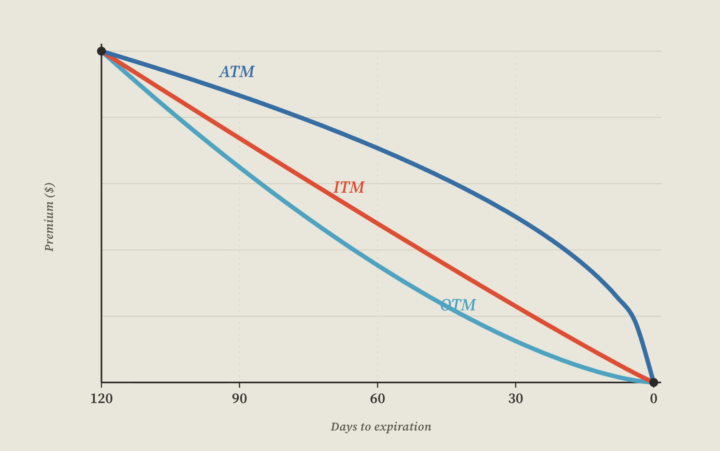

The "linear" theta line is a lie

I ran every strike through Black-Scholes this weekend. The output surprised me ($100 underlying, 20% IV, 4% rates): - ATM theta at 30 DTE: $4.36/day per contract - ATM theta at 1 DTE: $21.43/day per contract ATM decay accelerates into expiration. But OTM does the opposite. 5% OTM theta peaks at 21 DTE, then collapses, 10% OTM theta is essentially gone by 14 DTE. The closer you get to expiration, the slower OTM premium decays. The reason is gamma. Theta doesn't have its own engine. It borrows gamma's. Near expiration, gamma concentrates almost entirely at the money. OTM strikes lose gamma, so they lose theta too. Your OTM short that feels safe at 21 DTE has already peaked. Holding it to expiration isn't collecting more decay. It's carrying pennies in front of a steamroller. Theta is not magic income. It is rent for sitting on gamma risk.

1

0

Apr 2 •

SPY Risk-Free Butterfly

Hi, I did it again! If you follow, on March 23 I opened a SPY 640/620 put ratio spread for a $598 credit. Yesterday, I bought the 600 put for $4.77 and turned the entire position into a RISK-FREE butterfly. Now the trade has: - No downside risk - No upside risk - Locked-in profit: $121 - Max profit: $2,121 This is how short volatility works when we stop thinking directionally and start thinking in structures.

1

0

1-10 of 16

Active 7h ago

Joined Oct 27, 2025