Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

Volturon Trading Systems

247 members • Free

5 contributions to Volturon Trading Systems

Feb 13 •

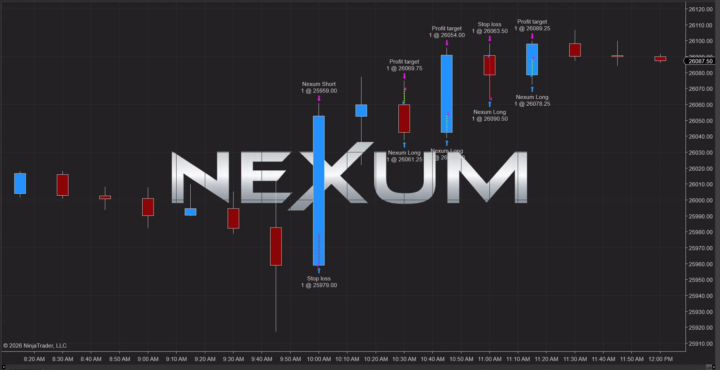

Post-Game 2-13-26

The March NQ contract opened soft around 24,842, quickly probed down to 24,579 (a ~1% dip) on lingering AI/tech rotation pressure from the prior session. The big catalyst was the 8:30 AM CPI print: - Headline CPI came in at +2.4% YoY (vs. +2.5% expected) and core at +2.5% (in line). - This was the softest headline reading in months and triggered an immediate relief bounce. NQ reversed sharply post-release, recovering most of the early losses and closing near 24,778 (+0.04% on the day) after swinging through a 417-point range. This kind of whipsaw action around high-impact data is exactly the environment where automated systems can get chopped: - Volturon’s two losses were textbook examples: the short at 10:00 AM EST (right on the Existing Home Sales release) got caught in the post-CPI momentum shift, and the long at 11:30 AM EST got stopped out during the subsequent consolidation/pullback. - The two wins likely captured the initial dip and one of the cleaner intraday swings, but the chop prevented a bigger net positive. - Nexum, with its more patient breakout/momentum filter, simply waited for confirmation and rode the cleaner recovery leg. No major surprises in the data itself—just the usual post-release volatility that tests edge robustness. Both algos stayed within risk parameters and avoided any outsized drawdowns, which is exactly what we designed them for. Quick note on next week: Monday is President’s Day, so U.S. equity and futures markets are closed (no NQ trading). This gives us a natural pause—perfect timing to run full diagnostics, review any parameter tweaks, and prep for Tuesday’s return with fresh eyes. The lighter holiday-shortened week should also mean lower volume overall, which can sometimes amplify the kind of chop we saw today, so we’ll keep that in mind.

1 like • Feb 13

Weird, because that first trade was a winner for me on Volturon.

Feb 13 •

Pre-Market 2-13-26

The E-mini Nasdaq-100 futures (NQ) for the March 2026 contract are trading lower this morning as of around 8:15 AM EST on February 13, 2026. The current price stands at approximately 24,725.25, reflecting a decline of 42.75 points or -0.17% from the previous close of 24,768.00. Today's open was at 24,842.25, with a session high of 24,864.75 and a low of 24,624.00. Volume is building at around 120,000-130,000 contracts, showing decent pre-open interest amid data anticipation. Broader futures are muted to soft, with Nasdaq 100 E-minis down ~0.3% in early indications. From a technical perspective, NQ exhibits a **Strong Sell** overall summary. Moving averages signal Strong Sell (0 Buy vs. 12 Sell), while technical indicators also lean heavily Sell (0-1 Buy, 0-1 Neutral, 7 Sell). Key indicators include an RSI(14) in neutral-to-sell territory, MACD with sell signals, ADX indicating moderate trend strength, and overbought conditions on some oscillators that could prompt short-term bounces but reinforce downside if supports fail. Pivot points for intraday trading feature a classic pivot near 24,750-24,780, with resistance at approximately 24,850-24,900 (R1/R2) and support at 24,650-24,600 (S1/S2). The bearish alignment from breakdowns below key averages suggests vulnerability, though today's high-impact data could override. Market sentiment is cautious to bearish for Nasdaq futures, extending Thursday's AI-stoked selloff (Nasdaq Composite down ~2%, S&P 500 -1.6%) as worries over tech displacement and high AI capex ripple into software, finance, and related sectors. Broader indices are mixed-to-lower premarket (Dow/S&P futures down ~0.2%), with rotation out of growth into value persisting. Global cues are steady but risk-off, with focus on U.S. inflation for Fed clues amid resilient growth and tempered rate-cut bets (March hold now ~90% priced in). Incorporating Fed speakers' announcements: Today features Federal Reserve Governor Stephen Miran speaking at 5:05 PM ET on "Regulations, the Supply Side, and Monetary Policy" (following recent comments downplaying inflation risks and advocating for cuts). This could provide late-session color on policy but is unlikely to dominate amid CPI focus.

1 like • Feb 13

Is there a way I can do 5 contracts with MNQ instead of 1 for Volturon?

0 likes • Feb 13

@Steven J. Hendriks perfect, thanks!!!

Feb 3 •

NEXUM Slippage Adjustment Feature

We've added a slippage adjustment feature to Nexum. It is an optional upgrade if you wish to download it. Go here for the download

0 likes • Feb 3

Ok, thanks

1 like • Feb 3

Also, we have a red folder news tomorrow that starts at the same time as the Nexum strategy. Do you recommend using the strategy during days like this?

Jan 27 •

1-27-26

We didn't go in live because of the FOMC meeting today and tomorrow, but we did sim trade. The very first trade took a wrong turn, and Nexum ended up flat after 5 trades. Volturon faired no better. It was no surprise though. FOMC days are notoriously tricky, which is why we don't trade live on those days. The Fed isn't expected to lower interest rates, but who knows? We'll know tomorrow afternoon..

1 like • Jan 27

I also ran Nexum on a Sim account, but it only took the first losing trade. No other trades were executed.

1 like • Jan 27

@Steven J. Hendriks Ok, makes sense. Pretty cool feature 🔥

Jan 26 •

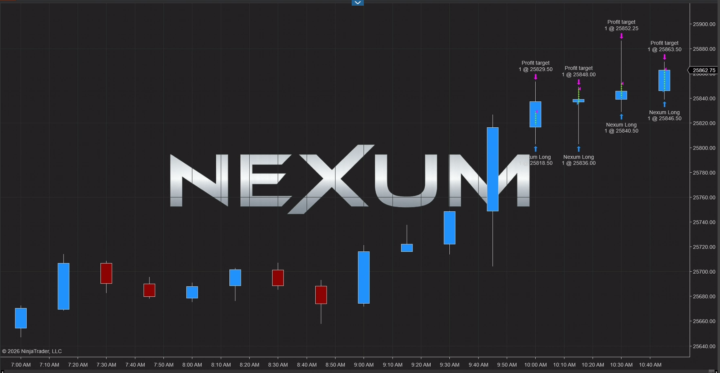

Short morning for Nexum

Nexum won handily ($1000 in emini ($100 in micro) per contract) in its first 4 trades. Volturon hasn't taken a trade yet, so we'll keep you posted.

0 likes • Jan 26

What is your usual daily loss limit with Volturon?

0 likes • Jan 27

@Steven J. Hendriks Perfect. And which timeframe do you use for Nexum?

1-5 of 5

Active 60d ago

Joined Jan 26, 2026