Activity

Mon

Wed

Fri

Sun

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

What is this?

Less

More

Memberships

6 Figure Funder Bootcamp

1.7k members • Free

TF

The Funding Mastermind

150 members • Free

THE ALIST WAY CREDIT GROUP

933 members • Free

Tradeline Secrets

2.3k members • Free

3 contributions to Tradeline Secrets

11d •

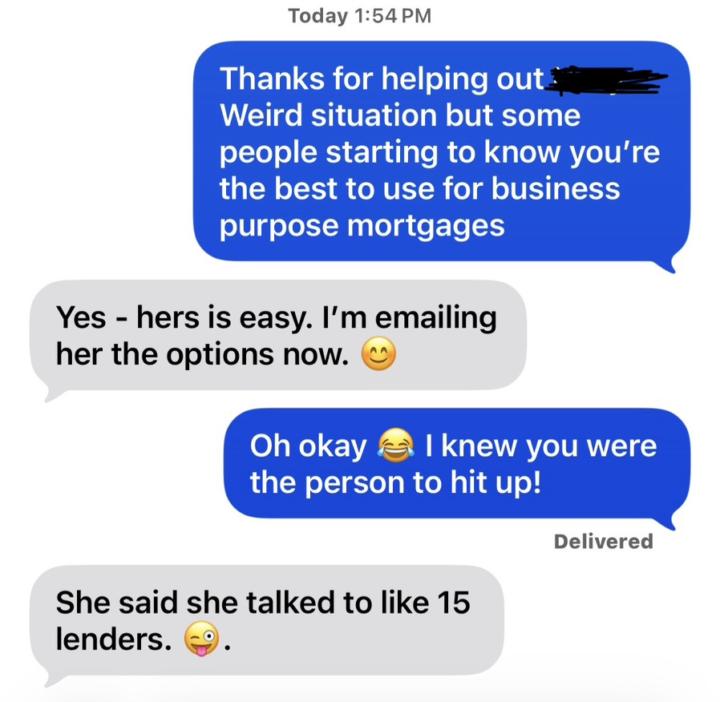

Everyone is a lender/broker these days

Very few can actually get it done. I get it done...we get it done. She owns her home free and clear. No mortgage. Clean title. But there's a co-owner on the deed that wants to sell. She doesn't. And if she can't buy them out, she loses the property. She talked to 15 different lenders. 15. Not one had a solution. We figured it out in a single text message introduction. Business purpose mortgage on the free and clear property. Pulls the equity out. Uses it to buy out the co-owner. She keeps the property. Then we flip the whole thing into an income producing asset. The area she's in does $10K+ per week on Airbnb. So we didn't just save the property. We turned a problem into a cash flowing machine. That's the difference between someone who knows products and someone who actually knows funding. Most people calling themselves lenders and brokers out here are just order takers with a license.

1 like • 11d

@David Ramirez Amazing!

11d •

If you've ever looked into "startup funding" online

You've probably seen gurus charging thousands to teach you how to get funded. Here's the truth: it's just business credit card stacking. By rotating bureaus and avoiding shared underwriters, you stack approvals without triggering denials. Real example: 3 banks pulling Experian, 3 pulling TransUnion, 3 pulling Equifax 9 potential approvals in 30 days. That's how you hit $50K–$150K at 0% or low interest without tax returns, financials, or collateral. Where most people mess up: They apply at banks that share the same underwriter (like Elan Financial). When that happens, all those banks see your prior applications and deny you. Or they burn through inquiries without a plan and tank their approval odds. The smarter play: Target regional banks and credit unions. They're more flexible, easier to work with, and you can actually talk to underwriters if needed. Use a bank call script to gather intel before applying. Know the bureau, the underwriter, and the approval limits before you pull the trigger. Then execute in sequence.

2 likes • 11d

Thanks for the intel I appreciate you for sharing.

25d •

🚨 THE UNO GLITCH 🚨

One hard pull. Five business cards. Run it till they tell you no. There's a major bank that lets you run this play Get approved, apply again. Pending, you wait. Approved, you run it back. You keep going until they cut you off or you pull all five cards off ONE inquiry. Low end — $30,000. One bank. One pull. High end — $150,000. One bank. One pull. And that's just ONE bank on the stack. Most people don't even know this exists. The ones who do stop at one card anyway. The bank, the card order, the profile requirements, and the full execution are inside VIP. You already know the play exists. Now you just gotta decide if you want in on the how. 🐋

3 likes • 25d

Hi David, I would love to learn more about the UNO Glitch.

1-3 of 3

Online now

Joined Dec 25, 2025

Powered by