Feb 11 •

📊 Underwriting Tip: Cash-on-Cash Isn’t One Number, It’s Two

Too many investors calculate cash-on-cash (CoC) once and call it a day. That’s how deals get misunderstood. You should always run both: 🔹 Current Cash-on-Cash This shows what the property is doing right now. Formula: Annual Cash Flow ÷ Total Cash Invested Use: • Current rents • Current expenses • Current debt terms This answers: “What am I getting paid today?” 🔹 Pro Forma Cash-on-Cash This shows what the property can do after execution. Use: • Market rents (not wishful rents) • Stabilized expenses • Renovation + refi assumptions This answers: “What does this become if the plan works?” ⚠️ Pro Tip: If the current CoC is negative or razor thin, your pro forma better be realistic — not optimistic. Cash-on-cash exposes weak assumptions fast. 💡 Smart investors buy on current performance and improve toward the pro forma, not the other way around. 👉 Want to get sharper at this? Join the ProSphere Skool community where we break these numbers down step-by-step with real deals, not theory. www.skool.com/prosphere-1303 ☕📈 Learn it. Underwrite it. Execute it.

Feb 7 •

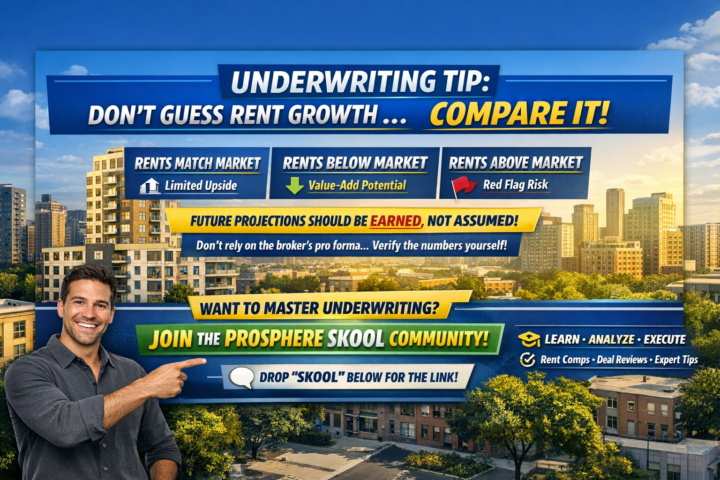

📊 Underwriting Tip: Don’t Guess Rent Growth, Compare It

When reviewing a deal, always compare market rents to the current rent roll. Here’s what you’re looking for: 🔍 Rents Match Market ➡️ Limited upside. Deal must work as-is. 📉 Rents Below Market ➡️ Potential value-add. Validate why they’re low (management, condition, lease terms). 📈 Rents Above Market ➡️ Red flag 🚩Future projections may be inflated or unsustainable. 💡 Pro Tip: Future projections should be earned, not assumed. If the rent roll doesn’t support market claims, your underwriting should reflect reality—not the broker’s pro forma. 👇 Want to sharpen this skill and underwrite with confidence? Join our ProSphere Skool Community where we break down real deals, rent comps, and underwriting frameworks step by step. www.skool.com/prosphere-1303

0

0

Jan 28 •

📊 ProSphere Underwriting Tip: Always Stress Test with the 50% Rule

One of the smartest ways to review a T-12 (trailing 12 months of income & expenses) is to compare it against the 50% expense rule. 🔍 Here’s how pros do it: Take the gross rental income and assume: 👉 50% goes to operating expenses (taxes, insurance, repairs, management, vacancy, utilities, CapEx, etc.) Then compare it to what the T-12 actually shows. ✅ If T-12 expenses are LOWER than 50% → great, but still underwrite at 50% for safety ⚠️ If T-12 expenses are HIGHER than 50% → dig deeper (there may be deferred maintenance, poor management, or rising costs) 💡 Why always use the 50% rule? Because it protects you from: • Overly optimistic seller numbers • Unexpected repairs & vacancies • Cash flow surprises after closing Smart investors underwrite conservatively — profits come from the margin of safety. 📈 Want to learn how to analyze deals like a pro? Join the ProSphere Community where we break down real deals step-by-step. www.skool.com/prosphere-1303

0

0

Jan 16 •

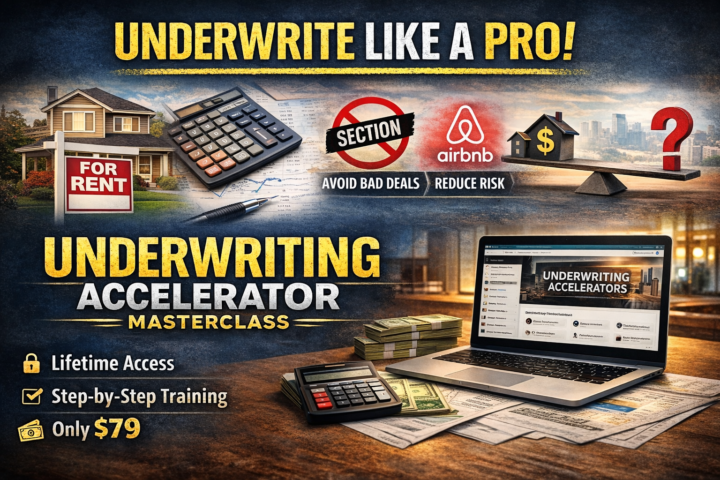

🔍 Underwriting Tip: Always Run the Numbers as a Long-Term Rental First

When underwriting a deal, always start with long-term rental (LTR) numbers…every time! 🚫 Never base your deal on: • Section 8 rents • Airbnb / short-term rental projections • Best-case or “pro forma” rent assumptions Why this matters 👇 ✅ LTR is the baseline reality It’s the most stable, lender-accepted, and market-tested income source. ✅ Protect your exit strategies Regulations change. Markets shift. Airbnb and Section 8 can vanish. LTR demand stays. ✅ True risk exposure Short-term and Section 8 numbers often mask vacancy, regulation, and management risk. 🧠 The Pro Rule If it doesn’t cash flow as a long-term rental, it’s not a deal, it’s a gamble. Once it works as an LTR, then you can layer in: ✔️ Section 8 ✔️ Airbnb ✔️ Mid-term or furnished rentals

0

0

Jan 12 •

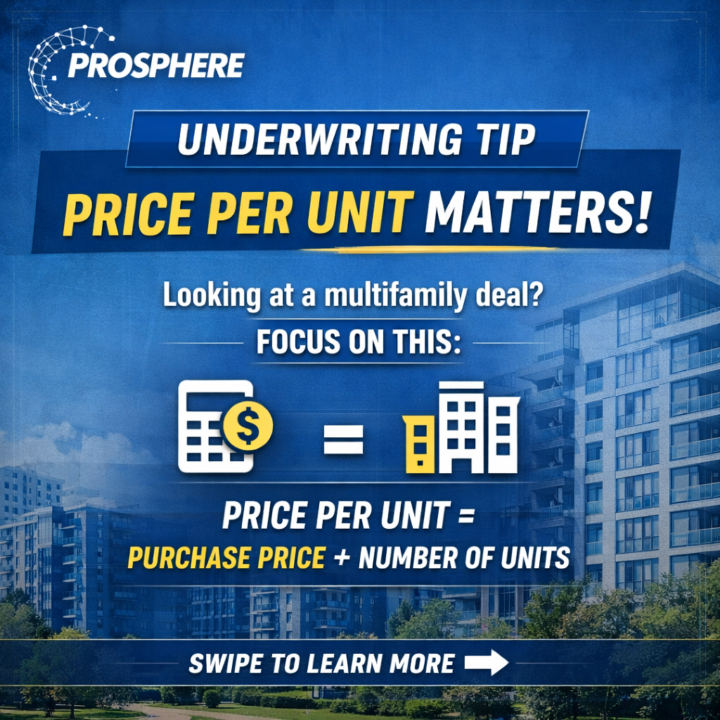

📊 Underwriting Tip: Price Per Unit (PPU) Matters More Than You Think

When analyzing a multifamily deal, don’t just focus on the purchase price, break it down to price per unit. 👉 Price Per Unit = Purchase Price ÷ Number of Units Why it matters: • It lets you quickly compare deals apples-to-apples • Helps you spot overpriced assets in “hot” markets • Reveals upside when rents don’t justify the seller’s ask • Keeps emotions out of the deal and numbers in control 💡 Pro Tip: If the PPU is higher than similar properties but rents aren’t stronger, the deal is already telling you something — your exit may be capped before you even buy. Smart investors buy the numbers, not the story. If you want to learn how to underwrite deals like a pro and spot pricing red flags fast, join our ProSphere Skool Community and check out the Underwriting Accelerator Masterclass 🚀 www.linktree.com/prospheremo 📌 Numbers don’t lie. Sellers sometimes do.

0

0

1-17 of 17

powered by

skool.com/prosphere-1303

Learn real estate investing with simple, practical lessons that build confidence, connections, and long-term wealth.

Suggested communities

Powered by