Activity

Mon

Wed

Fri

Sun

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

What is this?

Less

More

Memberships

Think Outside the Cell Comm.

143 members • Free

20 contributions to Think Outside the Cell Comm.

15d •

Yesterday in Chelsea, something powerful happened.

Our monthly Think Outside the Cell Community Meetup brought together growth-minded leaders — and what made it especially meaningful was the presence of two strong women, Cherri B and Marie, who added depth, insight, and powerful energy to the room. We need more of that. We need more justice-impacted women stepping into spaces where money is discussed openly. Where mindset is sharpened. Where ownership replaces limitation. Several of us sat around the table and played Cashflow, the financial literacy game created by Robert Kiyosaki — and let me tell you, it sparked conversations that went far beyond dice and game cards. It sparked: - Conversations about escaping survival mode - Conversations about investing instead of reacting - Conversations about how we build wealth differently This is what the Think Outside the Cell Community is about. Not just talking about money — but experiencing it, understanding it, and reshaping our relationship with it. And here’s what’s next: 📅 Saturday, March 20, 2026🕐 1:00 PM We’ve got lots of special activities planned over the course of the year: a boat ride, picnic, bowling, talent show, and more. All while living the Think Outside the Cell lifestyle. If you’ve been watching from the sidelines, it’s time to step in. If you’re a justice-impacted woman looking for a space to grow, you belong here. This community is rising — and you’re invited to rise with it. Stay tuned for details.

1 like • 14d

I can only imagine the energy that was in the room. This is a great place to be I’m sure to be in attendance at another meet-up in the future.

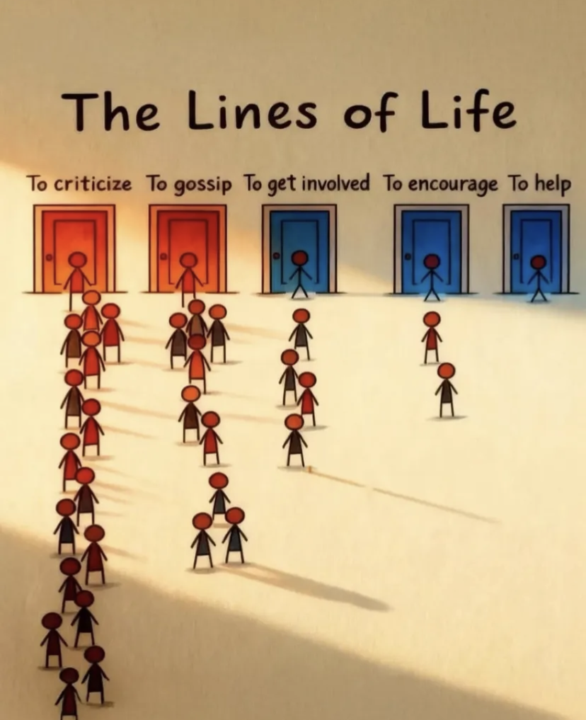

19d •

Sometimes pictures can speak louder than words

Over the next few days I’m going to share some pictures with the community and I really would like to get some feedback on what the picture means to you financially and/or otherwise.

1 like • 19d

To me The Lines Of Life represents me at different stages of my life. I use to be quick to criticize other people’s financial situation until I got responsible about my own finances. Now that I’m financially intentional with my finances I like To Help those that are willing to learn. The second picture represents to me a poor person mindset it’s easy to blame our problems on others like the Government and/or the rich and wealthy instead of releasing the rich and wealthy from within us.

29d •

My brother’s(sister) keeper

Just thought I’d share this as a reminder of what I’ve learned from participating in the SSI method finance class: - Portfolio diversification is a key to long-term investment success. (This is important to me because it helps to protect my principal) - A well-diversified portfolio includes a mix of stocks, bonds, and potentially, alternative investments across various sectors, company sizes, and geographic regions.(I must do this because I don’t like talking financial losses) - The right asset allocation depends on your individual risk tolerance, time horizon, and financial goals.(This helps me to make my decisions based on my goals instead of just focusing on numbers) - Mutual funds and ETFs (exchange-traded funds) offer ways to achieve the benefits of portfolio diversification.(As a beginner investor I find this to be the best approach for me) - Regular portfolio rebalancing is crucial to maintaining a diversified portfolio over time.(When I get to this point I’ll have some understanding of what to do because I’ll have some experience on my side) Like Joe Robinson always say in the SSI method we have to focus on our Investment strategy.

Jan 27 •

New to the community!

Hello. My name is Tamika. I live in Washington, DC and a mom of twins. I’m here to get financially educated and become more smart with my money and credit. I look forward to learning from you all. Life is a journey, always learning. I never want to be the smartest person in the room and I look forward to learning!☺️

1 like • 29d

Great place to start your financial journey

Jan 29 •

Identity Comes First

Before you build wealth, you build a self-image. Most of us were taught to see money as something we survive, fear, or react to. That shapes how we move. If you see yourself as “bad with money,” you’ll avoid it, or waste it. If you see yourself as “just getting by,” you’ll make decisions that keep you there. An ownership mindset starts with a different identity: I am someone who plans. I am someone who learns. I am someone who builds. When you change how you see yourself, your behavior follows. Budgets stop feeling like punishment. Saving becomes protection. Investing becomes a vote for your future. You don’t become disciplined and then change your indentity. You change your identity—and discipline grows naturally. This is the work: Not just learning what to do with money, but becoming the kind of person who does it.

1 like • Jan 30

This money mindset that you’re referencing I like to think of as a financial pillar.

1-10 of 20

Active 5d ago

Joined Aug 31, 2025

Powered by