Activity

Mon

Wed

Fri

Sun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Memberships

NextGen AI

42.9k members • Free

Cloud Residents · US Credit

1k members • Free

AI Automation Made Easy

18.9k members • Free

Modelify Academy Starter(Free)

1.1k members • Free

AB Free Dropshipping Course

2.3k members • Free

Project 8

263 members • Free

Mojo Mastery Challenge

1k members • Free

Mojo Dojo

4k members • Free

16 contributions to Cloud Residents · US Credit

25d •

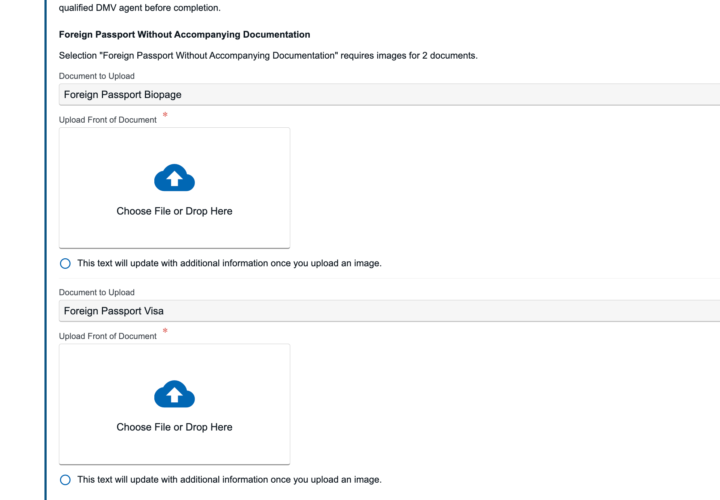

🚨 DMV New York Non-Driver ID – Problem with Documents

I'm planning to make NON driver ID and have problem during filling the pre screening form with verification process. I have two possible ways to qualify for a New York Non-Driver ID and I would appreciate some clarification. Option 1:My documents were pre-approved and I reached the required 6 points using: - Foreign Driver License (4 points) - Bank Statement (1 point) - ITIN document (1 point) The issue is that I never received my ITIN letter in original paper form. I only have a scanned PDF copy. I understand that the standard email says original documents are required. My questions are: - Will a printed copy of my ITIN letter definitely be rejected? - Do DMV employees have any way to verify the ITIN directly through their systems? - Has anyone successfully used a printed copy instead of the original IRS letter? I will only be in New York for one day and do not have enough time to request a replacement ITIN letter from the IRS by mail. Would an IRS local office be able to certify my copy or provide another official document confirming my ITIN that DMV would accept? Option 2:I also tried using: - Foreign Passport Without Accompanying Documentation - Foreign Driver License - My understanding was that this option does not require any visa documents. However, at the final document review stage, the system requires me to upload a Passport, Driver License, and Visa. I will enter the U.S. under ESTA (Visa Waiver Program) and do not have a visa in my passport. Is this a mistake in the online form, or is there another document that ESTA travelers are expected to provide? Previously I tried uploading my ESTA authorization and it was rejected. Would this document combination be accepted during an in-person DMV appointment without visa even the form saying at the last step is needed?

1 like • 21d

@John Flack I'm wondering if they would accept just Credit Card, in ID-44 form Credit Card is showing as 1 point but there is no Credit Card option in pre-screening form... Tried to call them but everytime I'm getting disconnected as soon as they say Hello, weird. On the chat support they can't answer my question.

May 15 •

DMV experience State ID card

Hello all, The past week I travelled to the USA, to open my bank accounts and get my state ID as well. Out of everything I had to do during the trip. This was the most unnecessary and stressful part. I had two addresses that I was thinking of using. A friends address and a paid residential address. (I ended up using my friends address just for the ID, and the paid address for all the banks) Since my friend agreed on a late notice, they could not add me to any utility bill or anything. So, for his house I had a lease agreement that was made from a website and renters insurance. For the paid address I had a lease agreement and a utility bill. I went to the DMV and asked them to apply for the Identification Card. After waiting in a painfully long queue, I was asked to proceed to the desk and to provide two proofs of address. I gave my lease and renters insurance and they said that only the lease is accepted because renters insurance is not accepted. So, she turned me away and asked me to go get a SSN ineligibility letter from the Social Security Administration. I went there and asked for the paper to be printed and also stamped just in case with my friends address. When I went back to the DMV, they accepted the renters insurance but not the lease because there was a clause in the lease that said "The term of the Lease is a periodic tenancy commencing at 12:00 noon on March 10, 2026 and continuing on a year-to-year basis until the Landlord or the Tenant terminates the tenancy." and they told me that the lease needs to have a specific start and end date so now the lease agreement is dismissed and can not be used as proof. They wanted to turn me away and told me multiple times that the documents are not sufficient but I stayed persistent and told them that the SSN ineligibility letter and the renters insurance count as two different proofs. They were still not happy and asked for my renters insurance declarations. On the spot I went to the contact page on the website asked for help from the renters insurance policy declarations only to find out that I had already printed it and she was looking at it the whole time. Then when she saw my ITIN letter, she was very confused as she could not understand why I do not have a SSN. She was constantly moving from her desk going to ask her colleagues which were not very helpful and friendly either. And finally she could not understand how the ITIN letter had a foreign address on it. So, I recommend for the people that do not have applied for the ITIN yet and want to use a friends address, to send the document to your friends house as it will be one more document you can use to the DMV if you want to apply for an ID. After a lot of back and forth she finally made the application and I got the license 10 minutes after we finished. The whole process of her trying to fill in my details and asking me for more and more proof of addresses took 3 hours!

0 likes • 25d

@John Flack the live chat is on dmv.ny.gov

0 likes • 25d

@John Flack I just write the post with my questions since 3 of my pre screenings was rejected and one approved but I dont have original ITIN document just printed scan, can you take a look?

May 14 •

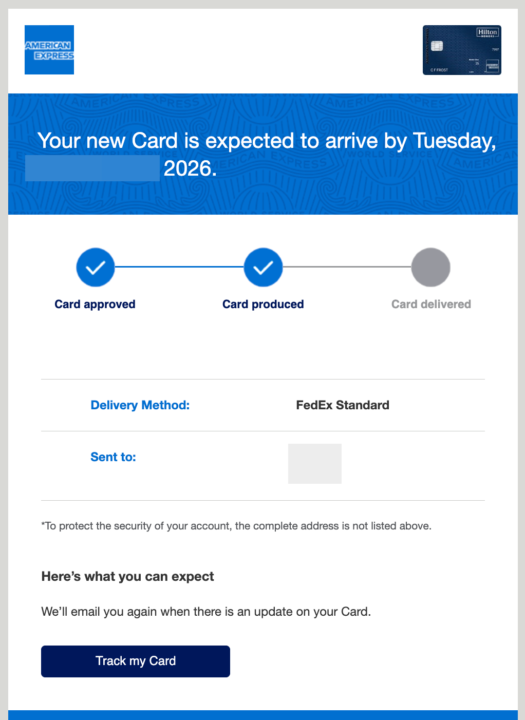

✅ AMEX Hilton Aspire - Approved. My Second Amex.

Got approval for my third credit card (and my second AMEX card) - AMEX Hilton Aspire - the most prestige Hilton Credit Card, new ITIN, applied as a non resident - online from outside of US with US proxy. History: 1) First try — auto rejection Reason: history with Amex is too short. 2) Tried again 8 days later It was one day after I received my first statement from my AMEX Gold. This time it went to manual review and they asked me to call them. The first question from the rep was: “Where do you want the card to be sent?” So I was like: wow, it’s already approved. But then the rep said I need to send documents: passport and ITIN. After the weekend someone will review them. I had some problem uploading documents, so I called Amex again and asked what I should do. This second person helped me to upload them and actually reviewed my docs while I was on the phone and said I also need to send address confirmation. I asked if he can wait on the phone while I upload it. He said yes. I uploaded it, he checked the document, and then said: “Congratulations, your card is approved.” Approved with 150k Hilton Honors bonus points.

1 like • May 14

@Philipp Hugentobler I have mailing addres in US, and then they forward it to me.

0 likes • May 15

@Dave N thanks!

May 7 •

NY Application for Non-Driver ID

Soon I will be in the US again and gonna have plans to go to the NY DMV and apply for a Non-Driver ID. I will be on ESTA. What I read here, it is quite easy and if you go with a standard, then you don't even need proof of address. Anyway there is also the option to go for REAL ID with proof of address. What I found is following: What does "TEMPORARY VISITOR" mean? A Temporary Visitor is defined as anyone who is not immigrating to or not permanently residing (living) in the United States. These visitors have US Department of Homeland Security (DHS) documentation that supports their legal status in this country. If you have DHS documents that identify you as a Temporary Visitor and have a REAL ID; your New York State driver license, permit or non-driver ID card will have: - "TEMPORARY VISITOR" on it - Your DHS document expiration date Please note that your DMV document does not expire on the Temporary Visitor expiration date, nor will your privilege to drive in New York. https://dmv.ny.gov/driver-license/resources-for-non-us-citizens It just says temporary visitor on the REAL ID thing, not for the standard. Does someone have a standard Non-Driver ID and can confirm it also has temporary visitor flag?

1 like • May 8

i'm planning to do the same thing within few weeks

1 like • May 14

@Ain - Cloud Resident are you sure? from what I remember there is an option to provide mailing address for delivery of the card.

May 6 •

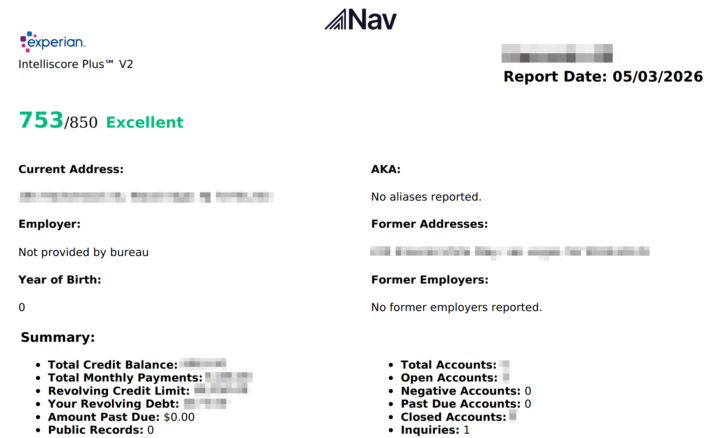

Experian Credit Score With Your ITIN (via Nav)

Most ITIN holders assume they can't see their Experian credit file online without a Social Security Number. You can. Sometimes. Shoutout to @momo for surfacing this method here first. Here's the updated standalone guide. Go to Nav.com, sign up for the free plan. You'll enter your name, DOB, address, and ITIN. Nav runs an Experian soft pull for identity verification and you're in immediately. If not, you can always retry. Once you're in, here's what Nav shows you: - VantageScore 3.0 from Experian - Score Factors - Payment History - Debt Usage - Credit Age - Account Mix - Debt vs Income - Hard Inquiries count - Current Address - Former Addresses Debt Usage drill-down: revolving credit limit, usage percentage, total revolving debt. Account Mix drill-down: split into mortgage, auto, revolving, and other accounts. Inquiries drill-down: total inquiries vs how many actually impact your score. Summary page: date of your first credit account, total balance across all accounts, total minimum monthly payments. Downloadable full report in PDF. This is genuinely useful if you're building US credit remotely and want to see where Experian has you — especially before applying for new cards. Now the caveats, because this matters. Nav's ITIN access for Experian is hit or miss. Some get through on the first try. Others don't, no matter what. If Nav doesn't work for you, alternatives exist: - Experian credit report by mail - Experian through Equifax Complete Premier - Experian FICO 9 through the Bilt app One more thing: VantageScore is not FICO. Almost all lenders pull FICO models when you apply. Nav's VantageScore 3.0 is directionally accurate, but don't treat a 720 VantageScore as a guarantee you'll get approved. Use it to track trends, not to predict underwriting decisions. If you try Nav with your ITIN - drop a comment below.

Poll

42 members have voted

0 likes • May 6

didn't work for me 2 errors: We are currently experiencing a connectivity issue with Experian. If you are trying to view an Experian report, please try again later. filling ITIN in SSN field didn't work.

0 likes • May 7

@Ain - Cloud Resident 9 months currently

1-10 of 16

Active 8h ago

Joined Mar 23, 2026

Bangkok / Medellin / Miami

Powered by