Activity

Mon

Wed

Fri

Sun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Memberships

Living in Thailand

31 members • Free

Auswandern nach Paraguay

204 members • Free

American Leverage™

6.3k members • Free

Meilenweit Voraus Basic ⭐️

4.4k members • Free

US Kreditkarten Talk

211 members • Free

Cloud Residents · US Credit

1k members • Free

39 contributions to Cloud Residents · US Credit

3d •

NY DMV-experience for Non-Driver ID application

Went to Manhattan Midtown DMV for the Standard Non-Driver ID. Was really smooth. Made an appointment a month before and already filled out the application online. When I went there my appointment barcode was scanned and I got a number. First I was called for taking the picture, second to go to the "real" counter. I had to give the application, the passport, I-94 admission number and my drivers license or two credit cards. After half an hour I was out of the building with an Interim Document in my hands. It really was as easy as it reads.

1 like • 18h

@John Flack My usual forwarder as mailing address and the New York address for the state ID. I mean they still offer pick-up

1 like • 18h

@John Flack Sounds like a plan. For me it was just unfortunate that they announced the flat fee one or two days before I went to the appointment. Wasn't able to arrange sth new. But yeah, it was just 13.50 USD or so and I can reapply for a new one with a new address in NY when I apply for a new credit card. Currently I let my file age.

May 27 •

Citi Custom Cash May Stop Accepting Applications

Reddit is buzzing with screenshots suggesting Citi will stop accepting new applications for the Custom Cash card as early as tomorrow, May 28. If the rumor holds, current cardholders keep their cards and benefits. No changes there. The only thing going away is the ability to apply for a new one. For anyone who's been researching this card and already knows it fits their setup, the next 24 hours might be your last window to grab it. Here's what the Custom Cash actually does: - 5% cash back on your top spending category each billing cycle - You don't pick categories manually - Citi automatically applies it to your highest spend category that month - Capped at $500 in spend per cycle, which comes out to $25 maximum cash back per month - No annual fee It's not a heavy hitter. It's a no-annual-fee workhorse that quietly earns 5% in one category each month. Solid for gas, groceries, dining, or whatever your real recurring spend looks like. For Cloud Residents: Citi has been one of the more consistent issuers for ITIN applicants. If the Custom Cash was on your roadmap as an early card or a category filler, this rumor changes your timeline. A few things to keep in mind: • $25/month cash back isn't life-changing money. Don't apply out of FOMO alone. • If you've already done your research and this card genuinely fits your setup, now is the time. • If you haven't researched it yet, don't panic-apply. A rushed application you regret later is worse than missing a discontinued card. • There will always be other cards. This one is good, but it's not unique. The rumor comes from Reddit with screenshots, so take it for what it's worth. But when multiple people are seeing the same thing and the date is this tight, it's worth paying attention. Sources: https://www.reddit.com/r/CreditCards/comments/1tognri/the_end_of_the_custom_cash/ https://www.doctorofcredit.com/rumor-citi-to-discontinue-custom-cash-card/

Poll

22 members have voted

0 likes • 30d

Unfortunatly it has 3 % FX. FX are really a pain

May 19 •

Equifax vs FICO: The Truth

Most people building US credit start with Equifax or Credit Karma. It's free, it's easy, and it feels like you're tracking your progress. Here's the problem: that number you're looking at is probably not the one your lender sees. Equifax/Credit Karma = VantageScore Credit Karma shows your VantageScore 3.0 or 4.0 from Equifax. Completely free, yes. But over 95% of lenders don't use it. And the kicker: your VantageScore typically runs 20 to 60 points higher than your actual FICO score. That gap is the difference between an approval and a denial. What Lenders Actually Pull FICO scores. Whether you're applying for a credit card, a car loan, or a mortgage, the lender pulls your FICO. Not VantageScore. Not Credit Karma. Not the score Equifax shows you. For Cloud Residents building credit with an ITIN, this hits harder. You're working with a thinner file, fewer accounts, shorter history and no proper channels to monitor your FICO. How to See Your Real Scores Platforms like myFICO let you view real scores. These are the same numbers lenders pull when you apply. The Play Use Credit Karma or Equifax as a baseline monitor. It's fine for watching report changes, new accounts, and inquiries Before you apply for anything, check your actual FICO. Know the real number, not the inflated one The gap between your VantageScore and FICO tells you exactly where you stand The difference might surprise you. See you in comments, Ain - Cloud Resident

Poll

30 members have voted

2 likes • May 19

My FICO Score is 14 points better then my Vantage Score at Equifax 😅

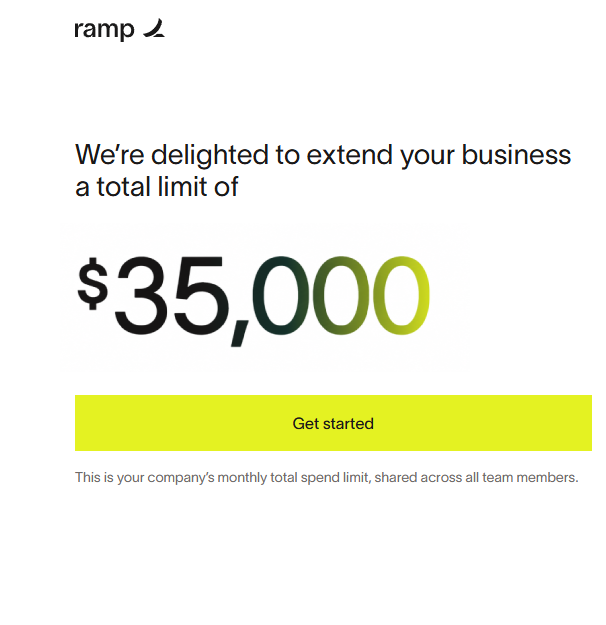

May 12 •

Ramp Approved — $35,000 ✅

Yesterday I applied for Ramp. Today I got approved. I asked for $35,000. That is exactly what they gave me. The process was not instant. First they asked for proof of identity. I submitted my passport. Then they asked for my EIN letter. I submitted that too. Today the approval came. $35,000 limit. The interesting part: they gave me exactly the amount I requested. Not less. Not more. Exactly $35,000.

0 likes • May 12

Awesome

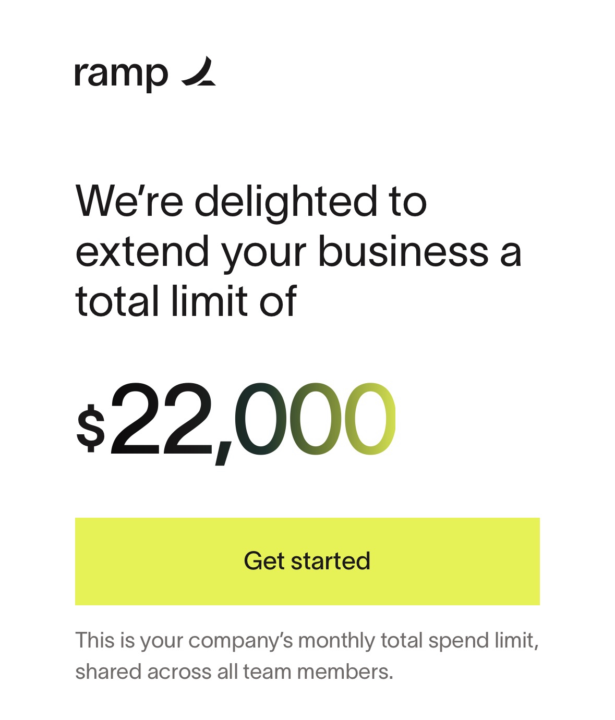

May 9 •

Ramp Card Approved — $22,000 Limit in 3 Hours

Strong datapoint for anyone building US business credit. I applied for the Ramp card and got approved for a $22,000 credit limit in around 3 hours. The process was much easier than I expected: No VPN. No document upload. No complicated forms. No long review. No back-and-forth. Just a simple application, and approval came through the same day. One interesting point: Ramp approved me for exactly the amount I requested. I asked for $22,000, and that is what they gave me. Looking back, I probably should have asked for more. Small regret there 🙂 And on top of the approval, they are also giving a $1,000 bonus gift. My takeaway: if your business profile and banking activity are solid, don’t be too conservative with the limit you request.

0 likes • May 12

Wonderful

1-10 of 39

Active 3h ago

Joined Jan 31, 2026

Powered by