Activity

Mon

Wed

Fri

Sun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Owned by Jeff

Personal financial budgeting course. Unique. Transformative. Simple 1- page method. No spreadsheets. Positive money mindset.

Memberships

Synthesizer: Free Skool Growth

43.2k members • Free

🏛️ Coaching Academy

3.6k members • Free

Course Creation Academy

472 members • Free

The Aspinall Way

32k members • Free

The Stronger Human

28.2k members • Free

Leadership Skool

1.6k members • Free

Free Skool Course

70k members • Free

Skoolers

176.2k members • Free

Creator X

12.7k members • Free

20 contributions to Bad Ass Budget

12d •

Pay Yourself First Method Article

Here is a great post from Citizens Bank on the Pay Yourself Method, which is the method I teach here in Bad Ass Budget. https://www.citizensbank.com/learning/pay-yourself-first-budget.aspx

0

0

May 14 •

When you need money, use credit card, or use Emergency Fund?

Hello All, When you need money to cover expenses, it is best to use money that you have saved in an savings account. It's OK to dip in, and we will then put the money back when we get paid. Here are the thoughts from Gemini AI also to give you a clear picture. This is a classic "math vs. convenience" dilemma. While the credit card feels easier in the moment, the best move for your long-term financial health is almost always to use the emergency fund. Here is the breakdown of why the savings account wins out and how to think about your "repayment" plan. 1. The Cost of Borrowing vs. Saving The biggest factor here is the interest rate spread. - Credit Cards: Most cards carry interest rates between 20% and 30%. If you don't pay the full balance by the due date, you are effectively paying a massive "convenience tax." - Savings Accounts: Even a high-yield savings account likely earns you around 4% to 5%. The Logic: By using your savings, you lose out on a tiny bit of interest (pennies or a few dollars). By using a credit card and potentially carrying a balance, you are paying the bank significantly more than you would have earned. 1. When the Credit Card is Acceptable There is one scenario where the credit card is the better tool: if you use the card to earn points/cashback and guarantee you will pay the statement in full before any interest is charged. However, if there is even a 10% chance that your next paycheck won't cover the full card balance, stick to the cash. Best Practice: The "Self-Loan" Method Since you are already on a budget, treat your emergency fund like a bank: 1. Withdraw the cash for the immediate need. 2. Adjust the budget: For the next one or two pay periods, mark "Replenish Emergency Fund" as a high-priority line item. 3. The "Pain" Factor: Using the savings account makes the expense feel "real." This often leads to more disciplined spending over the next month compared to the "invisible" nature of a credit card swipe. An emergency fund is exactly for this—preventing you from going into high-interest debt when life gets expensive.

0

0

May 14 •

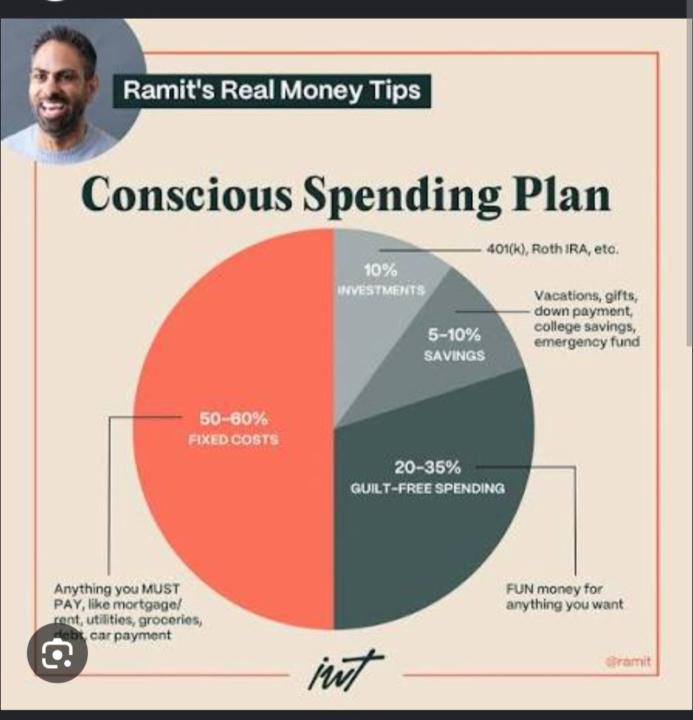

Conscious Spending Plan by Remit Sethi

Hey there. Here is Ramit Sethi's conscious spending plan. Its a bit of a different method, and IMO you have to have extra money in your budget to have guilt free spending. But overall its much like the 50/30/20 plans out there.

0

0

May 6 •

Quantum Vibrations and 4th Dimention. Solid explaination.

Here is a great video, very much like Joe Dispensa but a more solid, concise way. Love it. Quantum entanglement. Listen and take it in, its a great view of how to bring the future to you.

0

0

Mar 22 •

California to mandate financial education in high school.

https://x.com/i/status/2035405182948045229

0

0

1-10 of 20

@jeff-eisert-7711

Creator of Bad Ass Budget, a 1-page super simple way to budget your money. Budgeting, Investing, Mindset and Community.

Active 11d ago

Joined Oct 30, 2025

INTJ

Oceanside, California