Activity

Mon

Wed

Fri

Sun

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

What is this?

Less

More

Owned by Investorms

Become a macro analyst 📈 • Master technical analysis • Execute with precision 🎯 • Decode market myths Old-fashioned investors are bleeding money 💰

Think of this as a gym for your brain. We break down powerful books, mindset upgrades, and practical insights you can apply immediately.

Memberships

16 contributions to Investorms

6h •

Real-Time Macro Case Study: Conflict & Recovery Timelines

Understanding this material will help you understand why the market reprice and for how long. In the comment section you'll find a list of stocks that are mostly affected positively and negatively. Yesterday we mapped recovery assuming hostilities stopped. Today, that assumption weakens. In the last 24 hours, strikes have shifted toward "economic arteries", not just military targets. For investors, this is not a tactical detail -- it changes the pricing model. Here is what worsened in only 24h. 🛢️ Energy Infrastructure -- Timeline Risk Expands Yesterday: weeks to 6 months. That still applies to repairing oil fields and refineries. What changes is the "export layer". With ports hit and the Strait of Hormuz effectively disrupted: • crude may be produced • but shipments bottleneck • insurance pricing spikes • LNG cargoes face delay or rerouting Production recovery ≠ export normalization. From a market perspective: • the geopolitical risk premium in oil becomes stickier • volatility increases • forward curves steepen under uncertainty • refiners and import-dependent economies face margin pressure If maritime disruption continues, energy pricing reflects logistics stress -- not just supply capacity. --- 🛰️ Military & High-Tech Systems — Stabilization Delayed Yesterday: 3 to 5 years for full rebuild. Now add another constraint. Key allied bases responsible for securing sea lanes and reopening trade corridors have been targeted. Reduced stabilization capacity means: • maritime security risk remains elevated • shipping costs stay inflated • insurance markets remain tight • trade normalization slows For capital markets, this extends: • defense spending cycles • supply chain bottlenecks in aerospace • rare earth and component pressure The bottleneck is no longer only manufacturing --it is operational control. --- 💰 Economic Confidence — Confidence Shock Intensifies Yesterday: 5 to 10 years. New developments directly hit: • Dubai’s aviation hub • commercial ports

0

0

1d •

Middle East Macroeconomy Projection

In the comments section I will add which investments can potentially profit or suffer. If war in the Middle East stopped today, the Gulf would recover — but not uniformly. Full recovery separates into three timelines: • energy infrastructure • military and high-tech systems • long-term economic confidence The region has deep capital reserves. What it does *not* control is global supply chain friction. Here is the realistic recovery map. --- 🛢️ Energy Infrastructure Estimated timeline: weeks to 6 months This is the fastest-moving layer. There is clear precedent. After the September 2019 strikes on Saudi Aramco’s Abqaiq and Khurais facilities — which removed ~5.7 million barrels per day — production capacity was largely restored within weeks. Structural advantages: • highly standardized oil infrastructure • large domestic spare-parts inventories • centralized state operators (Aramco, ADNOC) • sovereign wealth funding with no financing delays Important exception: Qatari LNG liquefaction trains are more specialized and less easily substituted. Recovery there likely trends toward the **upper end of the window**. Assessment: Oil flows normalize relatively quickly. --- 🛰️ Military and High-Tech Systems Estimated timeline: 3 to 5 years This is the primary bottleneck. Physical cleanup of bases can occur quickly. Rebuilding the integrated defense and intelligence architecture cannot. Hard-to-replace assets include: • advanced radar systems • air defense networks • satellite communication hubs • specialized command infrastructure Constraint: Western aerospace and defense manufacturers are already operating with multi-year backlogs and tight rare-earth supply chains. Capital is abundant. Production capacity is not. Assessment: Defensive capability restoration is measured in years, not months. --- 💰 Economic Confidence and Capital Flows Estimated timeline: 5 to 10 years This is the slowest variable and the least visible in early headlines. Over the past decade, Gulf economies — particularly the UAE and Saudi Arabia — have positioned themselves as stable, globally integrated investment hubs under programs such as Vision 2030.

1 like • 1d

Highest-odds price increase in the near - intermediate future if ceasefire happens soon: 📈 Likely beneficiaries • Western defense contractors → forced multi-year restocking cycle • Energy shipping / tankers → insurance + routing friction lingers • Non-Gulf oil producers → risk premium decays slowly • Defense supply chain / rare earths → production bottlenecks tighten 📉 Likely losing bets • Gulf mega-projects → higher risk premium, slower FDI • Gulf-exposed airlines → margins pressured by insurance + routing • Luxury tourism in region → sentiment recovery lag

0 likes • Jan 26

Yes absolutely, an entire part of our course is dedicated for commodity supercycle and all its variables, I'll share it with you soon.

1 like • 2d

we hope that you are enjoying our latest gold updates like you asked :)

3d •

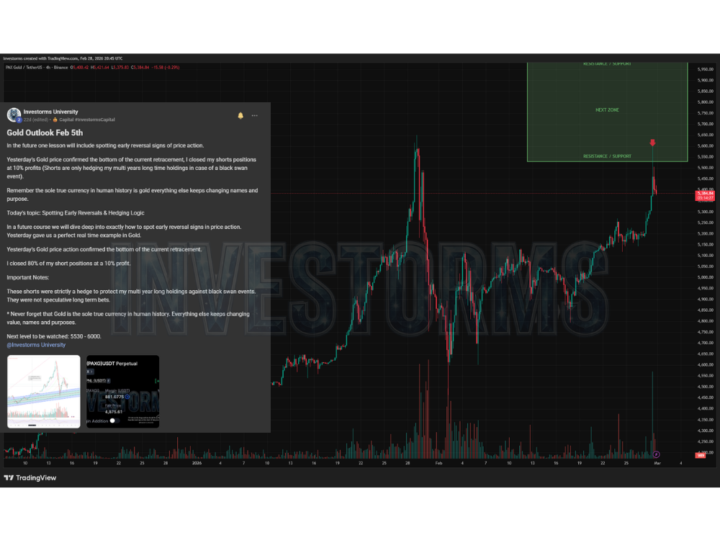

Update: Gold Outlook Feb 28th 🎯Target Hit

In our February 5th outlook, we mapped out the next critical zone to watch for Gold: 5530 - 6000. Today, that target was officially hit. Today’s big move was triggered by the war in the Middle East, but make no mistake the conflict was not the root cause. You will often hear mainstream analysts scrambling to explain a market move simply because something big happened in the news. We strive at Investorms to make you not think superficially. News events only confirm and accelerate the structural market moves that have been building quietly for years. Short-Term Noise vs. Long-Term Clarity - The Short Term (Unpredictable): Immediate price action from here is erratic. We could very well see a quick drop on Monday just to close the price gap left open since Friday. - The Intermediate to Long Term (Unquestionable): For our active trading positions, we are focused on intermediate to long-term profits. Looking at the larger cycle, it is almost unquestionable that we will break upward to set a new All-Time High. We will highlight the created pattern in a later updates. Important Note: Our posts are strictly for educational purposes and do not constitute trading advice.

0 likes • 3d

To add some context on our specific buy and sell on the chart: The long position that hit today’s target was entirely funded by the profits we secured from our previous short (as detailed in our Feb 5th update). Today, we locked in profits on 20% of that recent buy position, letting the rest ride the macro trend. As for downside protection if the price unexpectedly collapses from here, we rely on our trading bots deployed to automatically short every new 10% price spike and take profit on every subsequent 5% drop. This ensures our multi-year holdings are continuously hedged against volatility. We will be breaking down the exact mechanics of how to build and deploy these automated hedging systems in our upcoming courses.

5d •

🐺 Introduction

Nickname + where you’re based: Background / skills (any level): What you want to build here (goal): Skills you want to learn (to earn or build):

1

0

1-10 of 16

@investorms-university-8409

Lowkey Goldmine. ⛏️ You're taught to read news; I teach you to engineer a wealth machine. 🗾 Reclaim your freedom of time.⌛ Welcome to Investorms. 🤝

Active 23m ago

Joined Jan 26, 2026

Powered by