Activity

Mon

Wed

Fri

Sun

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

What is this?

Less

More

Owned by Eduardo

Memberships

Tu Crédito, Tu Legado

59 members • $7/month

EmpowerU Network

16 members • Free

The Enforcement Academy

30 members • $39/month

Rob The Credit Guy

577 members • Free

Skoolers

190.3k members • Free

Community Launch

10.3k members • Free

EliteACRM

211 members • $1/month

Acreditan2Futuro

291 members • $79/month

5 contributions to EliteACRM

25d •

Can a credit card company still “ban” you after an FCRA settlement if you refuse a lifetime ban?

I’m currently in settlement discussions with a credit card company over FCRA credit-reporting claims. They agreed to: • $7,500 cash settlement • Balance waiver • Tradeline deletion However, they added a lifetime ban on applying for or using any of their future products, which I clearly rejected. My questions are for people with real experience: 1. If you refuse a lifetime ban (or it’s not included in the settlement), can the company still effectively ban or blacklist you anyway? 2. Have people here applied again later and been approved, even after disputes, lawsuits, or settlements? 3. Is there any typical time frame (years, policy cycles, internal review periods) after which approval becomes possible again? 4. Does this usually affect only credit cards, or have people seen it impact other products (bank accounts, prepaid cards, etc.)? I understand lenders always have discretion to deny credit — I’m specifically trying to understand the practical reality after asserting FCRA rights, not legal theory. Appreciate any firsthand experiences.

0 likes • 25d

I’m not the most experienced but I think every business is allowed to get you as client or not

25d •

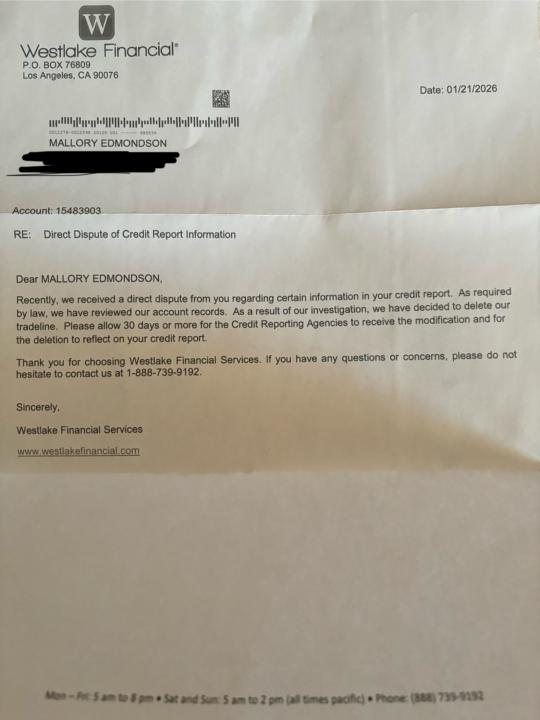

Charged off/ repo deleted!

I’ve been disputing westlake for well over a year and it only took round 1 of the charge off discovery letter to get it deleted!

1 like • 25d

@Mallory Edmondson I have mailed maybe 6 or 7 letters and nobody respond yet

2 likes • 25d

@Mallory Edmondson thanks. I am very hopeful with this method. The first one I did was just 30 days ago. I hope receive these responses within the next weeks

Jan 25 •

American Express FCRA settlement negotiation – how far do they usually go before arbitration?

I’m in a settlement negotiation with American Express over alleged FCRA violations related to a charged-off Hilton Honors account. Quick timeline: • I disputed reporting errors on the charge-off for about 6 months with the credit bureaus. • No corrections or deletions were made (just automated “verified as accurate” responses). • I then sent a Notice of Intent to Arbitrate. • AmEx’s settlement offers so far: • First offer: $0 (balance waiver + deletion only) • Second offer: $1,000 • Third offer: $2,000 They continue to deny liability but say the offers are “goodwill.” I countered at $10,000, with $7,500 as my absolute minimum, plus deletion and balance waiver. I’ve made clear that anything under $7.5k isn’t acceptable and that I’m prepared to file arbitration if we don’t resolve this. For anyone who’s been through this with AmEx (or similar banks): • How far do they usually increase offers before letting it go to arbitration? • Do they tend to move more after arbitration is filed, or before? • Did anyone actually see them settle closer to demand once arbitration fees were on the table? • Any experience specifically with AmEx and FCRA disputes? Not asking for legal advice — just real-world experiences.

0 likes • Jan 27

I have started to challenge the creditors this year with my clients. I hope to hear about those settlements asap 🙏. This method will be very profitable and secure for my clients

Jan 4 •

Discover Letter

Could I send a Discover Letter to a creditor through CFPB or it is always better by certified mail?

1-5 of 5

Active 3h ago

Joined Dec 25, 2025

Powered by