Write something

Jan 6 •

Action. Behavior. Knowledge.

This is why we are here. To provide knowledge and education. Education is key. How are you making sure you continue your financial literacy? Are you reading books on it? Are you joining discussions and groups focused on it? Have you taken any recent classes about it? Just as everything else evolves, so does the financial world and the products available to help us save and grow retirement money. How are you making sure you aren't getting left behind? How can you better set yourself and your family up for a beautiful and long retirement?

2

0

Dec '25 •

Automate, Don't Procrastinate

Creating savings and "retirement" funding is as easy as budgeting and automation. Uh oh, I said "Budget" 🚩🚩🚩 Why is "budgeting" such a bad word?! I believe it's because there is a general lack of knowledge around financial literacy. We are a country that literally avoids the subject. Financial literacy is rarely, if ever, taught in schools, and we cannot even walk into our local banks and get the education that the 1% (the ultra wealthy) is provided with. Instead, in general, it has become 'taboo' to talk about money. Well here, we strive to empower through education! So today I am providing 3 simple rules that can make a huge different to help improve your financial state. In doing so, you can get back to that bubble bath and let your money work for you! 1. Pay yourself first. We all live "paycheck to paycheck" right? ...WRONG! Generally speaking, the more we make, the more we spend! So by figuring out which expenses are discretionary and which are non-discretionary, and where we can cut back (yes, this may be a little uncomfortable at first), then we can figure out an amount that can be saved each month for the long-term. Think growth, strengthening and stretching yourself financially. You wouldn't always want to just pick up the lightest weight in the gym. Strengthening your capability to save is the same, you might feel a little sore for a bit after, but you will also start to see results and feel more confident too! 2. Automate that money!! Set up a monthly amount to automatically go into the account that you choose for your long-term savings. And yes, by definition, this means this is not money that you are allowed to touch for many, many years! DO NOT TOUCH THIS MONEY, until retirement that is. So make sure you do have some liquid money that is in another account for emergencies first. 3. And finally, make sure that the account you DO set up for this long-term growth is one that is aligned with your risk tolerance, and is growing at a pace faster than inflation. It doesn't help you to be saving somewhere where the money is actually depreciating in value.

Nov '25 •

The 3 Legged Stool

Pensions. Social Security. Personal Savings. These are the three legs of retirement. Or at least they were established to be just that many decades ago. 🔴 Pensions have all but disappeared. If you are still in the working force and have a pension of more than $600 or $700 a month coming your way, then you are in the vast minority! And what is $700 going to cover in retirement anyway? That doesn’t even cover food now in most households! I have clients who easily spend $4-$500 a week on groceries for their families. 🟠 Social Security, well, how much faith do you have that it will not be greatly changed, reduced, or even completely wiped out by the time you, or your children, or your children’s children get to retirement age? In ‘The Power of Zero’ David McKnight talks about how when SS was first established in 1935, “…the math behind it ensured its financial viability into perpetuity” because we had around 42 working individuals paying into SS, for every one retired individual taking money out. Furthermore, at the time, the average life expectancy was 62, and the retirement age was 65! While our retirement age has not moved much, our life expectancy has increased to 85! One in 3 women live to age 90! And because the baby boomer generation did not have as many children when they grew up, our working to retired ratio (rather, those paying in, to those taking out SS) is more like 3 to 1, and moving into 2 to 1 very quickly. The math isn’t mathing anymore. 🟡 So what we are left with is Personal Savings… 😳 How much are you saving for retirement? Are you paying yourself first? Are you placing your money into a growth state and letting it compound at a higher interest rate and over a longer period of time? 🙋🏻♀️🙋🏽♂️🙋🏼Who wants to learn how to empower themselves to save better? Take charge & 10x their money? What strategies are available to compound your savings faster? Let’s talk!

Nov '25 •

Congrats, you failed!

Ouch! Too harsh? Failure, loss, and being told no, these are quite often difficult to swallow. Pushing many people to give up, or even worse, to never try. Fear creates huge setbacks. So I want to take a moment to celebrate our fails. I have adopted the idea that within my business I will “No” my way to every “Yes” and I will count each no as a small win, because it means I’m that much closer to my next yes! I encourage you to share a recent failure or “No” that you received, so we may celebrate our best efforts together! #trial&error #failyourwaytosuccess #entrepreneurialmindset

Oct '25 •

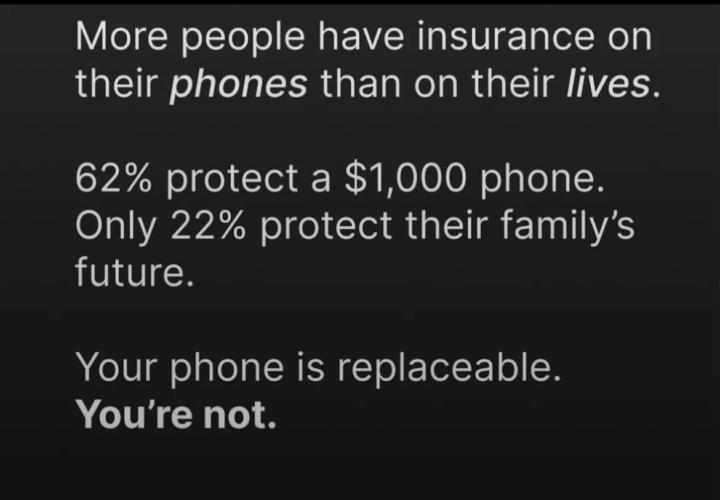

Are you insured?

Who’s paying your bills if you’re injured or sick and you cannot work for 6 months, a year, or longer? Life insurance can. For just pennies to the dollar, you can ensure a backup plan if something happens. Just like you can replace your cellphone for free it it is ensured. You don’t have to pay out of pocket. Do you have insurance on your life, or just on your phone?

1-5 of 5

powered by

skool.com/the-prosperity-project-9756

Built to empower you to not only take charge of your personal finances, but to grow a community focused on lifestyle, family, faith, & future.

Suggested communities

Powered by