Write something

15d •

Bad credit is expensive.

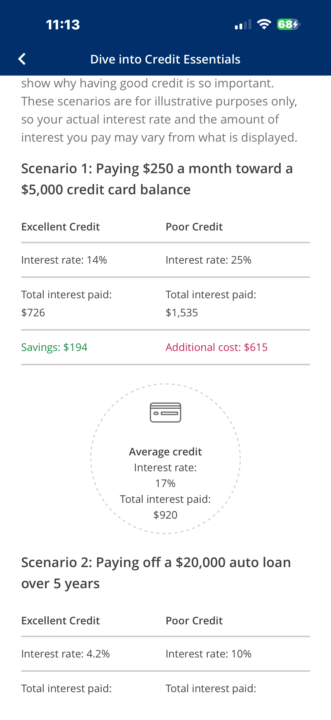

A lot of people think a credit score is just a number, but it actually determines how much money you pay in interest over time. Look at these examples. If someone with excellent credit carries a $5,000 credit card balance, they might pay around $726 in interest. Someone with poor credit could pay $1,535 for the exact same balance. Same thing with a car loan. On a $20,000 auto loan, someone with great credit might pay about $1,656 in interest, while someone with poor credit could end up paying over $4,100. And when you get into mortgages, the difference becomes massive. On a $300,000 home, the difference between good credit and poor credit could cost someone over $76,000 extra in interest. Your credit score doesn’t just affect approval, it affects how expensive life becomes. This is why building and protecting your credit profile is so important. What’s something about credit that surprised you the most when you first started learning about it?

0

0

22d •

Credit Myth: Carrying a Balance Builds Your Score

A lot of people still believe you need to carry a balance and pay interest to build credit. That is completely false. You do NOT need to carry a balance. You do NOT need to pay interest. You do NOT need to “leave something on the card.” Your credit score improves from: • On-time payments • Low utilization • Age of accounts • Responsible behavior Paying interest does nothing for your score. It just makes the bank richer. Have you ever heard this myth before?

0

0

25d •

Credit Tip of the Day: 30% Is Average. Not Elite.

A lot of adults think staying under 30% utilization is “good.” And technically… it is. But here’s the truth: 30% is average behavior. If you want an 800+ score, you don’t aim for average. Most high FICO achievers report under 6% utilization. That means: – If you have a $10,000 limit, you should report $600 or less. – If you have a $5,000 limit, you should report $300 or less. And ideally, you’re reporting low balances across all cards or just even one works Important: this doesn’t mean you can’t use your cards. It means you manage what reports. Low reported balances = low utilization = stronger scoring behavior. If your utilization is sitting at 20–30% consistently, that alone could be holding your score back. Be honest — what’s your current utilization range?

0

0

28d •

Everyone wants an 800 score but they don’t follow 800 behavior.

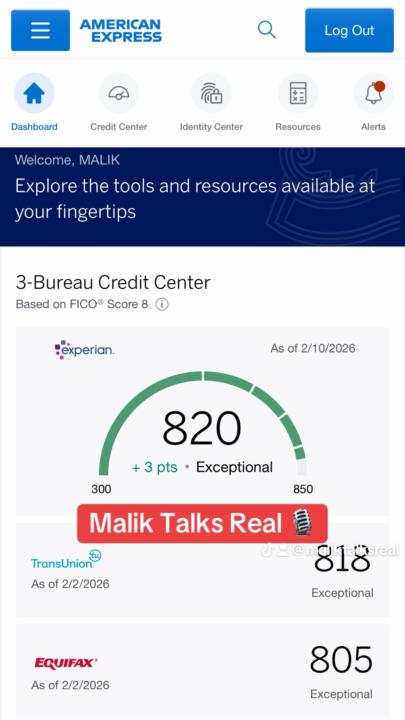

Everybody says they want an 800. But look at the data. Only a small percentage of people even reach that range. It’s rare for a reason. An 850 consumer doesn’t: - Max out cards. - Miss payments. - Apply emotionally. - Carry high balances. The difference isn’t luck. It’s behavior. The average consumer carries higher balances, higher utilization, and less discipline. An 800+ score is not about making more money. It’s about managing what you already have correctly. My 820 didn’t happen because I’m special. It happened because I followed boring rules consistently. Low utilization. On-time payments. No emotional decisions. If you want an 800, you have to act like someone who already has one. Be honest… What habit do you think is holding your score back right now?

1

0

28d •

Your Credit Score Is a Behavior Score

Most people think credit is about money. It’s not. It’s about behavior. Your score goes up when you: - Pay on time. - Keep balances low. - Don’t open accounts emotionally. - Stay consistent. Your score drops when you: - React emotionally. - Overspend. - Miss payments. - Close accounts randomly. Credit isn’t complicated. It’s predictable. If you’re struggling with your score, what do you think is the main reason? Let’s talk about it below.

1

0

1-7 of 7

powered by

skool.com/the-abundant-learners-club-2265

Let’s talk about what school, our parents and life never taught us 📚

Suggested communities

Powered by