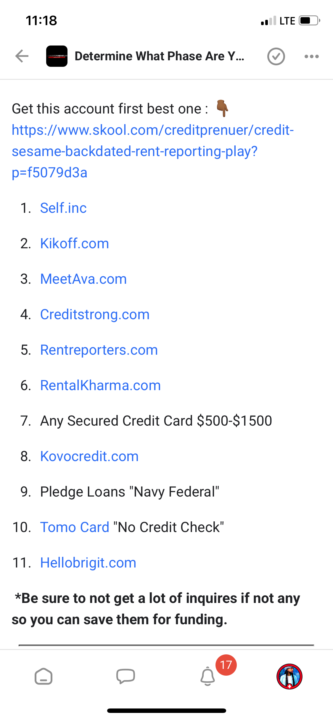

6d •

ADD TRADELINE AND PRIMARIES TO YOUR CREDIT

HERE A LIST OF ACCOUNT, THAT CAN BOOST YOUR SCORE, AND GET YOU APPROVE.

0

0

20d •

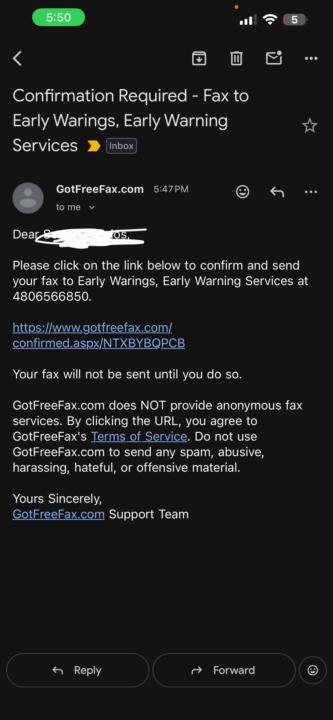

Fax the Secondary Bureaus

To get a quicker response from the secondary credit bureaus, call them and fax them at the same time. While on the phone, watch how the conversation changes. Read Below . 1. Core Secondary & Public Records Bureaus These agencies gather extensive public records, asset data, and alternative credit histories. LexisNexis Risk Solutions (Consumer Center) Fax: (866) 414-4436 Usage: Best for requesting/disputing your primary full disclosure file or Accurint reports. SageStream (A LexisNexis Subsidiary) Fax: (858) 312-6275 Usage: Direct lines for alternative credit score and subprime credit data disputes. Innovis Note: Innovis officially decommissioned their public consumer dispute fax lines in favor of their secure online consumer portal and certified mail processing. If you absolutely require direct electronic delivery, utilize their phone dispute line at (1-866-712-0021) to request an immediate file update or a secure upload link. 2. Banking & Checking Account Bureaus Essential for fixing forced closures, checking history data, or handling identity theft issues related to bank accounts. ChexSystems Fax: (602) 659-2197 Usage: Send completed Consumer Request for Disclosure or Factual Dispute forms directly to Consumer Relations. Early Warning Services (EWS) Note: EWS does not maintain a public-facing inbound fax line for consumer disputes. They strictly route incoming factual disputes through their online portal or standard mail. 3. Subprime & Alternative Lending Bureaus These bureaus track short-term lending, payday loans, auto title lending, and rent-to-own agreements. CoreLogic Teletrack Fax: (800) 237-6526 Usage: Handles consumer services, report disclosures, and traditional file disputes. Clarity Services (An Experian Company) Note: Clarity processes freezes and disputes via their dedicated online portals. To bypass mail delays, use their direct consumer phone line at (866) 390-3118 to initiate an immediate investigation or secure document link over the phone.

1

0

21d •

🚀 The Best Credit Gems for Funding Your Fuel (Stop Leaving Money at the Pump)

Family, if you are out here building businesses, scaling operations, and running the daily play, you are spending money on gas. But if you are using a basic debit card or a weak 1% cash-back card at the pump, you are literally leaving free money on the table. We talk a lot about high-ticket funding, but optimizing your everyday data points is how you build a rock-solid foundation. Here are a few absolute credit GEMS you should be stacking to turn your fuel expenses into a major leverage point: 1. 💎 Citi Custom Cash® Card The Strategy: Use this card strictly for gas and nothing else. The Play: It automatically grants you 5% cash back on your highest spending category each billing cycle (up to the first $500 spent per month). By isolating it just for fuel, you instantly lock in a permanent 5% discount every time you fill up. Annual Fee: $0 2. 💎 Wells Fargo Autograph® Card The Strategy: The ultimate no-fee multi-tool for the daily grind. The Play: You get an unlimited 3x points on gas and EV charging stations. On top of that, it pulls 3x points on restaurants, travel, transit, and streaming. It’s an elite card for building data points without paying an annual fee. Annual Fee: $0 3. 💎 Sam’s Club® Mastercard® The Strategy: The wholesale heavy hitter. The Play: If you already have a membership, this card gives you a massive 5% cash back on eligible gas worldwide (up to the first $6,000 per year). The cheat code here is that it works at any eligible gas station, not just Sam’s Club pumps. Annual Fee: $0 (Requires Sam's Club membership) 4. 💎 Blue Cash Preferred® Card from American Express The Strategy: The ecosystem builder. The Play: It drops 3% cash back at U.S. gas stations and on transit (rideshares, tolls, parking). Plus, it gives you 6% back on U.S. supermarkets. If you want to start building that high-value relationship with Amex, this is a phenomenal entry point. Annual Fee: $0 intro annual fee for the first year, then $95. 💡 THE PRO-TIP

1

0

Apr 30 •

The "Magic Eraser" — OpenSky® Secured Visa®

Best for: People who have been denied everywhere else (even after bankruptcy). How it works: OpenSky is famous because they do not perform a credit check. Period. Your limit is based entirely on the deposit you send them ($200 to $3,000). The Step-By-Step: Go to the OpenSky website. Fill out the basic info (Name, SSN, Income). The Application Secret: When it asks for your income, remember the "Serial Entrepreneur" rule: include your job, your side hustles, and any shared household income. Send your deposit via a debit card or bank transfer. Your card arrives in 7–10 days.

2

0

Apr 20 •

Every morning, feed your mind.

When you wake up, the first thing that should be on your mind is structuring how you want your day to be, by meditating using the 3,6,9 manifesting method. It might sound ridiculous, but trust me, it works. Give yourself an affirmation in the mirror before you check your phone. Write the credit score you want, write how much money you want, or funding. Anything that's going to align your day with your success. 20-30 minutes in the morning when you wake up is the most powerful moment because you awaken from the 4th dimension. That's when your higher self is most one with you. The phone separates us from that by radiation, since we are electric beings and magnetic beings. The two combined become our law of attraction. Feed your mind self-affirmation. High-frequency sounds like 999 Hz, 666 Hz, 333 Hz. I know it sounds silly, but this is the "think rich, grow rich" method. You have to see to believe and see yourself rich so you can trigger your belief system to believe in yourself.

1-26 of 26