Pinned

Feb 8 •

🚀 Welcome to the 700 Club! Start Here (Action Required)

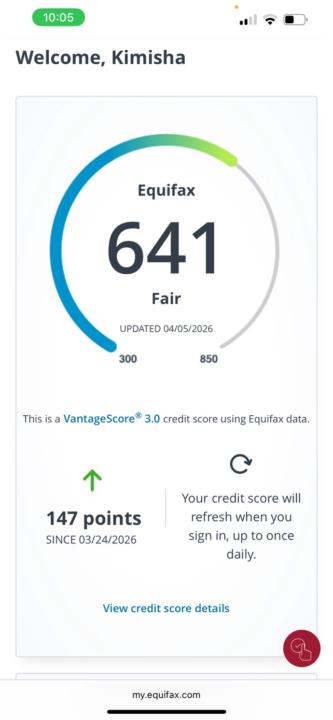

Peace and Strength Team! Welcome to the inner circle. You aren’t just here to “fix your credit”—you’re here to master the system and unlock the lifestyle you deserve. Whether you’re at a 400 or a 650, the goal is the same: Tier-1 Credit and Financial Freedom. Most people fail because they use outdated templates and "free" apps that actually hurt their scores. In this community, we do things differently. We use Metro 2 compliance—the same "federal code" the banks use—to force the bureaus to play by the rules. Where to start right now: Watch the Masterclass: I’ve uploaded a step-by-step presentation (find it in the Classroom tab) that breaks down exactly how to audit your report. Download the Checklist: Get your 400 to 700 Roadmap (attached below). Print it out. This is your battle plan for the next 45 days. Claim Your Gems: Check the "Weekly Letters" section for this week’s free dispute templates. Introduce Yourself: Post a quick "Hello" in the feed! Tell us: What is your goal score? What is the first thing you’re going to do once you hit 700+? (New home? Better car? Business funding?) The Bonus Perks: Don’t forget, as a member, you get access to our 1-on-1 Book Calls and our Weekly Credit Consultations. If you get stuck, the community and I are here to pull you through. The bureaus are betting that you’ll get bored and quit. We’re betting that you’ll stay consistent and win. Let’s get to work. See you in the feed, Samiel Quijano

Jun 19 •

The Truth Hurts: You Can Lead a Horse to Water...

Let’s keep it 100% real for a second. The biggest reason people don't see results in their credit, their business, or their life isn't a lack of information. We live in an era where the blueprints are right in front of you. The real issue? People either don't use the tools they are given, or deep down, they just don't want better for themselves badly enough to change. You can buy the software, join the inner circle, and download the templates. But if those tools just sit there collecting digital dust, your situation stays exactly the same. You can take the horse to the water, but you can’t force them to drink it. If you are tired of looking at the water and you’re actually ready to start drinking, I’m laying out the ultimate 90-Day Gems Hack roadmap. No fluff. Just the exact systems to structure, automate, and fund your life. Choose what side of the fence you're on, and let's get to work.👇

1

0

Jun 19 •

im back

i have alotttt of new gems... The Credit Game is changing, fixing credit is the government worse nightmare.

1

0

1-30 of 80