5h •

💡 Why Your Personal Credit Limits Dictate Your Business Funding Approvals

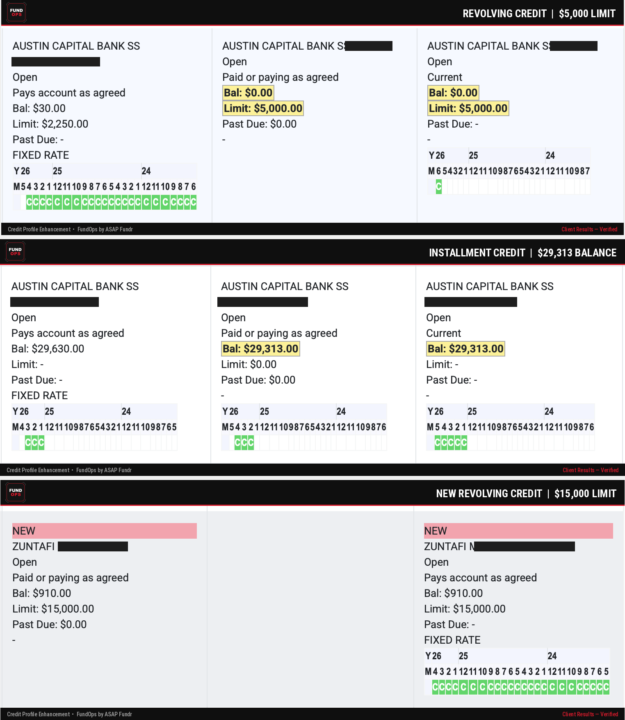

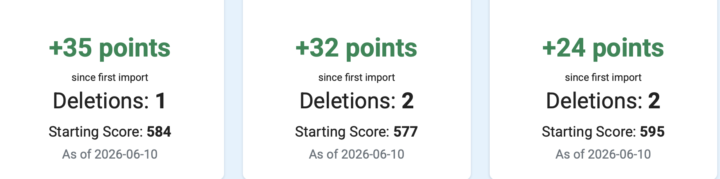

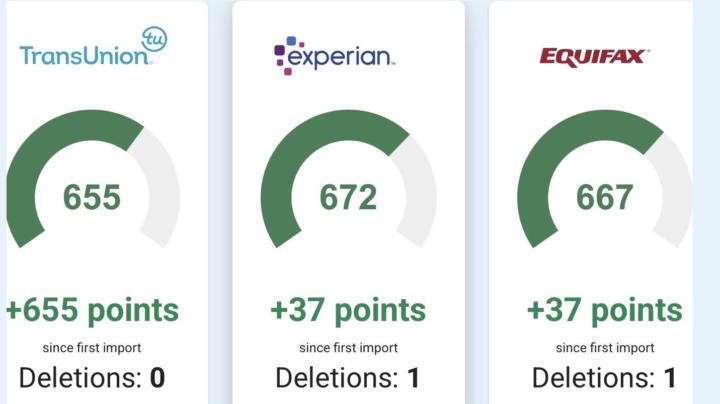

Most business owners don’t realize this… When you apply for business credit or funding, lenders aren’t just looking at your business. They’re pulling your personal credit profile and making decisions based on what they see there. Here’s the truth nobody tells you: - Your personal credit limits signal to lenders how much other banks already trust you with - Low personal limits = low business approvals. It’s that simple. - Lenders use your personal revolving utilization AND installment history to gauge risk - A thin personal credit file = automatic declines on $50K+ business funding So what do we do about it? We build BEFORE we apply. 🏆 Client Win — Jan Pierre @Jan Pierre Ventura followed the FundOps path and strategically added: ✅ $20,000 in revolving credit — including a brand-new $15K credit line and a $5K limit increase ✅ $30,000 in installment credit — a strong installment tradeline reporting across all 3 bureaus ✅ $50,000 total added to his personal credit profile ✅ Perfect payment history — every single month reporting as “Current” This wasn’t random. This was strategic credit positioning — beefing up his personal profile so that when he goes into his funding round, lenders see a borrower they WANT to approve. 📊 Here’s what lenders actually look at: 1️⃣ Revolving credit limits — Higher limits = higher trust signals. Jan went from $2,250 to $20,000+ in available revolving credit. 2️⃣ Installment tradelines — Shows you can manage structured payments. His $30K installment is rock solid. 3️⃣ Payment history — All green. Every month. No exceptions. 4️⃣ Credit mix — Revolving + installment together shows lenders you’re a well-rounded borrower. When Jan walks into his funding round, his profile says: “I handle large amounts of credit responsibly.” That’s the difference between a $10K approval and a $100K+ approval. This is the FundOps framework: 🔹 Build your personal credit strategically 🔹 Position your profile for maximum approvals

2d •

Another Fundops Win

@Dahianna Ventura has been showing up while running a 7 figure establishment in NY! This month we were able to repair some little items holding her back from entering funding and she officially has a CLEAN credit report. Every business has its challenges and every clients process has its turns... but when you have the mindset to win... the strategy always comes together at the end! Looking forward to funding in July!!

20d •

Big Thanks to Timo!!! Wow!!!

Big shout out to Timo. He got my credit score from 515 up to 720 Let’s Go! The numbers just came in today big thanks to him and his team finally moving up to level two Thanks Timo and the A Team

May 14 •

Warwick Credit Results

Let’s clap it up for @Noel Occomy ! Him and I have worked diligently over the months to get his credit in line. We are now one round away from completing, a few meetings away from having his business in line to fund. Thank you for your patience throughout this process

May 5 •

Huge Funding Weekend!!!

@Timo Wilson and his team once again show that they are the best in game. Thur. Approval for 15k BOA Cash Card, and $7500 BOA Travel Card. Friday, approval from Chase for Ink Unlimited 28k. Sunday second approval fro Chase 28k Cash.

1-30 of 49

skool.com/sacredwealthsystems

Correct Credit Errors In Record Speed📈

Access To Our Private Banker Network 💰

Weekly Masterminds & Support

Personal & Business Credit Stacking 💳

Leaderboard (30-day)

1

+102

2

+50

3

+47

4

+28

5

+28

Powered by