🔥

2d •

Why is it that Investing is what we do with extra money?

Where did that programming come from? The best investments I have ever made were decisions to invest with absolutely no money in hand. I found the deal or the group of deals of a lifetime and right there on the spot I decided to get it. I'm talking about coming up with life changing amounts of money. That is where the subconscious mind instantly goes into ACTION! All of a sudden things start to show up. People start to show up. Ideas start to show up that were not there a second ago. Your mind finds a way! If and only if... you truly want that investment above everything else. You're not thinking about food or sleep or anything else. You are determined to get that investment and you will not take no for an answer! ⬇️Has this ever happened to you? Let me know below⬇️

🔥

14d •

Who are you willing to become in order to build a wealthy retirement?

I remember buying my first investment property thinking who do I think I am? I processed that thought over and over in my mind. I came to the conclusion that I want to be thought of and recognized as an investor by my Realtor, my Attorney and my Mortgage Broker. This transformation took place 4-5 months before I had my first investment property. I became a real estate investor just with no houses yet. Fake it till you make it. I would drive around looking at multifamily houses while everyone else was spending their weekends doing weekend kind of stuff! Why? Because that's what Investors did or at least that's what I thought they did. I didn't have a mentor or ChatGPT or a Skool Community. I had my realtor Arlene Longo that was gracious enough to entertain my BS title of "Real Estate Investor" long enough to actually get me to a closing table and sign a ton of papers! I found her while calling a listing of another 2 family house I was interested in. I think we looked at about 30 properties until I came up with my first purchase. I looked at this 2 family and liked it but the numbers didn't work. I drove to the listing agents office and asked the listing agent why I should buy this house. My realtor flipped out when she heard I went around her to gather some Intel information. Turns out the homeowner was going through a divorce and was sleeping in the basement of the 2 family and freaking out the girls renting the first floor apt. and he needed to sell fast! Perfect! I offered my number that worked and they accepted it. My first distressed asset of my life! Who are you willing to become? Drop a line below

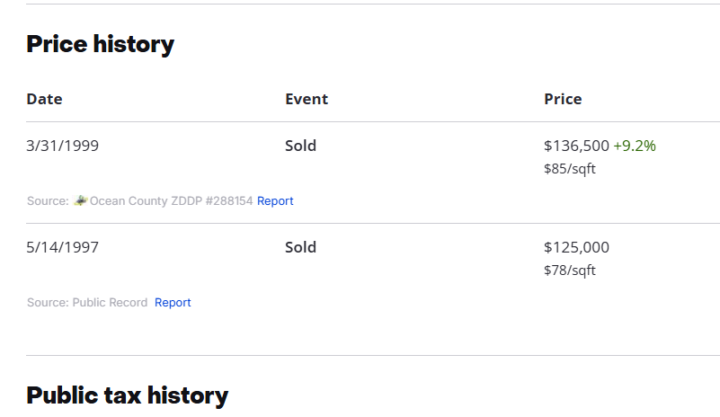

🔥

Mar 26 •

Auction bidding

I hit the sheriff sales every once in a while in different parts of the country and really enjoy the excitement and the bewilderment of first timers. Ha! The look on their faces trying to figure out what the heck just happened? Talking to auction bidders, it's a funny conversation. When asked what I do I say, I bring these deals to auction and watch you all fight over who is going to pay me the most. We have been buying non-performing notes going on 20 years now and foreclosure is our biggest tool in the toolbox. We only foreclose to get the borrowers to take us seriously. If one of our deals makes it all the way to sale, that is a failure on our part and our FC attorneys part. We are looking for cash flow. Multiple streams of income flowing into our tax advantaged retirement accounts. Let us hear some of your auction stories

🔥

Mar 24 •

50 Percent - 50 Percent?

Nearly 50% of American families have ZERO saved for retirement. Let that sink in. According to the Federal Reserve Survey of Consumer Finances, roughly half of households don’t have a 401(k), IRA, or any retirement account at all. This isn’t just concerning… it’s a wake-up call. But here’s the uncomfortable truth: This isn’t only a personal finance problem. It’s a financial education problem. For those of us in the financial education space, this should hit hard. Because if nearly half the country isn’t even getting started, then something in the way we’re teaching, communicating, or reaching people is broken. People aren’t lazy. (Some are) They’re overwhelmed. They’re under-informed. And in many cases, they’ve been left out of the conversation entirely. We don’t need more complex strategies. We need more accessible starting points. Because retirement success doesn’t begin with maxing out accounts… It begins with opening one. If you’re in this field, the mission is bigger than numbers—it’s impact. And if you’re someone who hasn’t started yet: Start small. Start now. Just start. Because doing nothing is the most expensive decision of all.

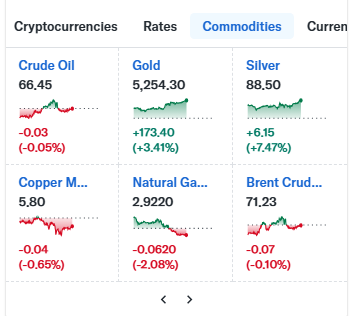

🔥

Feb 23 •

Who pays attention to the boring things?

Silver is in my focus One day move! 7.47% I bought in last month at $60 which was twice the normal price for many years I felt like the sucker at the poker table! HA! Silver is a very rare essential manufacturing mineral. The most conductive element known. Needed in data centers worldwide. Electro vehicle battery material. Solar panel material. Will we see $40 or $150 first? Let's hear it!

1-30 of 52

skool.com/retirement-cash-flow-

Retire wealthy with multiple streams of income! Build these streams one by one. Get one going then work on the next. NO: stocks bonds mutual funds!

Leaderboard (30-day)

1

+20

2

+18

3

+18

4

+14

5

+8

Powered by