13d •

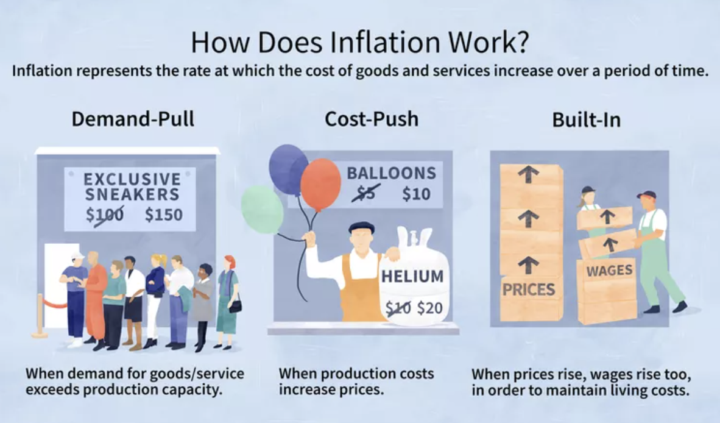

Inflation is a B!T@H 😦

Happy Weekend LEARNin Academy! 🤓 I have GOOD NEWs and BAD NEWs! The GOOD NEWs is that I met face to face over coffee (this past Thursday 8am, April 16th) with someone who found the LIVE show (because the Facebook algorithm, starting hunting him down!) LET EXPLAIN 🤓 He is C-level suite business owner who will be retiring in 5 years and would like real estate investing to be his path to "Financial Freedom". A few tid bits about this potential client: - He owns 2 automotive advertising businesses and estimates the value of those businesses to be $10-12M 😗 A "high net-worth" client ✅ - He has a real estate investor friend who he claims makes $500k per flip on buying Oceanside property 😚 Means that he already is sold on real estate as an investing strategy & potential referrals from his friend ✅ - He has a young daughter who is 9 years old 😙 which helped me build rapport with him VERY easily ✅ I could go on about other positive signs of a "real, legitimate buyer & borrower", but I think the 3 reasons I stated are enough. So let's get to the BAD NEWS. This proved to me that charging 1 cup of coffee per month, or $5/per month is too low.... So... thus prices for new members are going up 10x per month for all 3 levels... Standard, Premium and VIP. But.. there is MORE GOOD NEWS. You still have an opportunity to BECOME A VIP MEMBER in 2026 by paying $543 for the whole year of 2026!! If you have questions, please reach out and we can discuss!!! Let's CREATE together in 2026! Make sure to become a VIP before it 10x in cost!! Coach RU @Ruben Austria

18d •

April 17th Deal for the Day!

@Ruben Austria @Christopher Astillero @Rafael Davis @Martin Magana @Chad Sliwa @Nicole Turner Happy Wednesday, Educators! Let's have the deal for this Friday and post it on the comments! Excited to see what type of property, strategy, and the approach on how you can educate, empower, and inspire investors and home buyers in Santee!

19d •

Client referral for Reverse 1031 Exchange Lender

Hi everyone back from a well rested vacation! Can someone please let me if you are a lender and if your underwriting guidelines allows you to lend on a Reverse 1031 Exchange? Need a lender asap for this transaction! Thank you! 😊

26d •

Deal for April 10 Allied Gardens

Hey everyone! If any of you have a deal or a listing in or around the surrounding areas of Allied Gardens San Diego, we would love to feature it on the deal segment this weekend. We already have a listing from Arnold but we should have time for a more area specific one if anyone has something. Let me know down below by Wednesday if anything comes to mind! Thanks Guys

25d •

Learn Together. Grind Together. Close Together.

Every deal in Allied Gardens tells a story, not just of numbers, but of navigating a market where opportunity lives in the details. From $900K to $1M+ price points, strong price per square foot, and steady demand, this is a neighborhood where persistence and positioning matter more than ever. It’s not about chasing the fastest deal, it’s about understanding the market, staying consistent, and recognizing where the real opportunities exist. Keep showing up. Keep following up. Keep putting yourself in position to win. The deals are out there, but they go to the ones who stay in motion. Someone is looking for exactly what you bring, your expertise, your hustle, your commitment to getting it done. Stay active, stay visible, and stay engaged here in Skool. Share your wins, your lessons, your deals, and your journey. Because the more you show up, the more opportunities you create—not just for yourself, but for the entire community. Let’s keep grinding, keep selling, and keep closing. @Aaron Kruse @Adib Mahdi @Alley Perkins @Anastasiia Buiadzhy @Angel Garduno @Aris Anagnos @Arnold Shackelford @Baylea Ducote @Luis Barboza @Victor Bell @Carver Tripp @Casey Clayton @Christopher Astillero@Claudia Gramm @Colette Gallagher @Corie Aguinaldo @Crystal Hughes @Daryl Dean Santos @Dj Napolitan @Dylan Valenzuela @Harry Dennis @Michele Denys @Rafael Davis @Erica Traulsen @Pamela Edwards @Noemi Flores @Harrison Goldblatt @Hayden Goldberg @Patrick Gannon @Salvador Guzman @Hanjoo Kwak @Jon Hayes @Michael Harris @Maria Ingle @Jean Anagnos @Jeninth S. Roa Hyde @Jim Sprouse @Johana Austria @Julie Pierce Casey @Karla Ruiz @Ryan King @Yoichi Kato @Marilou Lee @Roger Lee @Martin Magana @Michelle Adams @Nicole Turner @Patrick Ono @Ruben Austria @Simi Rush @Stephanie Sundell @Sondra Hooley @Tracie Hasse

1-30 of 51

Leaderboard (30-day)

1

+85

2

+55

3

+47

4

+37

5

+22

Powered by