Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

Creative Real Estate Academy

1.5k members • Free

The Real Estate Academy

4.1k members • Free

The Closing Table

410 members • Free

6 contributions to The Closing Table

2d •

Individual vs. LLC Property Ownership: Insurance & Liability Breakdown

Individual - Policy: Standard Personal Lines (HO-3 or DP-3) - Cost: Lower premiums; cheap to stack a Personal Umbrella policy over top. - Liability Protection: Relies entirely on your policy limits. Personal assets are exposed if a claim exceeds your policy. - Best For: Primary homes, second homes, and beginner landlords with 1–2 properties. LLC - Policy: Commercial Lines or specialized Dwelling policies that allow entity ownership. - Cost: 10%–30% higher premiums; requires Commercial General Liability. - Liability Protection: Strong double layer (LLC corporate shield + policy limits) to protect your personal wealth. - Best For: Real estate investors, partnership-owned properties, and multi-unit portfolios. ⚠️ The #1 Trap: Never transfer a property deed to an LLC without updating the policy. If the owner on the deed (LLC) doesn't match the named insured on the policy, the carrier can deny the claim.

2

0

2d •

Breakdown of the most valuable endorsements available for homeowners policies:

Extended or Guaranteed Replacement Cost: Increases your dwelling limit (typically by 25% to 50%) if building costs surge after a natural disaster and standard limits aren't enough to rebuild. Water Backup & Sump Pump Overflow: Covers water damage to your home and belongings caused by a backed-up drain or a failed sump pump (a major gap in basic policies) Service Line Coverage: Pays to excavate and repair damaged underground utility pipes or lines running through your yard (water, sewer, gas, electric) for which homeowners are responsible Hydrostatic Pressure / Foundation Seepage: Water soaking through basement walls, floor slabs, or foundation cracks due to heavy rain or high water tables is excluded by standard homeowners policies and is generally not covered by standard Water Backup endorsements.

2

0

Nov '25 •

Book Your 1-on-1

Welcome to your 1-on-1 Strategy Call portal: 👉 Click here to schedule: https://api.leadconnectorhq.com/widget/booking/iqfBFEpIGHw2QwcNg4j3 Choose a Topic: ✅ Deal analysis & next steps ✅ Seller call breakdown & scripting ✅ Offer structure + negotiation angles ✅ Dispo strategy if the deal is signed ✅ Creative finance frameworks (when applicable) Please have ready (if applicable): 🔹 Property address 🔹 Seller situation + motivation 🔹 Numbers you’ve gathered (ARV, repairs, ask price) 🔹 Exit strategy you think fits 🔹 Your biggest sticking point Call format: ⏰ 30 minutes 🎯 One focus: momentum + clarity 📌 You’ll leave with an exact next action Rescheduling policy: If you need to move the appointment, please do so at least 4 hours in advance. Who this is for ✅ Action takers ✅ Members who are talking to sellers ✅ People who want deals closed, not theory Who this is NOT for: ❌ “Thinking about it” stage ❌ People who haven’t watched the core training ❌ Tire-kickers After the call you’ll receive: ✅ Call recap ✅ Action steps ✅ Resources (if needed) ✅ Accountability check-in Let’s get your next deal to the table. Book now while slots are available. ➡️ https://calendly.com/ajsantana425/aj-santana-consultation

1 like • May 13

Hey!

0 likes • 15d

@Aj Santana Hey, yes! Super cool but leads are slow

May 22 •

If you are flipping, you need to know the difference between these two:

- Vacant Property Policy: Perfect if the house is just sitting empty while you wait for permits or list it on the market with only minor cosmetic updates. - Builder’s Risk (Course of Construction): Absolute must-have if you're pulling permits, knocking down walls, replacing major systems, or doing structural additions. It protects the existing structure plus your building materials on-site.

2

0

May 18 •

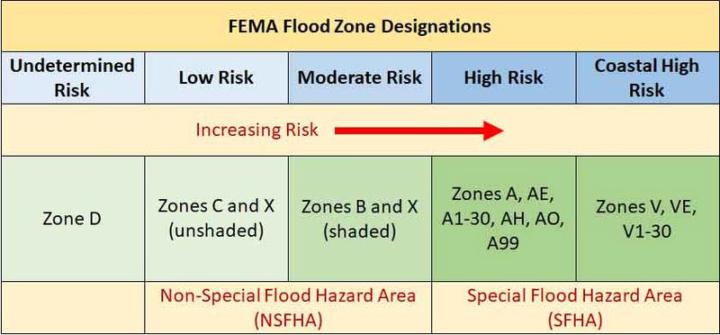

Why the FEMA Flood Zone Map Matters to Investors

For investors, whether in residential, commercial real estate, or land development the FEMA Flood Zone Map is a critical due diligence tool because it directly affects risk, cost, compliance, and value. The FEMA flood zone map is essential because it quantifies flood risk, dictates insurance and lending rules, shapes construction costs, and affects long-term value. For investors, it’s a non-negotiable part of pre-investment analysis to protect capital and maximize returns.

1 like • May 21

@Aj Santana Fema doest the mapping and if they determine that the home is in a flood zone, they will automatically update it. So the answer is YES definetely!

1-6 of 6

@imane-bournine-4977

Your Trusted Property & Casualty Insurance Broker

Active 19h ago

Joined May 13, 2026

Powered by