Activity

Mon

Wed

Fri

Sun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Owned by Ain

Helping non-US residents and business owners access US banking, credit cards, and ITIN - from anywhere.

Memberships

596 contributions to Cloud Residents · US Credit

3d •

⭐ cloudresidents.ai ⭐

What Is Cloud Residents AI, And What Is It Built On? Cloud Residents AI is an assistant built to answer your US credit card and banking questions from real, lived experience, not from a generic AI guess. It is built on: 135,000+ curated data points from nearly five years of real activity, from 2021 to 2026, refreshed monthly. That includes approvals, denials, reconsideration scripts, Financial Review survival stories, and step-by-step walkthroughs from people who already did this as non-residents, with an ITIN and no SSN. Every answer is built from real outcomes and real walkthroughs from people who already did it. So this is not another chatbot that guesses and invents. The intelligence you feel is the curated, cited, real-experience library behind it. Now In Public Beta For the last 3 weeks, this was quietly in private beta with a small group of you. Today, it opens to everyone at cloudresidents.ai, free to use. A real thank you to everyone who tested it in private beta and sent feedback, screenshots, and bug reports. You shaped this, and it is sharper because of you. How It Works Ask in your own words. Type or speak, in 19+ languages. It searches by meaning. Your question is matched against every one of the 135,000+ data points based on what you actually mean, not just keywords. It keeps only the best sources. Hundreds of matches are filtered down to the 10 to 20 most proven, most recent, and most relevant sources. It writes a cited answer. You get a clear, structured answer in your language, with a Sources panel behind every claim. Use Fast for quick answers. Use Pro for deeper, multi-step problems. What You Can Actually Ask This is where it gets useful. You can attach a file or screenshot and ask in plain language. For example: Attach a screenshot of your credit history and ask what to clean up before you apply. Attach your credit file or report and ask which card to try next for your profile. Attach a bank letter, denial, or 4506-T request and ask how to respond and clear it.

Poll

40 members have voted

0 likes • 20h

@Patrick Jersey thanks for this, i’m currently sending from mail.cloudresidents.ai. which has DMARC set up, do you reckon i should also add DMARC/DKIM/SPF to the root domain cloudresidents.ai or doesn’t really matter?

0 likes • 20h

@Apple Service thank you, really appreciate you trying it and glad you like the answers.

1 like • 22h

congrats, that was pretty quick. most members here wait on avg a week to get approved by navy fed.

2d •

Best use for cloudresidents.ai

If looking to build credit from scratch with ITIN, how to best use cloudresidents.ai for this exact purpose? If there are tips recommended, it's greatly appreciated.

2 likes • 2d

cloudresidents.ai can absolutely help you not just start from zero with an ITIN, but also optimize and guide your whole US credit/banking journey. it’s still in public beta so there are bugs I’m finding from everyone’s feedback and I’m fixing them as they show up. in the next few days I’ll drop a new classroom section with exact prompts, examples, and a walkthrough on how to use it properly so you can get max value and accurate results, stay tuned.

4d •

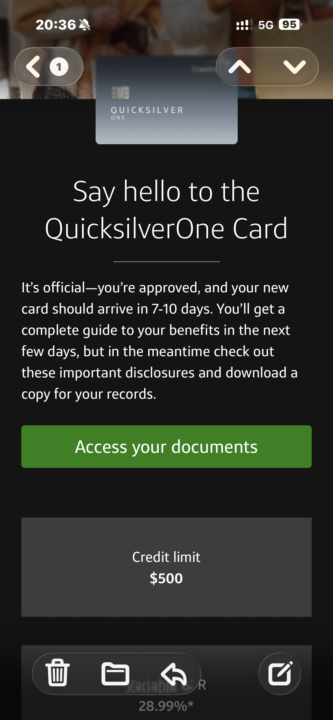

Capitalone approved, Quicksilver 500$ unsecured and closed 2 days thereafter

Recently I received my ITIN with the help of Taxsym, which was very good experience. After a quick chat with @Ain - Cloud Resident and studying the classroom (as premium member), I gave C1 pre approval a shot. What a bummer - no offers! Just dont take no as an answer so I tried again after some days passed, and like magic 2 offers appeared this time. Platinum secured and Quicksilver unsecured. So I grab the quicksilver offer, request for the usual passport and itin paper and getting approved for 500$ unsecured limit 2 days later. Thanks to @Ain - Cloud Resident and the community, theres some solid stuff here. Edit: card was shipped but on the same day account got closed without any extra activity on my side.

1 like • 4d

Big congrats Stefan, really happy for you. $500 is a good starting limit, especially since you were offered both secured and unsecured. For paying the C1 card, yes, you can pay it from any US bank account which supports ACH debit (ach pull / direct debit). If you already have a Wise USD account with US banking details, you can use that. If not, you can also pay with IBKR or Schwab Brokerage or open a new US bank account probably Alliant CU by following the guide shared by @Isabel G Thanks for sharing the DP, Small tip: if you feel like it, edit/adding a screenshot/photo usually makes these posts pop more. 😄

0 likes • 3d

@Golen C. depends, but it's safe to use for paying back your capital one credit card.

3d •

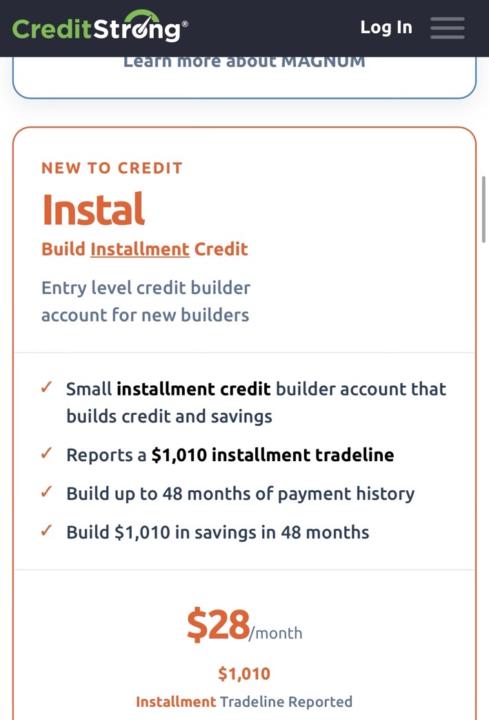

For those currently using CreditStrong, which plan did you choose and why?

I’m looking at: • Revolv ($15+/month)• Magnum ($16+/month)• Instal ($28/month) For those who have used any of these: - Which plan did you start with? - How long did it take to report to the bureaus? - Did you see a meaningful FICO score increase? - If you were starting over today, would you choose the same plan? I’m especially interested in feedback from ITIN holders and non-U.S. residents. I’m leaning toward Revolv because of the revolving tradeline, but I’d love to hear from people who compared it with Magnum or Instal. Thanks in advance for sharing your experience and data points!

2 likes • 3d

creditstrong’s loan plans are daylight robbery, the only thing that isn’t trash is Revolv. pick one revolv tier that fits your budget, leave it open for minimum 2 years

1 like • 3d

@Chrisdy Masson not yet, you need at least 6 months of solid reporting history with creditstrong before you’ll notice anything, the real value is just keeping it open and clean for 2+ years so approvals get easier over time

1-10 of 596

Online now

Joined Sep 18, 2025

Cloud Resident of U.S

Powered by