Activity

Mon

Wed

Fri

Sun

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

What is this?

Less

More

Memberships

Actual Tax Law

12k members • Free

🏠 Lower Taxes w/ Ryan

1.3k members • $1/year

12 contributions to 🏠 Lower Taxes w/ Ryan

5d •

Material Participation

What pre-work activities for a specific deal prior to closing count towards your material participation hours? Also, is there a tool you would recommend to track that?

1 like • 5d

This is an interesting question because there doesn't seem to be any solid consensus on whether hours spent on a property before it is placed in service as a rental can count as material participation hours in that property. Those hours do count as real estate professional hours if you're going for that. But whether they count for material participation seems to be a subject of a lot of uncertainty. A lot of tax professionals say that you can't count hours as participating in an activity if the activity hasn't begun operations as a business yet. I believe Ryan has said in one of the podcasts that hours before the property is in service don't count for material participation, but I don't know if that has been his consistent position on that or if I understood his statement on that correctly. Other prominent real estate tax professionals seem to be split on this issue, some say yes and some say no.

6d •

Financial Software for STRs

Hi all, I'm a long time user of Quicken for my personal finance. I know, you can make fun of me - I get it! At any rate, it worked perfectly fine to run my part-time rental, part-time 2nd home through their Business & Personal software option. However, I'm a full-time real estate investor now, closing on my 2nd property next month, and am considering leveling up! With 1, soon-to-be 2 properties, and dreams of 2-3 more in the next 2-3 years, please answer my poll, I'd love to hear your POV as well as any commentary about why you recommend what you do. Could be from a tax / CPA perspective / real estate investor perspective / or small business owner perspective - I'd love to hear your thoughts! Thanks in advance, Josh

Poll

4 members have voted

2 likes • 5d

All you need is financial software that makes it easy to put transactions into categories. Quicken is actually just fine and does everything you need for rental real estate. But if you prefer to use a website, my next choice would be Baselane because it also does everything you need and it's free. REI Hub has a nice design, but personally I think the rental expense categories it uses are not ideal, but it's a totally fine option as well. The only one I would definitely not recommend would be Quickbooks. Quickbooks is fine if you're an accountant and you've taken the time to be trained in Quickbooks, and it's nice to be able to do fancy things like journal entries. But it's also slow, expensive, and just a pain to deal with compared to other options. When I have tax clients who have used QuickBooks, it's almost always a disaster and just a mess compared to something simpler like Baselane or REI Hub that is designed for rental real estate.

13d •

Filing an Extension on 2025 Taxes

Hi all, I'd heard that filing an extension can be beneficial, or at least common practice, for Real Estate Investors. Can anybody explain the rationale for doing so along with any requirements to do so? Thanks in advance, April 15 is around the corner!

1 like • 11d

It's a good practice to always file an extension even if you file your tax return on time, simply because the extension also extends the amount of time you have to file an amended return if you later discover any issues. For some types of elections that you can only make up until the extended due date of the return, it gives you until October to make those elections if you miss something. And for the final date to be able to amend the final return, it gives you another six months additional at the end of the usual three-year time span. And there's no reason not to file an extension.

29d •

OTA fee's for book keeping

I use Baselane for banking/ book keeping. It's been a great $0 option. Has all the reports and classifications I need. But I am stuck on OTA hos fee's. My OTA accounts deposit directly into the selected account. I assign the deposit as short term rent. The issue i have is this deposit is the net proceeds after the OTA has taken their cut. Accurate book keeping would show the full rental revenue (and cleaning fee's) then an expense for the OTA host fee. Do i need to make 2 additional entries for this? 1. Add the OTA host fee as rental revenue. 2. Add the OTA host fee as a commission expense? this would net to $0, but would help the revenue match the 1099 from the OTA's. Thanks for the help, sorry if this has been answered before. I did a search first and couldn't find anything. Bill

0 likes • 26d

There are going to be some numbers that are reported differently for tax purposes than what is in your bank ledger and your accounting software. It's ok if those things don't always match up, it gets sorted out when you or your accountant collect other documents for your taxes. For example, if your property taxes and/or insurance are paid by your mortgage company. I would just let Baselane track the net payout to your bank account. But when filing your taxes, you can look at the Airbnb earnings report and put on Schedule E what they report as the gross earnings, and their commission as an expense. And then if you want, you can double check that the net difference matches your Baselane report.

Mar 12 •

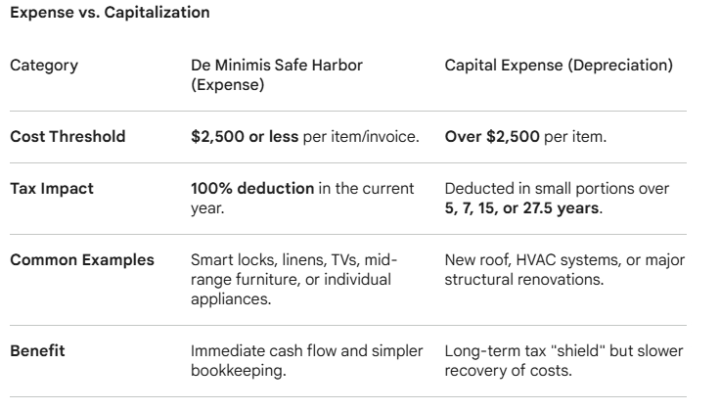

De Minimis Safe Harbor

Are there any gotcha's I should be aware of? I am DIY installing a mini-split in our garage game room conversion that costs about $2400 and want to expense the entire purchase. 'Essentially, this IRS provision allows you to immediately deduct (expense) the full cost of tangible property or repairs up to $2,500 per item, rather than depreciating those costs over several years as capital expenses. For an STR owner, this is incredibly useful when furnishing a new property or performing upgrades. Instead of "recovering" the cost of a $2,000 sofa over five or seven years, you take the full $2,000 hit against your income in Year 1. This lowers your taxable income right away, keeping more cash in your pocket for the next project. To leverage this, you must have an accounting policy in place at the beginning of the year stating you expense items under this threshold and formally "elect" the safe harbor on your tax return."

0 likes • Mar 18

No, there really aren't any catches to it. There may be unusual situations where maybe if your income is low this year, you would rather depreciate an item over a period of time rather than get the immediate expense in the current year. But most of the time, I would say it's to your advantage to use it when you can. Don't forget to include the election statement on your tax return.

1-10 of 12

@david-orr-4330

Real estate investor, and real estate tax pro at Tax Modern, specializing in tax consulting for rental property owners.

Active 11h ago

Joined Sep 27, 2025

Powered by