Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

Medical Courier Community

30.3k members • Free

Half Savage / Half Saint

82 members • Free

CLOSE -February '26 Mastermind

621 members • Free

Fundops

140 members • $99/month

Checkmate Picks

213 members • Free

42 contributions to Fundops

2d •

Insights into todays funding market

Grand rising tribe. We had something interesting happen yesterday that can benefit all Fundops clients.I had a personal friend whose son is in the NFL contact me for funding for his wife. Wife had over 50k in personal credit cards, 780+ Fico and a 2 year old LLC. MONTHS ago I shared with this friend the relationship banking process ( Seasoning bank accounts ) which never got established at the time. They went to chase yesterday , opened the business checking account , deposited 5k .... we introduced to the RM at CHASE and to my surprise, this client was only approved for 14k when I for sure estimated a 50-75k approval. I then went on to manually fill out the second application and to my surprise DECLINE! We called the reconsideration line for the banker to say , well you JUST opened a business checking account you were declined because we do not have enough information / data on the business. I share this with you guys because the relationship banking part of the process is one of the most crucial steps in getting larger approvals. Steps To Follow : 5-8 transactions monthly on the PRIME bank account we recommended If you can also get a payroll account and pay yourself from the business checking account bi weekly this adds points to your internal scores If you cannot, order checks and pay yourself bi weekly. All business transactions must run through this account with no negative days throughout the month Personal + Savings + Business Checking account with the lender goes a long way if you can. The market is changing , CHASE changed everything once again, we must get re committed , re focused to cross the finish line. Hope this helped =Your Funding Coach Timo

5 likes • 1d

Solid Insight 👊🏾

6d •

Financial Freedom July 30-Day Challenge

How it works: 🐺Week 1 (Jul 1-6): Post your "Freedom Declaration" your #1 financial goal for July (credit score target, first biz credit card, funding amount, etc.) 🐺Week 2-3: Post proof of action steps (screenshots of applications submitted, credit monitoring updates, bank account openings) 🐺Week 4 (Jul 28-31): Post your results vs. your declaration Finance Fridays bonus: Attend live = 2x points on that week's posts Prizes: 🏆Grand Prize — Free 1-on-1 strategy call with Timo + $100 cash 🏆2nd Place — Free month of credit monitoring + shoutout 🏆3rd Place —Fundops merch bundle or gift card Who's claiming the top spot in JULY? Drop a 🐺 if youre in.

5 likes • 6d

Solid Challenge 👊🏾🔥

19d •

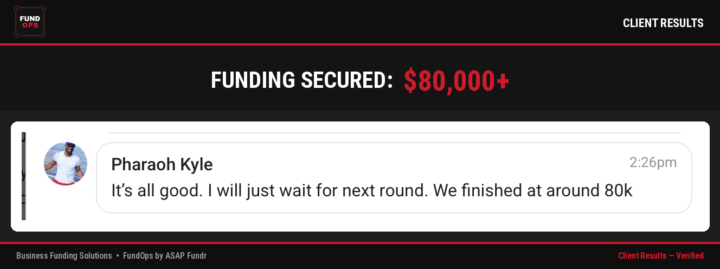

Fundops WIN!

Lets clap it up for @Pharaoh Kyle ! Finished at 80k on the first round. Would 80k of 0% biz credit take your biz to the next level?

5 likes • 18d

Congratulations 🎊 Looking forward to it once I'm in position 💸

23d •

🔥 No $15K Revolving History? You're Stuck. Here's the Fix.

Banks approve you based on your highest limits + revolving depth. Small limits = small approvals. That's why people get $500 store cards instead of $10K–$50K business lines. The $15K Primary Tradeline from Monetary Jewelers fixes that fast 👇 ✅ Reports as YOUR account (primary, not AU) ✅ Instantly raises your high-limit ceiling ✅ Deepens revolving history + drops utilization ✅ Fuels your business credit stacking The play — in order: 1️⃣ Grab the $15K primary 👉 http://monetaryjewelers.com/ (Code: T117W1) 2️⃣ Wait for it to report CLEAN — zero negatives 3️⃣ Then book Shaunt, our Chase banker 🏦 Don't book Shaunt early. Let it report clean first, THEN we capitalize. 🚀 Drop a 🙋 when yours reports and we'll get you on Shaunt's calendar.

4 likes • 23d

Solid 👊🏾🔥

28d •

What Lenders Look For To Approve

The intro to fundops virtual course is being recorded where clients can move ahead on their own time to expedite the process. If you would like a head start on the knowledge - attached is the presentation I will be teaching from. Lets win tribe, here to help and here to serve always. Drop a 🐺 if you're excited for the recent changes we have implemented.

3 likes • 27d

🐺

1-10 of 42

Active 1d ago

Joined Aug 11, 2025

Powered by