Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

Academy for Private Lending

36 members • Free

3 contributions to Academy for Private Lending

1 like • Jan 30

As a Buy and hold assuming good rental numbers it could work with less than 10K held in the property assuming an 80% LTV. As a flip its tight and financing fees and holding costs leave the margin less than 25K, less than my preferred return. There would need to be some other factor like a 2022 market or very desirable location to push me in the deal. From a lenders point of view Id need to be at a max loan of about 270,000 with 210,000 upfront. Buyer would need about 30000 to close with 60,000 in escrow. Buyer would still need 20,000 for the additional repairs. Not an ideal lending deal.

Jan 7 •

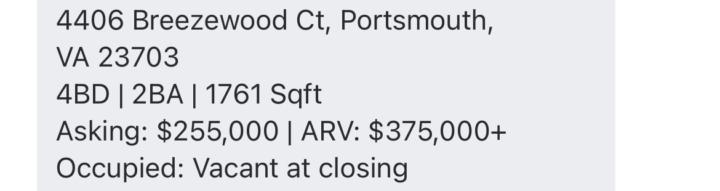

Let’s talk about if it’s a deal/ no deal to be the leader on

Let’s go through this from the number standpoint to show LTV, room for Rehab, would this be considered a safe loan?

1 like • Jan 12

$375,000 ARV is fair but at the high end of the area this home is in. Unable to tell what the repairs will cost but I have not been in a house yet that couldn't make 20,000 disappear! Underwriting at 75% LTV is 281,250 with 26250 toward renovations. Lending at 90% of 255,000 is $229,500. Escrow $51750. I don't know much about setting lending fees, but I've paid lots of them. Rate at 12% interest only + other fees and points of about 2% (5625). Assuming 4 months to turn $11248 interest. fees and interest = $16873 Return. It's a tight deal and I'm not sure the return is worth the risk. In this deal if everything goes well it works, but if the sale price is less or the marketing/renovation time expands the investors margin shrinks quick.

Dec '25 •

Welcome to the Community and lets get started

Please take a second to introduce yourself to the community and whats a starting question for you ?

0 likes • Dec '25

Thank you for the update. I look forward to learning and contributing.

1-3 of 3

Active 77d ago

Joined Dec 17, 2024