Activity

Mon

Wed

Fri

Sun

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

What is this?

Less

More

Memberships

Don't Buy Real Estate

309 members • Free

23 contributions to Don't Buy Real Estate

Jan 8 •

Buying a New Home Without Selling Your Current One

One of the biggest misconceptions I hear is“You have to sell your current home to buy the next one” That’s not always true. If structured correctly, you can turn your current home into a rental and still qualify for a new primary residence. Here’s what that can look like• Rent out your current home• Use a portion of that rental income to offset the mortgage• Qualify for a new home with as little as 5 percent down• Keep your first property as a long term investment Lenders don’t automatically count two mortgages against you when rental income is documented properly. This is how many homeowners slowly build wealth without overextending themselves. If you’re curious whether this works for your situation, ask below or message me. Happy to break it down.

Dec '25 •

Seller Concessions Explained Simply

Seller concessions are one of the most underused tools buyers have right now. In today’s market, homes are sitting longer, which means sellers are more open to covering certain costs to get deals done. Depending on the loan type, concessions can help pay for closing costs, prepaid taxes and insurance, interest rate buydowns, and in some cases even repairs. VA, FHA, and Conventional loans all have different rules and limits, which is why strategy matters. This is where working with the right lender and agent can change the entire outcome of a deal. If you’re buying or advising buyers, understanding seller concessions can save real money and open doors that feel out of reach at first glance.

3

0

Dec '25 •

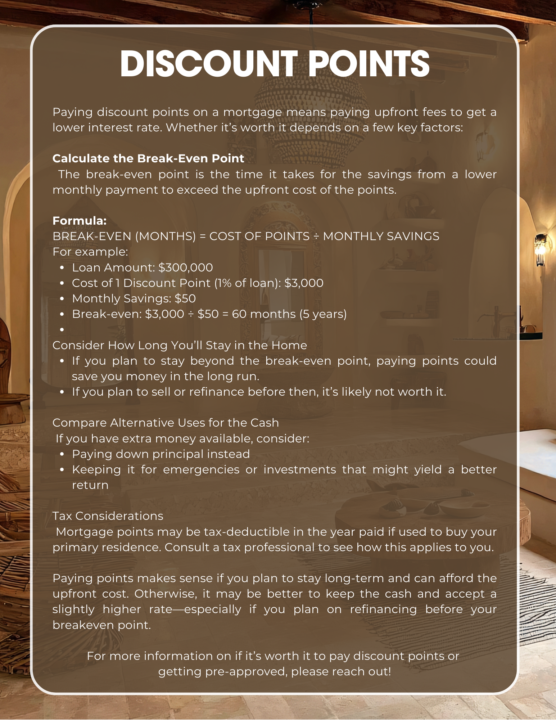

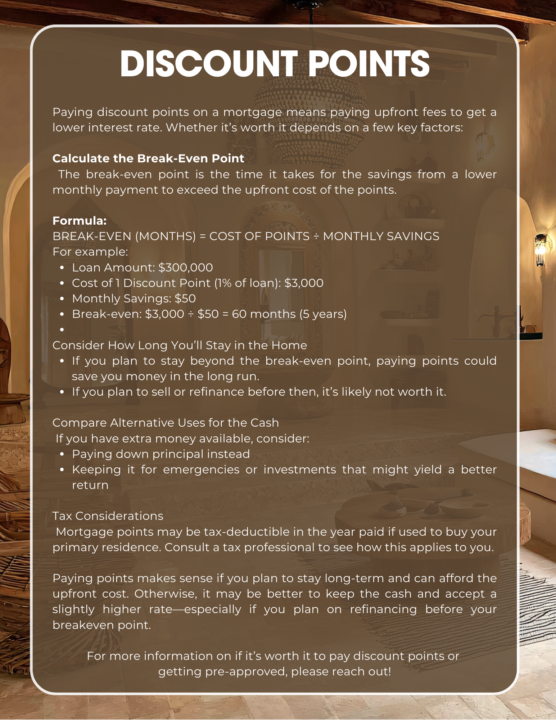

Should You Pay Discount Points?

Discount points can lower your interest rate but they come with an upfront cost. The real question is not “Is the rate lower?” it is “How long am I keeping this loan?” If you sell or refinance before the break even point you likely never see the benefit.If you plan to stay long term it can be a smart move. This is why strategy matters just as much as the rate. Always run the numbers before deciding.

3

0

Dec '25 •

Quick mortgage myth-buster

Paying discount points is not automatically “smart” or “bad” — it’s a math decision. The real question is your break-even point.If the monthly savings don’t outweigh the upfront cost before you sell or refinance, the points didn’t do their job. Simple rule of thumbCost of points ÷ monthly savings = months to break even If you plan to stay long-term, points can make senseIf you plan to move or refinance sooner, cash may be king This is exactly why strategy matters more than rate shopping. Drop a 🧮 if you want help running your numbers.

4

0

Dec '25 •

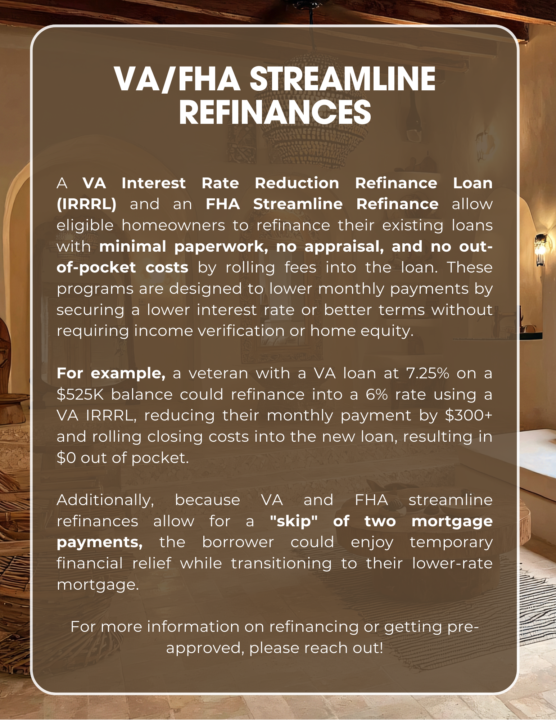

VA and FHA Streamline Refinances Explained

If you currently have a VA or FHA loan, you may be able to lower your interest rate, reduce your monthly payment, and skip two mortgage payments without the hassle of an appraisal or full documentation. A Streamline IRRRL (VA) or FHA Streamline Refi lets eligible homeowners refinance quickly with minimal paperwork and no out-of-pocket costs, since fees can be rolled into the new loan. These programs are designed for one thing: helping homeowners secure better terms without income verification or home equity requirements. For example, a veteran with a 7.25 percent rate could refinance into a 6 percent rate, save $300 plus monthly, and transition smoothly into their new payment. If you want to explore whether you qualify or want to run scenarios, I’m here to help. Drop your questions in the comments or message me directly.

2

0

1-10 of 23

@randa-dehaan-7168

San Diego based

Mortgage Lender

Aspiring real estate investor

Active 26d ago

Joined Jun 8, 2024

Powered by