Write something

13d •

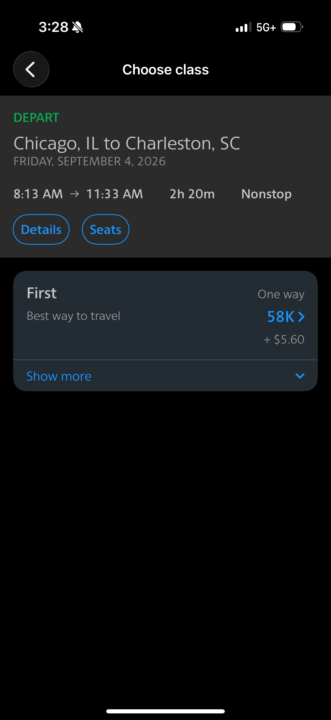

The $0 Charleston Weekend: How a Junior Suite, First-Class Flights, and a Sold-Out Resort All Bent to a Better Strategy✈️🏨

There is a particular kind of silence that settles over a points enthusiast when a dream booking refuses to materialize. It is the silence of refreshing an award calendar at 6 a.m. with a cup of coffee gone cold, watching the same blank availability stare back day after day. For weeks this spring, that was the soundtrack of my mornings. The destination was Charleston, South Carolina. The occasion was the annual Points and Miles Credit Card Meetup, scheduled for September 4–6 at the Wild Dunes Resort, a Hyatt property tucked along the Isle of Palms just north of the city. For anyone serious about loyalty programs, this is the kind of weekend you do not miss. The location, however, had other ideas. The Wall My search began in early May, comfortably ahead of the booking deadline. Hyatt is generally one of the more generous transfer partners in the ecosystem, and I expected the kind of low-friction redemption that makes Hyatt loyalists insufferable at dinner parties. Instead, I found nothing. Day after day, the award calendar held firm. The cash rate, meanwhile, hovered at $569 per night for a standard king. Across the two-night stay, that came to $1,514.01. Paying that figure was never on the table. The whole point of building a points portfolio is to refuse prices like that on principle. I began plotting a fallback. Downtown Charleston, roughly thirty minutes inland from Wild Dunes, offered more inventory and a chance to deploy resources I already had in reserve, namely three Fine Hotels & Resorts credits and a $300 Citi Strata Elite credit. It was a workable plan. It was not, however, the plan I wanted. The whole appeal of the meetup is staying where the meetup happens. I gave myself until the end of May. The Break On May 19, a junior suite appeared. Two nights, 62,000 Hyatt points, both dates of the meetup. There was no time to deliberate. I logged into my Bilt account, where I had been parking points specifically for moments like this one, and transferred 60,000 to Hyatt. Combined with the roughly 3,000 points already sitting in my account, the booking went through in less time than it takes to brew a pot of coffee. Five minutes, start to finish.

0

0

Apr 26 •

Chargebook: The Credit Card Tracker You've Been Missing (Coming Soon)

If you're someone who carries multiple credit cards — and especially if you're deep in the points and rewards game — you already know the pain. You've got due dates scattered across different apps, benefit credits you keep forgetting to use, and no clean way to see everything in one place. That's exactly the problem Chargebook was built to solve. What Is Chargebook? Chargebook is a personal credit card management app designed for people who take their credit cards seriously. Whether you're managing two cards or twenty, Chargebook gives you a single clean dashboard to track balances, monitor credit utilization, stay on top of due dates, and make sure you're actually using the benefits you're paying for. Think of it as the app Wallet Balance should have been — but built specifically for credit cards, with the depth and intelligence that serious cardholders actually need. The Problem It Solves Most credit card users are leaving money on the table every single year. Not because they're bad with money — but because the tools available to them aren't built for the way they actually use cards. Here's what typically happens. You pay a $695 or $895 annual fee on a premium card. That fee comes with hundreds of dollars in credits — airline credits, dining credits, hotel credits, streaming credits, and more. But because those credits are spread across different categories, reset at different times of the year, and tracked nowhere in one place, most people forget to use them. That money just disappears. At the same time, you've got multiple due dates to track, statement dates that affect your credit score, and anniversary dates that trigger benefit resets — all living in different places, none of them talking to each other. Chargebook fixes all of that. What Chargebook Does Balance Tracking That Actually Makes Sense When you log a charge in Chargebook, your balance goes up. When you log a payment, your balance comes right back down. The app always shows you exactly what you owe on each card and how much available credit you have left — in real time, as you use it.

0

0

Apr 20 •

ONE FREE NIGHT CERTIFICATE. ONE ANNIVERSARY. ONE UNFORGETTABLE NIGHT AT THE WALDORF ASTORIA CHICAGO.

There is a particular kind of satisfaction that comes from walking up to a world-class hotel knowing you're not paying for the room. That is exactly how I felt on the evening of April 24th, 2026, when my wife and I pulled into the entrance of the Waldorf Astoria Chicago for our one-year wedding anniversary. No room charge waiting at checkout. No mental math on whether it was worth it. Just valet, champagne, a terrace overlooking the city, and a night that neither of us will forget. This is the story of how a single card benefit — one that most Aspire cardholders either don't know about or never use — paid for a room that runs $800 to $1,000 a night. THE DECISION We have a 10-month-old. That changes everything about how you travel. Long international itineraries are a different kind of planning now — but a one-night escape to somewhere truly exceptional? That felt not only achievable, but necessary. My wife had never stayed at a Waldorf Astoria. For our first anniversary, that felt like the right way to celebrate — Hilton's flagship brand, one of Chicago's most iconic luxury properties, and a night that stood apart from the ordinary. I pulled up the Hilton website and found the Deluxe King with Fireplace running $869.46 for April 24th. My first instinct was to apply the Fine Hotels and Resorts $300 credit from the Amex Platinum. Then I remembered something I hadn't touched yet: the Free Night Certificate on my Hilton Aspire card. THE MATH The Hilton Aspire issues a Free Night Certificate every year after your card anniversary date. It posts 8 to 12 weeks after your annual fee hits and is valid for 12 months. The FNC is uncapped — meaning it covers any standard room regardless of the nightly cash rate — and must be redeemed by calling Hilton directly, not online. My anniversary month is May. I had a certificate about to expire. I made the call. The Deluxe King with Fireplace at the Waldorf Astoria Chicago — a room running $869.46 that night — was booked for $0.

0

0

Apr 15 •

THE AMERICAN CLUB: HOW WE TURNED ONE AMEX CREDIT INTO A LUXURY THANKSGIVING ESCAPE FOR $225

There is something quietly powerful about walking into a five-diamond resort in the middle of a snowstorm knowing you paid a fraction of what the room is worth. That was the feeling my wife and I had on the evening of November 26th, 2025, when we pulled up to The American Club in Kohler, Wisconsin — exhausted from a three-hour white-knuckle drive through the season's first blizzard, and completely floored by what was waiting for us on the other side of those doors. This is the story of a one-night Thanksgiving getaway that cost us $225.47 out of pocket — on a trip worth $625.47 in real value. And it all came down to one card benefit most people never use correctly. THE DECISION My wife and I have a five-month-old son. That alone changes the calculus on travel. Long international trips require a different kind of planning now — but a one-night escape to somewhere genuinely special? That felt achievable. We had heard about The American Club through the Fine Hotels and Resorts program on our Amex Platinum. A quick search confirmed why it had earned its reputation. The Midwest's only AAA Five Diamond Resort Hotel. A member of Historic Hotels of America. Consistently ranked among the Top 100 Golf Resorts in the world. And it sits just two hours from home in Kohler, Wisconsin — the headquarters of Kohler Co., the iconic American manufacturer best known for its kitchen and bath products. The date was set for November 26th — the night before Thanksgiving, with family plans locked in for the 27th. One night. One great hotel. A chance to breathe before the holiday. THE MATH BEFORE THE TRIP Room rate for November 26th: $391.17. Here is where the strategy starts. Every American Express Platinum card comes with a $600 annual Fine Hotels and Resorts credit — split as $300 in the first half of the year and $300 in the second. To receive the credit, you book through the FHR program and pay in full upfront. Amex reimburses the $300 to your account within a few days. I used maxfhr.com to locate the property and confirm FHR

0

0

Apr 15 •

U.S. Bank Cash+ — The 5% Cash Back Card I Quietly Profit From Every Month

There’s a difference between a flashy credit card and a profitable one. The U.S. Bank Cash+® Visa Signature® Card isn’t going to impress anyone at a dinner table. It’s not a luxury travel card. It doesn’t come with airport lounges or elite status. But from a business and personal finance standpoint?This is one of the most strategically valuable cash back cards I carry. And I’ll be honest—I use this card every single month for two things: My energy bill My gym membership That alone tells you everything you need to know. Why I Keep This Card in My Wallet This card fills a gap that most cards completely ignore. Most credit cards focus on: - Dining - Travel - Groceries But what about the bills you have to pay no matter what? That’s where this card steps in—and starts producing real returns. The Multipliers (Where the Real Money Is Made) Let’s break it down the way it actually matters. 5% Categories — The Core Strategy Every quarter, I choose two categories where I earn: - 5% cash back on up to $2,000 per quarter (combined) Categories include: - Utilities (this is where my energy bill goes) - Gym/fitness centers (this is where my membership goes) - Internet & streaming - Cell phone bills - Electronics stores - Fast food and more This is where the card becomes powerful. Most people overlook these categories—but these are fixed expenses. You’re paying them anyway. So instead of money going out with no return, I’m pulling 5% back on bills I can’t avoid. 2% Category — The Secondary Lane You also choose one category for: - 2% cash back (unlimited) Options include: - Gas - Groceries - Dining I treat this as a backup—not the main driver. 1% Everything Else Anything outside those categories earns 1%, which is why this is not a “main spending” card. This is a targeted-use card, not an everyday card. Credits & Value Add (Simple but Effective) This isn’t a credit-heavy card like premium products, but it still delivers value where it counts.

0

0

1-30 of 33

powered by

skool.com/the-upgrade-life-9567

Learn how to earn, transfer & redeem points and miles to travel better and pay less. Beginner friendly. New lessons weekly.

Suggested communities

Powered by