Write something

2d •

Portfolio Change +$IWM -$XLV -$TLT

We went long $IWM (small caps), closed the $XLV (healthcare) after a few days, and exited $TLT. Added long exposure in $QQQ and $SPY. I like watching how the portfolio behaves, especially during market selloffs. Being positioned to go long VXX into crashes doesn’t always hit, but when it does, staying positive while the market is red feels great.

0

0

2d •

Myth #6: "The 4% Retirement Rule Always Works"

"Retire on the 4% rule and hope you don't hit a bear market in year one." Hope is not a strategy. Proper allocation is. The 4% rule works IF your portfolio is allocated efficiently. A random 60/40 works 95% of the time. A PNL-weighted portfolio works 97-98% of the time. The difference? When the market crashes, your optimized allocation recovers faster because you're allocated for recovery, not just diversification. Don't retire on theory. Retire on a proven allocation with proven recovery mechanics. PNL's weights are designed for both growth AND stability. That's why they work through crashes. The rule isn't magic. The allocation is.

0

0

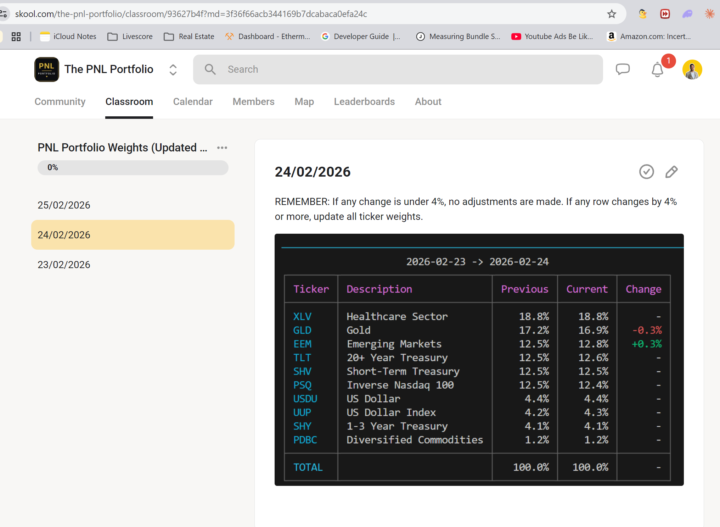

2d •

Where can I find the weights?

You will see it in the classroom it will be updated daily market open/before market close https://www.skool.com/the-pnl-portfolio/classroom/93627b4f

0

0

4d •

Myth #5: "You Need $500K to Invest Properly"

"I can't invest properly until I have $500K saved." You're backwards. Start now. PNL's allocation works at $5K just as well as it works at $500K. The weights scale perfectly. You don't need massive capital. Waiting to accumulate $500K means you miss years of 32% CAGR compounding. Start with $5K. Rebalance the same. Own the same percentages. Compound the same way. At 32.19% CAGR, every year you wait costs you massively. Start now. Your portfolio isn't about the size of your position. It's about the consistency of your allocation. Start now. Size doesn't matter. Weights do.

0

0

4d •

Myth #4: "Bonds Are Dead"

Tell that to the people who needed to rebalance into stocks during crashes and couldn't because they panicked. Bonds aren't sexy. They're not supposed to be. They're stability. SPY lost -33.72% at its worst. PNL's worst drawdown? -6.78%. Our worst year was still +4.62%. That's the difference proper allocation makes. When markets crash, bonds perform. You have cash flow to live on. You can rebalance into stocks mechanically without emotional override. You sleep. The people who hate bonds are the ones who never needed them. The people who own them smile during crashes because they can BUY the dip, not PANIC SELL. PNL allocates bonds for reasons. Ignore them at your own expense.

0

0

1-11 of 11

skool.com/the-pnl-portfolio

Passive income from the stock market targeting 30%/year. Follow the trades, go hands off, or learn how. One portfolio. One community. Join us 👇

Leaderboard (30-day)

1

+1

Powered by