6d •

Last month I finally stopped guessing where my money went.

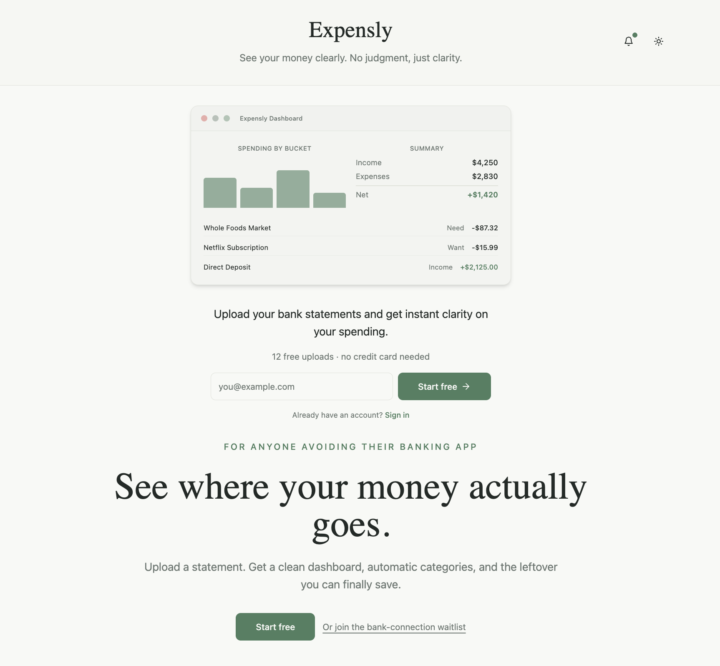

I uploaded my June bank statement into the app I've been building — no spreadsheet, no manual sorting. It read the statement and sorted every transaction into Need, Want, Dream, or Fix, then flagged a few recurring charges I'd honestly forgotten I was paying for. Took less than a minute. Your statement gets processed once and is never stored. If you want to see your own numbers laid out the same way, you get 12 free uploads, no card required: https://expenslyfinance.lovable.app/ Try it on last month's statement and drop your Need/Want/Dream/Fix split in the comments... https://youtu.be/Qu5xbkR-7Skcurious what everyone's "Fix" category looks like.

13d •

July budget setup. Five steps, fifteen minutes.

Pull June. That's your baseline, and today's the last day of the month, so the timing is right to look back before you move forward. Add what's specific to July. The Fourth, a trip, a wedding, a getaway, a concert. If it's already on the calendar, build it into the budget now. Check the savings goals. We're at the halfway mark of 2026: are you on pace with what you set out to save this year? If not, this is the checkpoint to adjust, not the moment to panic. Set up or top off the summer sinking funds. Travel, gifts, events. If they exist, fund them. If they don't, start them today. Automate the thing you've been putting off. A transfer into savings, a sinking fund, an investment account. Set it once, stop thinking about it monthly. Before you build June's numbers from memory, get the real ones. Try Expensly to see what you actually spent last month: it gives you the anchor this whole process depends on. Try Expensly: https://expenslyfinance.lovable.app/

Jun 9 •

Hobby or Business - The IRS Refreshes a Few Questions

Tax Tip 2026: Is it a Hobby or a business? The IRS just clarified the tax differencehttps://app.heygen.com/videos/sba-grocery-guarantee-are-you-loan-ready-0abcb1e027924031809440a5c8ffb923 between a hobby and a business - which one are you? SBA Freedom250: $1 Million Cash Prize Competition - Submit by Tuesday The SBA is awarding a $1M prize pool to entrepreneurs through the Freedom250 pitch competition. $30 million in loans now available via 90% Grocery Guarantee Small Business in food production, distribution, and retail can access SBA backed loans through the enhanced 90% Grocery Guarantee. Find out if this is for you NAV loan requirements complete guide to qualifying in 2026. NAV Breaks down updated SBA loan requirements including rule changes effective March 1, 2026. A reliable resource can be found here. Imposter scam losses jumped 20% - $3.5 billion lost in 2025 Government imposter scams are up 40% with fraudsters faking toll programs and threatening registration suspension. Stay Informed

0

0

Jun 6 •

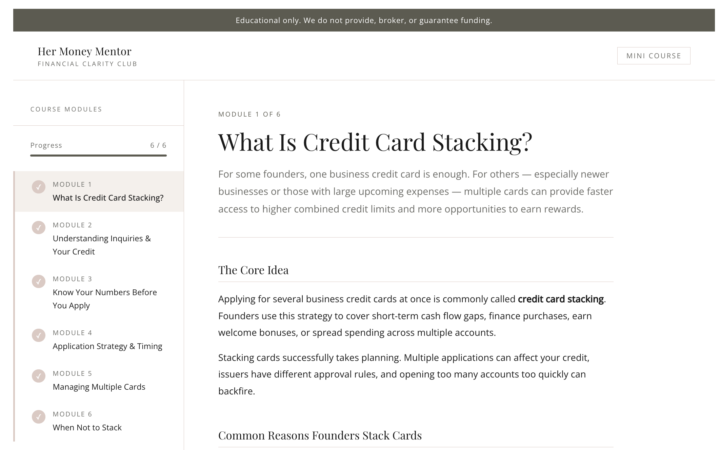

New resource inside the community — Business Credit Card Stacking

A lot of my clients are asking about Credit Card Stacking Lately, and there's a lot of prep work required to qualify actually! So I put together a short, self-paced course walking through how credit card stacking works as a business financing strategy. It covers: — What stacking is and why some founders use it — How hard inquiries work and what different issuers typically pull — What documents to have ready before you apply — How to sequence and time applications — How to manage multiple cards once you have them — When this strategy does not make sense for your situation It is six modules, built from a single source, no fluff. Each module has a checklist or reference table you can actually use. You can find it here This is for educational purposes. I do not provide, broker, or guarantee funding.

3

0

May 25 •

You did everything right.

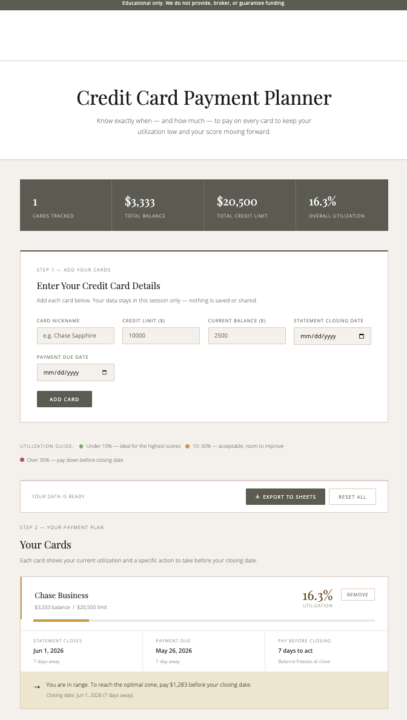

You paid on time. Every month. Never missed a payment. And your score barely moved. That was me trying to figure out what I was missing. I kept doing the thing I was told to do and kept getting the same result. On time, every month, like clockwork. And still watching that number sit there like it owed me nothing. I started digging. Not because I had extra time. I had a W-2, a side hustle I was trying to grow, and a list of things I needed credit to actually do. A business card. A lease. Room to breathe. I needed my credit to reflect what I was building, not just prove I could hit a due date. That is when I found out that the due date is not the date that matters. There is a date that happens before that. Your statement closing date. That is the date your card reports your balance to the credit bureaus. Whatever your balance is on that day, that is what gets recorded. That is what your utilization is calculated from. Not what you pay by the due date. The closing date. I sat with that for a minute. Because I had been paying on time for months. Doing everything right. But I was paying after my balance had already been reported. My score was seeing a high balance every single month before I ever touched it. Nobody told me that part. The advice is always "pay on time and keep your utilization under 30%." But there is a step missing in the middle of that sentence. The step where you actually know what date your balance gets locked in. The step where you know exactly how much to pay, and by when, to hit whatever target you are going for. Without that, the advice is just noise. It is like someone telling you to be on time but never giving you the address. So I started paying before the closing date. Not a random amount. A specific number. The exact dollar amount that would bring my balance to under 10% of my limit before that date hit. And things started moving. Not overnight. But they moved. Because I finally had the full picture instead of half of it. Here is what I kept thinking about after that.

0

0

1-30 of 33

skool.com/skool-of-financial-literacy

Position your business for approvals by separating your personal and business expenses.

Powered by