Write something

Mar 12 •

The Biggest Misunderstanding About the Fair Credit Reporting Act ⚖️

There's one thing I see people get wrong about the Fair Credit Reporting Act more than anything else — and it's usually the reason their disputes go nowhere. Drop what you think it is below. I'll share mine and break it down.

Mar 6 •

Leverage the Fair Credit Reporting Act 🚀

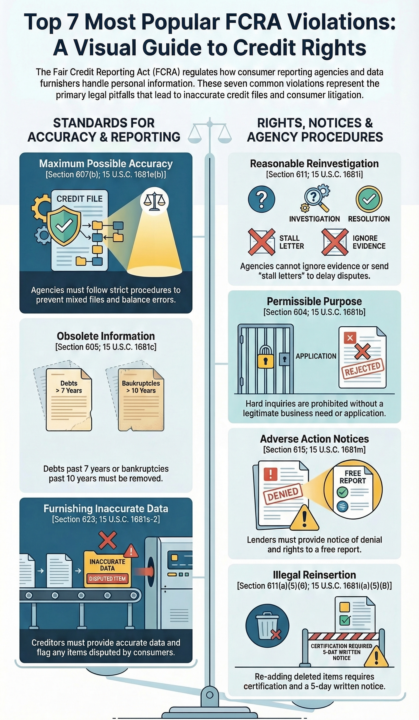

The FCRA is the bread and butter of disputing. Below are the most common violations commited by credit bureaus and furnishers: 𝟭. 𝗙𝗮𝗶𝗹𝘂𝗿𝗲 𝘁𝗼 𝗔𝘀𝘀𝘂𝗿𝗲 "𝗠𝗮𝘅𝗶𝗺𝘂𝗺 𝗣𝗼𝘀𝘀𝗶𝗯𝗹𝗲 𝗔𝗰𝗰𝘂𝗿𝗮𝗰𝘆" (𝗦𝗲𝗰𝘁𝗶𝗼𝗻 𝟲𝟬𝟳(𝗯)) This is perhaps the most fundamental violation. Whenever a consumer reporting agency (CRA) prepares a report, it is legally mandated to follow 𝗿𝗲𝗮𝘀𝗼𝗻𝗮𝗯𝗹𝗲 𝗽𝗿𝗼𝗰𝗲𝗱𝘂𝗿𝗲𝘀 𝘁𝗼 𝗮𝘀𝘀𝘂𝗿𝗲 𝘁𝗵𝗲 𝗺𝗮𝘅𝗶𝗺𝘂𝗺 𝗽𝗼𝘀𝘀𝗶𝗯𝗹𝗲 𝗮𝗰𝗰𝘂𝗿𝗮𝗰𝘆 of the information concerning the individual. • 𝗖𝗼𝗺𝗺𝗼𝗻 𝗩𝗶𝗼𝗹𝗮𝘁𝗶𝗼𝗻: Bureaus often fail this standard by 𝗺𝗶𝘅𝗶𝗻𝗴 𝗳𝗶𝗹𝗲𝘀 of consumers with similar names, reporting 𝗶𝗻𝗮𝗰𝗰𝘂𝗿𝗮𝘁𝗲 𝗮𝗰𝗰𝗼𝘂𝗻𝘁 𝗯𝗮𝗹𝗮𝗻𝗰𝗲𝘀, or allowing "𝘁𝗲𝘁𝗵𝗲𝗿𝗲𝗱" 𝗽𝗲𝗿𝘀𝗼𝗻𝗮𝗹 𝗶𝗻𝗳𝗼𝗿𝗺𝗮𝘁𝗶𝗼𝗻 (like misspelled names or old addresses) to remain, which prevents old errors from being removed. As we discussed, reporting a collection trade line before an original creditor has even charged off the account is a clear factual inconsistency that violates this standard. 𝟮. 𝗙𝗮𝗶𝗹𝘂𝗿𝗲 𝘁𝗼 𝗖𝗼𝗻𝗱𝘂𝗰𝘁 𝗮 "𝗥𝗲𝗮𝘀𝗼𝗻𝗮𝗯𝗹𝗲 𝗥𝗲𝗶𝗻𝘃𝗲𝘀𝘁𝗶𝗴𝗮𝘁𝗶𝗼𝗻" (𝗦𝗲𝗰𝘁𝗶𝗼𝗻 𝟲𝟭𝟭) If you dispute the completeness or accuracy of an item, the bureau must conduct a 𝗿𝗲𝗮𝘀𝗼𝗻𝗮𝗯𝗹𝗲 𝗿𝗲𝗶𝗻𝘃𝗲𝘀𝘁𝗶𝗴𝗮𝘁𝗶𝗼𝗻 to determine the current status of that information. • 𝗖𝗼𝗺𝗺𝗼𝗻 𝗩𝗶𝗼𝗹𝗮𝘁𝗶𝗼𝗻: Agencies frequently violate this by 𝗶𝗴𝗻𝗼𝗿𝗶𝗻𝗴 𝗿𝗲𝗹𝗲𝘃𝗮𝗻𝘁 𝗲𝘃𝗶𝗱𝗲𝗻𝗰𝗲 submitted by the consumer or by sending "𝘀𝘁𝗮𝗹𝗹 𝗹𝗲𝘁𝘁𝗲𝗿𝘀" that claim a dispute is "frivolous" without providing the specific reasons or documentation required to proceed. Legally, the presence of contradictory information in your file is not enough for them to label your dispute as frivolous. 𝟯. 𝗥𝗲𝗽𝗼𝗿𝘁𝗶𝗻𝗴 𝗢𝗯𝘀𝗼𝗹𝗲𝘁𝗲 𝗜𝗻𝗳𝗼𝗿𝗺𝗮𝘁𝗶𝗼𝗻 (𝗦𝗲𝗰𝘁𝗶𝗼𝗻 𝟲𝟬𝟱) The FCRA generally prohibits CRAs from including negative information in a report that is too old. • 𝗖𝗼𝗺𝗺𝗼𝗻 𝗩𝗶𝗼𝗹𝗮𝘁𝗶𝗼𝗻: This usually involves "𝗿𝗲-𝗮𝗴𝗶𝗻𝗴" 𝗱𝗲𝗯𝘁𝘀, where a collector or bureau reports a delinquency date that is more recent than the actual date of the first delinquency. Most adverse information, including 𝗰𝗼𝗹𝗹𝗲𝗰𝘁𝗶𝗼𝗻𝘀 𝗮𝗻𝗱 𝗰𝗵𝗮𝗿𝗴𝗲-𝗼𝗳𝗳𝘀, must be removed after 𝘀𝗲𝘃𝗲𝗻 𝘆𝗲𝗮𝗿𝘀. Bankruptcies (specifically Chapter 7 or 11) have a longer limit of 𝟭𝟬 𝘆𝗲𝗮𝗿𝘀.

0

0

Mar 3 •

What can I do to give my disputes and CFPB complaints the most LEGAL POWER?

Under the Fair Credit Reporting Act (FCRA), both consumer reporting agencies (bureaus) and furnishers (creditors/collectors) have specific statutory duties to review the information you provide. 1. Information Required for Direct Disputes (with Furnishers) When disputing directly with a creditor or collection agency, the law is very specific about what you must provide to trigger their duty to investigate. Pursuant to FCRA Section 623(a)(8)(D), your dispute notice must: - Identify the specific information that is being disputed. - Explain the legal or factual basis for your dispute. - Include "all supporting documentation" required by the furnisher to substantiate your claim. Advice: You should definitely send copies of your credit report with the errors clearly marked or circled. This satisfies the requirement to identify the specific information in dispute. 2. Information Required for Bureau Disputes When you submit a dispute to a credit bureau, they are legally mandated to "review and consider all relevant information submitted by the consumer" during the reinvestigation period. Furthermore, the bureau is required to provide notification of your dispute to the furnisher, which must include "all relevant information regarding the dispute" that the bureau received from you. Advice: To ensure the bureau cannot dismiss your dispute as "frivolous or irrelevant," you must provide sufficient information for them to investigate. This includes: - Proper Identification: The bureau may require you to furnish "proper identification" (such as a government ID or utility bill) as a condition of conducting the investigation. - Evidence of Accuracy: If you are disputing a balance or payment status, include account statements or payment receipts as "relevant information" the bureau must consider. 3. Submitting Previous Letters to the CFPB When escalating a matter to the Consumer Financial Protection Bureau (CFPB), providing copies of your previous correspondence with the credit bureaus is highly effective.

2

0

1-3 of 3

powered by

skool.com/ai-logic-credit-repair-2026-1199

AI-powered credit repair education — free to join. Members get 60% off the full Credit Control Lab platform.

Suggested communities

Powered by