Activity

Mon

Wed

Fri

Sun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Memberships

Cloud Residents · US Credit

1k members • Free

52 contributions to Cloud Residents · US Credit

12d •

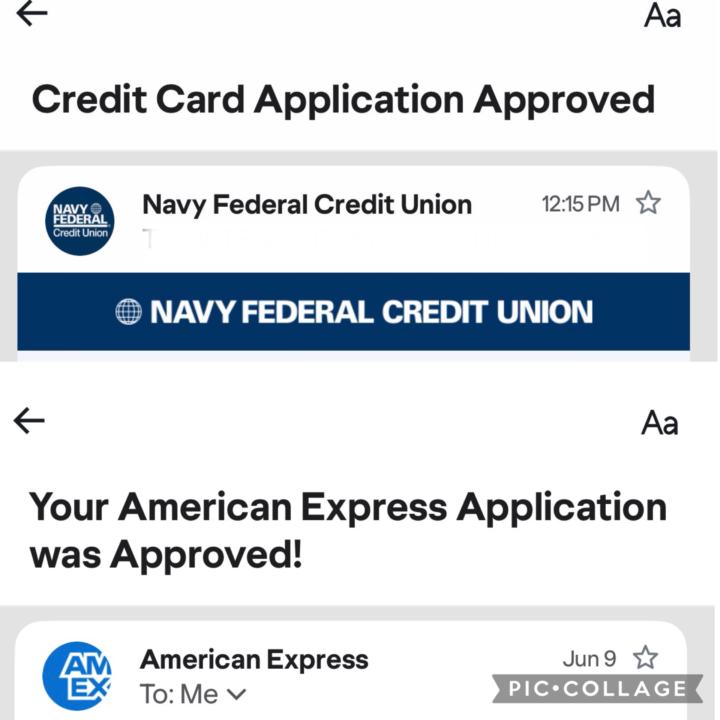

Amex and Navy Fed Card approved

Happy to share that I was approved for the Navy Cash Rewards & Amex BC Everyday card. Both has 0% intro APR for 12 and 15 months for BT and Purchases. I only have 1 year of ITIN history. Thanks, guys for sharing your knowledge here :) I will maximize the 0% APR 🤸🏻♂️ Ps: I don’t have any DD or Pledge loan in Navy Fed. Waited 3months from the date of account opening from them before tried applying for their card.

0 likes • 12d

Congratulations! How are the credit limits on both cards?

23d •

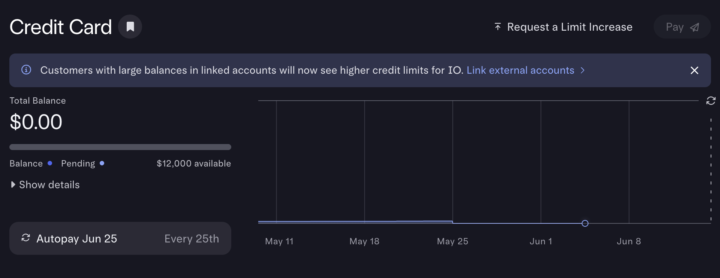

Mercury IO Card Update

Now, you can connect your EXTERNAL personal or business account and that will count towards your daily balance of Mercury and your IO limit will increase I came to know about this today only and connected my personal account. Have you tried it? 🔥

0 likes • 23d

My Mercury Bank account was just closed 😂

0 likes • 23d

@Apple Service I only made a few small personal deposits into the account, with no significant transactions, and then a few days ago I received an email saying they'd decided to close the account. 😂

1 like • 24d

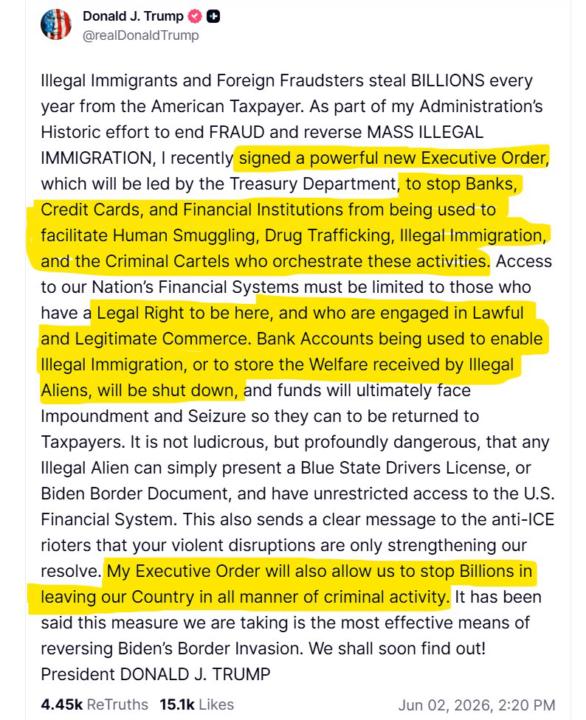

While opposition parties, civil rights groups (like the ACLU), and blue-state Attorneys General typically push back against such executive orders, we haven't seen a massive, system-wide block yet due to several legal and procedural reasons: Guidelines are not yet finalized (No ripe harm): The executive order currently only "directs" the Treasury and regulators to draft rules. In the U.S. judicial system, a lawsuit requires "standing." This means plaintiffs must prove they have suffered a concrete, actual injury. Because the specific banking enforcement rules have not yet been published—and banks haven't started shutting down accounts en masse—any lawsuit filed by civil rights groups or prosecutors right now would likely be dismissed by a judge as "not ripe." Resistance and lobbying from banks: Instead of jumping straight into lawsuits, Wall Street and major banks usually work to "soften" policies through compliance reviews and industry lobbying. For banks, forcing a review of the immigration status of millions of customers incurs massive administrative costs and could potentially violate existing federal anti-discrimination laws, such as the Equal Credit Opportunity Act. Therefore, financial institutions themselves will push back during the rulemaking phase to prevent the final policies from being too radical. Internal "disclaimer" clauses in the EO: The text of this executive order includes a standard disclaimer stating that the order "is not intended to, and does not, create any right or benefit, substantive or procedural, enforceable at law or in equity by any party against the United States, its departments, or agencies." This means it is an internal administrative directive rather than an immediately enforceable civil judgment. Summary The counterattack from various U.S. sectors is unfolding systematically. At this stage, immigration advocacy groups and legal experts are primarily urging the public to remain calm and advising individuals not to panic-withdraw or close their bank accounts based on scare tactics on social media.

May 20 •

Presidential Executive Order

(ii) institutions maintain the authority, where warranted by other risk indicators or supervisory concerns, to obtain additional information necessary to resolve material compliance concerns, including information relevant to whether account holders possess lawful immigration status and employment authorization in the United States when such information is relevant to assessing risks associated with fraud, identity misrepresentation, sanctions evasion, or other illicit financial activity, as part of a risk-based customer due diligence program. https://www.whitehouse.gov/presidential-actions/2026/05/restoring-integrity-to-americas-financial-system/

1 like • May 20

@Daniel Johnson This could lead to stricter regulations or KYC procedures; the impact is currently unclear.

0 likes • May 20

@Apple Service Indeed, I hope it won't have too much of an impact.

May 19 •

Equifax vs FICO: The Truth

Most people building US credit start with Equifax or Credit Karma. It's free, it's easy, and it feels like you're tracking your progress. Here's the problem: that number you're looking at is probably not the one your lender sees. Equifax/Credit Karma = VantageScore Credit Karma shows your VantageScore 3.0 or 4.0 from Equifax. Completely free, yes. But over 95% of lenders don't use it. And the kicker: your VantageScore typically runs 20 to 60 points higher than your actual FICO score. That gap is the difference between an approval and a denial. What Lenders Actually Pull FICO scores. Whether you're applying for a credit card, a car loan, or a mortgage, the lender pulls your FICO. Not VantageScore. Not Credit Karma. Not the score Equifax shows you. For Cloud Residents building credit with an ITIN, this hits harder. You're working with a thinner file, fewer accounts, shorter history and no proper channels to monitor your FICO. How to See Your Real Scores Platforms like myFICO let you view real scores. These are the same numbers lenders pull when you apply. The Play Use Credit Karma or Equifax as a baseline monitor. It's fine for watching report changes, new accounts, and inquiries Before you apply for anything, check your actual FICO. Know the real number, not the inflated one The gap between your VantageScore and FICO tells you exactly where you stand The difference might surprise you. See you in comments, Ain - Cloud Resident

Poll

30 members have voted

1 like • May 19

My EQ app shows scores of around 689 from three credit bureaus, FICO's EQ score is 737, TU's score is 720, and I cannot find the EX score.

1-10 of 52