Activity

Mon

Wed

Fri

Sun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

What is this?

Less

More

Owned by Richard

Set up, protect, and optimize your 1099Anesthesia income:Taxes, entities, contracts, & rates. Find the leaks.Make the leap. Create your leverage.

Memberships

Claude Code Club

4.7k members • $9/month

Skoolflow

230 members • Free

Community Builders - Free

11.1k members • Free

AI Automation Society

393.9k members • Free

🏛️ Coaching Academy

3.5k members • Free

The Great AI Shift

3.4k members • Free

The Iron Forge Brotherhood

29k members • Free

The Dr. Z Clinical

597 members • Free

🏠 Lower Taxes w/ Ryan

1.4k members • $1/year

38 contributions to 1099AnesthesiaAdvantage

6h •

The Cost of “I’ll Figure It Out Later”

A lot of CRNAs spend years planning patient care. We prepare for emergencies. We think through complications. We always have a backup plan. But when it comes to our own finances? Many of us say: “I’ll figure it out later.” Later turns into years. Years turn into missed opportunities. Retirement accounts never get opened. Tax strategies never get implemented. Contracts never get negotiated. And suddenly you’ve worked thousands of hours without maximizing the opportunities that were available all along. This isn’t about being perfect. It’s about taking one step today instead of waiting for the perfect time. What’s one financial move you wish you had made sooner in your career? 👇 I’d love to hear it. #CRNA #NurseAnesthetist #CRNALife #LocumCRNA #1099CRNA #FinancialFreedom #HealthcareProfessionals #AnesthesiaLife #CareerGrowth

0

0

7d •

True or False

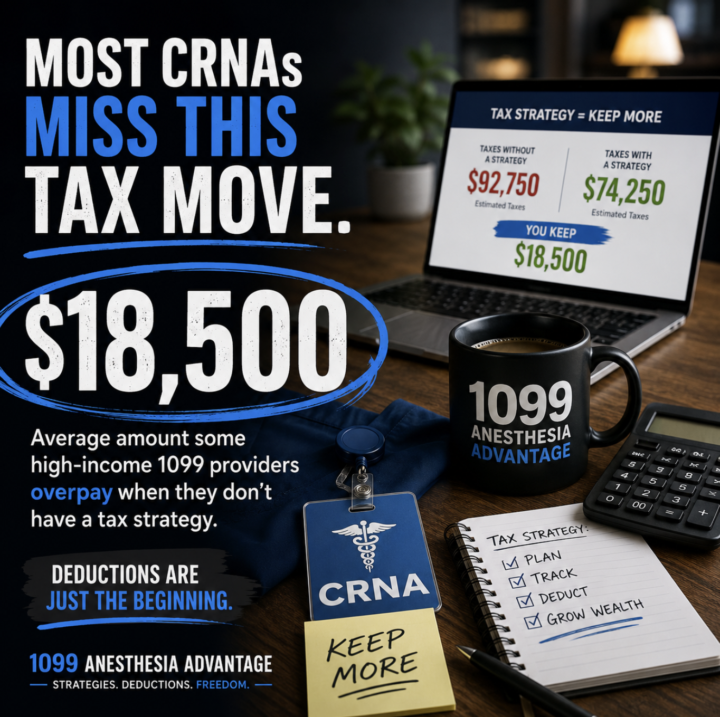

A CRNA making $300,000 can legally pay thousands less in taxes than another CRNA making the exact same income. Same profession. Same income. Different strategy. Most providers never learn the difference. What's the biggest tax mistake you've seen someone make? 👇

0

0

12d •

Introduce Yourself

Every week brings new members. Let's make sure you're known. Drop a comment below with: - Your credential (CRNA or MD) - Your state - Your current setup (W-2, already 1099, considering the switch) - One thing you want to fix or figure out in the next 6 months That's it. We'll reply, point you to the right tools, and if there are other members in your state or situation we'll tag them so you're not navigating alone. This is the post that makes the community not feel like complete strangers!

0 likes • 11d

@Bryan Taylor Glad to have you Bryan. THIS COMMUNITY is about you and everyone who was tired of getting bad info from the experts in the CRNA forums. And from the tax experts we trusted. Just let us know what your questions are and I will make sure you have the most accurate and up to date answers. Also let me know if you have suggestions on how to make our community better.

0 likes • 10d

@Bryan Taylor hey Brian can you tell us a little bit more about your blindsided story? I'd love to hear it and we all learn from each other's experiences.

10d •

5/28 Live Q+A with Rich

You've probably been hearing more about Trump Accounts lately. This video is a quick introduction to what they are, why they're generating so much discussion, and some of the basics you should know. If you're not familiar with them yet, take a look. We'll be releasing additional videos soon that go much deeper into the strategy, tax implications, and planning considerations surrounding these accounts. What questions do you have about Trump Accounts? Let us know in the comments.

0 likes • 10d

In this video, we take a closer look at how Trump Accounts may work, some of the planning considerations families should understand, and why the details matter when evaluating any long term savings strategy. This is part of our ongoing educational series on Trump Accounts. If you're just hearing about them, start with our introductory video. If you've already seen the basics, this deeper dive will help you better understand some of the questions and opportunities being discussed. More videos and educational content on this topic are coming soon. Have a question you'd like covered in a future video? Leave it in the comments below.

11d •

Trump accounts for your kids, the quick version (plus the catch)

Bunch of you have asked about these, so here's the fast breakdown. What they are: a new IRA for kids under 18 from last year's tax bill. Launches July 4, 2026. You can drop up to $5k a year per kid, and the kid does NOT need a job or any earned income to get one. Kids born 2025 to 2028 also get a free $1k from the government. Why they're worth it: you don't get a deduction going in, so that money's already been taxed. When the kid later converts it to a Roth, only the growth gets taxed, not your contributions. Do it right and they end up with a Roth that grows tax-free for 40+ years. The compounding on that is wild. The catch (this is the part that matters for us): everyone online says "just convert it at 0 to 12%." That only works if your kid is out from under the kiddie tax. A Roth conversion counts as unearned income, and the kiddie tax taxes a dependent kid's unearned income at YOUR rate, not theirs. It hits kids under 18, and full-time students under 24 who aren't supporting themselves. So if you convert your 19-year-old's account while you're sitting in a 35% bracket, that growth gets taxed at 35%, not 12%. The fix: don't rush the conversion. Let it grow, then convert in a year your kid is genuinely out of the kiddie tax (usually 24 or older, or sooner if they're self-supporting), and spread it across a couple of their low-income years to stay in the low brackets. There's no deadline to convert, so it's easy to time right. For the business owners: the law also lets your business kick in $2,500 of that $5k pre-tax. Looks good, but the rules are still proposed and whether it's actually tax-free for S-corp owners like us isn't nailed down yet. Don't bank on that piece. Bottom line: opening the account is the easy part. The timing of the conversion is what decides whether this is a home run or a tax bill. Click here if you would like to see some more free resources on this topic!

1

0

1-10 of 38