Activity

Mon

Wed

Fri

Sun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

What is this?

Less

More

Owned by Leny

DIY credit repair with an AI that reads your report and drafts the letters. No agencies. No BS

Memberships

AI SEO | Rank & Rent Lead Gen

2.8k members • Free

AI MVP Builders

2.8k members • Free

NextGen AI

35.9k members • Free

Clief Notes

35.4k members • Free

Hyliox

866 members • $3

Leadbase Free

12.5k members • Free

Klient Engine

1.7k members • Free

AI Automation Society

386.9k members • Free

Fix Your Credit

248 members • Free

22 contributions to DIY Credit Repair Academy

2d •

The $900 lesson nobody warns you about

Real talk for the community 👇 One of the most common stories I hear: "I paid a company $150/month for six months and my score didn't move." If that's you, I want you to know two things. One — it's not your fault. The process was deliberately invisible. You couldn't see which items were disputed, on what basis, or whether anyone followed up when a bureau stonewalled. Two — the actual mechanics aren't a secret. Disputing inaccurate items for investigation is a right you already have. The value isn't access to the work; it's knowing exactly which dispute, on what basis, in what order — and tracking every deadline so nothing slips. That's literally what CreditShield is built to do, and why members run it themselves for $29–79/mo instead of $150 with a blindfold on. If you haven't yet: run your free scan, then drop your biggest "where do I even start" question below and I'll point you to the right first move. 👇 (Reminder: this is a self-directed tool. Results vary, and we never promise to remove accurate items.)

0

0

6d •

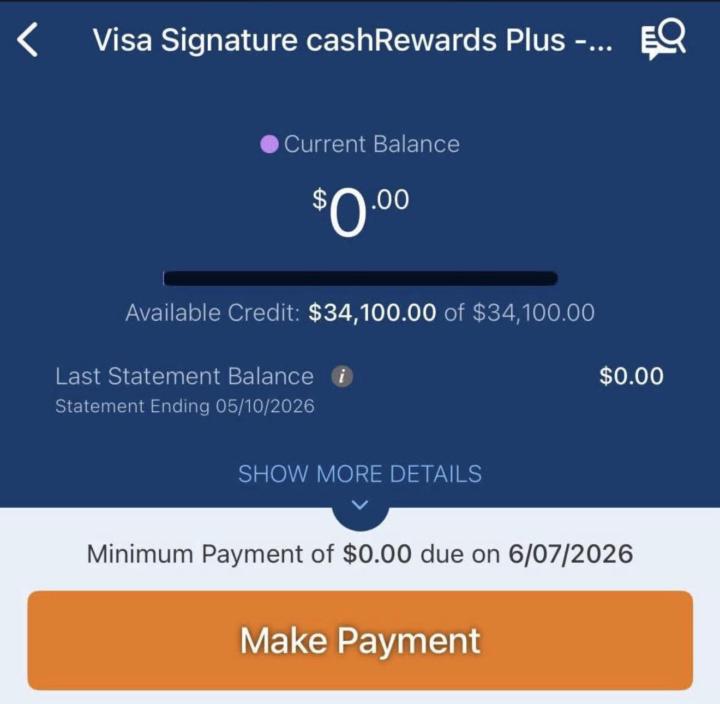

Quick thought for the community 👇

Most people don't realize this until it's already costing them: Good credit isn't about a number on a screen. It's about ACCESS. Access to capital. Access to opportunity. Access to the kind of decisions that build wealth instead of just survive the month. The screenshot above? That's not a flex. That's leverage sitting quietly, ready when it's needed. Here's the part I keep coming back to: The AVERAGE person uses credit to buy depreciating junk — shoes, the latest phone, furniture they don't need — and then wonders why they feel stuck. The SMART person uses credit to start businesses, acquire assets, fund income streams, and create leverage. Same tool. Completely different outcome. The difference? Strategy. And the willingness to actually invest in their own financial position instead of treating everything in life as a "bill." Think about it: People will finance a $40,000 car without blinking. A $1,500 phone? Easy. But hesitate to invest in the ONE thing every bank, landlord, lender, and insurance company actually looks at? That's the part that doesn't make sense. Here's the truth I want every member of this community to internalize: Good credit doesn't change your life because of the score. It changes your life because of what the score UNLOCKS. That's the entire game. For anyone who hasn't upgraded yet — Premium members get full access to Credit Shield Fortress at no extra cost, plus the advanced credit repair education that takes you from "just disputing" to actually understanding how to play the long game with your credit and your money. All of it for $47/month. No pressure. Just know it's there when you're ready to stop surviving and start building. Keep moving 🛡️

2

0

8d •

Si alguien me puede explicar, por favor 🙏

“Recibimos una solicitud reciente relacionada con su información de crédito que no parece haber sido enviada directamente por usted o autorizada por usted. Como medida de precaución, no hemos tomado ninguna acción sobre su supuesta solicitud. De acuerdo con la Ley Federal de Reporte Justo de Crédito (Fair Credit Reporting Act), si la integridad o exactitud de cualquier información contenida en el archivo de un consumidor en una compañía nacional de reportes de crédito es disputada por el consumidor y este notifica a la compañía directamente sobre dicha disputa, la compañía deberá reinvestigar sin costo alguno. Por lo tanto, usted puede disputar cualquier información incorrecta directamente con Experian de manera gratuita. Si usted cree que la información en su reporte de crédito personal es incorrecta o está incompleta, por favor llame al número 833-421-3400, o visite nuestro sitio web seguro para subir documentos en: [oai_citation:0‡experian.com](https://www.experian.com/dispute?utm_source=chatgpt.com)” En resumen, esta carta significa que Experian recibió una solicitud o disputa relacionada con su crédito, pero sospecharon que podría no haber sido autorizada por usted, así que detuvieron el proceso por seguridad. Ahora le están indicando cómo confirmar y enviar la disputa correctamente. Buenas tardes, me llegó esta carta, que me dice de esto?

1 like • 8d

¡Hola! 👋 No te preocupes, esa carta es muy común y la conocemos como "carta de verificación" o stall letter. ¿Qué significa realmente? Experian recibió tu disputa, pero sospecha que pudo haber sido enviada por un tercero (por ejemplo, una compañía de reparación de crédito) y no directamente por ti. Por eso pausaron el proceso como medida de seguridad. NO es un rechazo, ni significa que algo esté mal con tu disputa. La carta también te recuerda tu derecho bajo la Fair Credit Reporting Act (FCRA): puedes disputar información incorrecta gratis directamente con Experian. Eso ya lo sabes — solo te lo están reafirmando. ¿Qué debes hacer ahora? 1️⃣ Llama al 833-421-3400 o entra a experian.com/dispute 2️⃣ Confirma tu identidad (te pueden pedir tu ID, número de Seguro Social, comprobante de domicilio) 3️⃣ Confirma que SÍ autorizaste la disputa 4️⃣ Si te piden documentos, súbelos al portal seguro de Experian Una vez verificada tu identidad, Experian tiene 30 días por ley para investigar la disputa. 💡 Tip pro: Para evitar este tipo de cartas en el futuro, las disputas funcionan mejor cuando se envían por correo certificado, con tu firma original, copia de tu ID y comprobante de domicilio reciente (factura de luz, agua, etc.). Esto le quita a las agencias la excusa de "sospecha de tercero". ¿Tienes preguntas? Avísanos por aquí 👇

11d •

Quick Poll

What's the #1 thing hurting your credit right now? A) Collections B) Late payments C) High utilization D) Don't know yet — haven't pulled my report Let me know in the comments

1 like • 10d

@Talisha Bishop Good news on this one, Talisha — high utilization is the fastest thing you can fix on a credit report. Unlike a collection or late payment that sits there for 7 years, utilization updates every single month when your statement closes. A few moves that actually work: Pay your balance down before your statement closing date — not the due date. Most people pay on the due date but the bureau already reported your balance at statement close. Timing matters. If you can't pay it all down, call your card issuer and ask for a credit limit increase. Same balance, higher limit = lower utilization instantly. Takes 5 minutes and a lot of issuers will do it without a hard pull if you've been a customer for a while. The target is under 10% per card if you want to see a real score jump. Under 30% helps but under 10% is where the score moves significantly. How many cards are we talking and are they all maxed or is it mainly one?

1 like • 9d

@Sharon McElroy “All of the above” is actually the most common starting position — not the unusual one. The trap is trying to fix everything at the same time. The sequencing that actually works: 1. Stop the bleeding first — get every account current. New late payments hurt your score more than old ones, and they’re the #1 dealbreaker for auto financing. 2. Clean the file — disputes on collections, charge-offs, and any inaccuracies. 3. Optimize what’s reporting — utilization & statement-date timing (covered in the comment above). 4. Build — new tradelines, authorized user strategy, account age. Most people skip step 1 and wonder why disputes don’t move their score. The bureaus will clean up old items while new lates keep showing up — net zero movement. Given your vehicle-financing goal, steps 1 and 3 are the most direct unlocks. Bring your actual report to the next Q&A and we’ll sequence the real moves on your file. — Leny

1-10 of 22

@leonard-pearson-6977

I built CreditShield to find errors on your credit report. Join the community and learn to fix them. https://www.skool.com/creditshield-academy/about

Active 2h ago

Joined Mar 28, 2026

Palatka, FL 32177

Powered by