Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Owned by Donald

Learn the craft of buying profitable businesses through real deal breakdowns, acquisition frameworks, and operator thinking.

Memberships

Carl's Golden Ticket Auction

704 members • Free

Closers.io - Remote Sales Reps

15.5k members • Free

The AI Advantage

126.7k members • Free

Skoolers

164.5k members • Free

97 contributions to Acquisition Operator Network

2h •

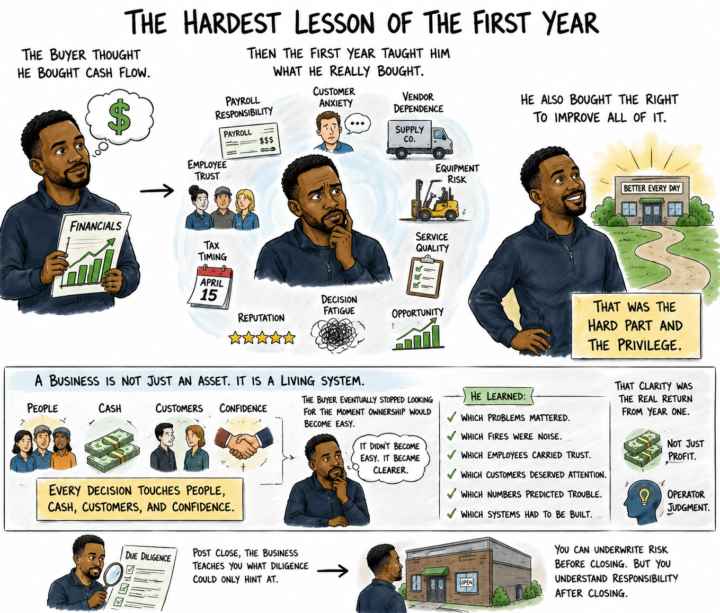

The Hardest Lesson Of The First Year

When the buyer closed on the business, he believed he had purchased one thing above all else. Cash flow. The financial statements were solid. The projections made sense. The financing was in place, and he was excited about the opportunities that lay ahead. It didn't take long to realize he had purchased something far more significant. He had bought the responsibility of making payroll every two weeks. He had inherited anxious customers who wanted reassurance, vendors the business depended on, aging equipment that didn't always cooperate, employees who were quietly deciding whether they could trust their new owner, tax obligations that never seemed to arrive at a convenient time, and a reputation that could be strengthened or damaged by the decisions he made each day. He had also purchased something else. The opportunity to improve all of it. That became both the greatest challenge and the greatest privilege of ownership. Over time, the buyer stopped thinking of the business as an asset and started seeing it for what it really was. A living system. Every decision influenced something else. A change in operations affected employees. Better communication improved customer confidence. Investments in maintenance reduced future surprises. Stronger systems made better financial decisions possible. Nothing existed in isolation. At first, he kept waiting for the moment when ownership would finally become easy. It never did. What changed wasn't the difficulty. It was his perspective. As the months passed, he became better at recognizing which problems truly deserved his attention and which were simply part of running a business. He learned which employees carried the trust of the organization, which customers represented long term value, which numbers signaled trouble before it became visible, and which systems needed to be built if the company was going to grow beyond its current limits. Looking back, he realized the greatest return from his first year wasn't found on the income statement.

0

0

3d •

Poll: Would You Find Value In Watching Live Deal Reviews?

One of the biggest gaps between learning acquisitions and actually buying a business is seeing how experienced operators think through real situations. Every acquisition is different. A seller changes their mind. A lender asks unexpected questions. Due diligence uncovers new risks. The original deal structure no longer works. That's where judgment is developed. I'm considering opening a limited number of live sessions where members can observe actual deals being evaluated by our community. We'd walk through real financials, discuss valuation, evaluate risk, explore financing options, review negotiation strategies, and talk through the decisions being made along the way. These wouldn't be hypothetical case studies. They would be real acquisition opportunities, discussed in real time, with the goal of helping members understand not only *what* decisions are made, but why they're made. Before putting something like this together, I'd love your feedback. Would you participate in live deal review sessions?

Poll

Cast your vote

0

0

6d •

The Exit He Started Building Before He Wanted To Sell

When the buyer acquired the business, selling it was the last thing on his mind. He had spent years searching for the right opportunity, and now his focus was on building, improving, and growing what he had just purchased. Yet only six months after closing, he began preparing the company as though a sophisticated buyer might review it at any moment. Not because he wanted to sell. Because he realized the discipline required to build an attractive business was the same discipline required to build a better one. He started with the fundamentals. Monthly financial statements became more consistent and easier to understand. Add-backs were documented clearly instead of relying on memory. Operating processes were written down, customer concentration was tracked, vendor contracts were organized, employee responsibilities were clarified, equipment maintenance was logged, and key performance indicators were reviewed regularly. Even management meetings began producing written notes and action items. At first, the team questioned why so much documentation was necessary. They weren't planning to sell the company, so it felt like unnecessary work. Over time, however, the benefits became impossible to ignore. Decision-making became faster because reliable information was readily available. Conversations with lenders became more productive because the business could answer questions with confidence. New employees were onboarded more quickly, reporting became cleaner, and planning for future growth required far less guesswork. The buyer eventually realized that exit readiness had very little to do with exiting. It was about building a business that was understandable, transferable, and financeable. In many ways, the characteristics that make a company attractive to a future buyer are the very same characteristics that make it a better business to own today. Looking back, one lesson stood above the rest. Enterprise value isn't created only through higher revenue or larger profits.

7d •

The Moment The Business Felt Like His

The buyer assumed ownership would feel real the moment the deal closed. He expected the excitement of signing the documents and receiving the keys to mark the beginning of a new chapter. It didn't. A few weeks later, he thought perhaps it would happen after processing the first payroll. When that came and went, he still felt more like a caretaker than an owner. Then came the first major customer win, and while it gave him confidence, something still felt missing. The moment finally arrived six months later during an ordinary team meeting. An employee raised a question and asked, "How do we want to handle this going forward?" The buyer immediately noticed what hadn't been said. The employee didn't ask, "How did the seller handle this?" Nor did they ask, "What would the old owner do?" Instead, they looked to the future. That subtle change in language meant more to the buyer than the purchase agreement ever had. It signaled that the team had stopped filtering every decision through the previous owner. Without anyone announcing it, the business had begun developing a new operating identity. The buyer hadn't forced that moment. He had earned it. Over the previous six months, he had kept his promises, resisted the temptation to change everything at once, solved problems without assigning blame, protected the parts of the business that already worked, improved the areas that didn't, and consistently showed up when ownership was inconvenient. Looking back, he realized something important. Legal ownership transfers at closing. Psychological ownership is earned through repeated proof. One of the most meaningful milestones after an acquisition isn't found in a closing binder or a financial report. It happens quietly, when the people inside the business stop treating the new owner as a temporary disruption and begin trusting them as the person responsible for what comes next.

8d •

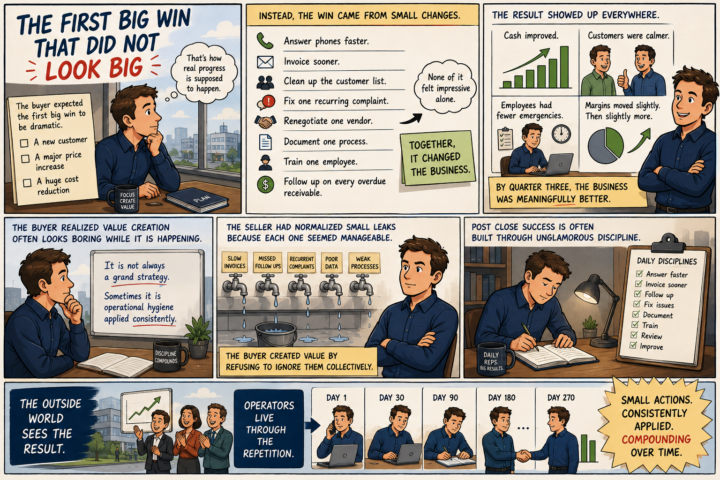

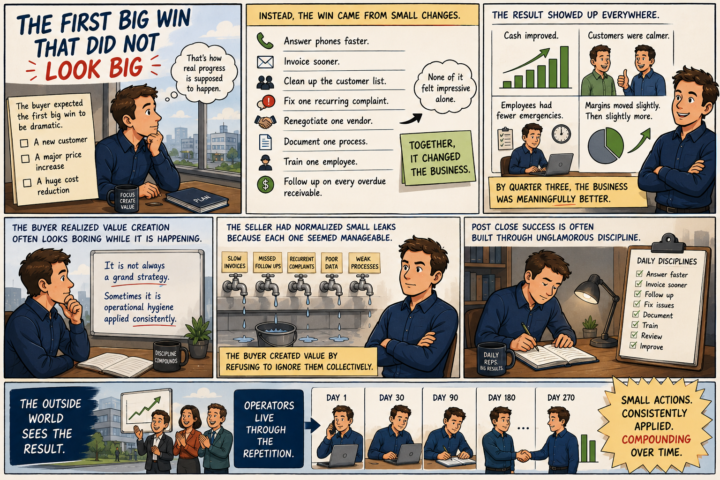

The First Big Win That Didn't Look Big

When the buyer took over the business, he imagined his first major win would be obvious. He pictured landing a large new customer, negotiating a meaningful price increase, or finding a way to eliminate a major expense. Those were the kinds of victories he had envisioned while searching for the right acquisition. Instead, the first real breakthrough came from a collection of changes that barely seemed worth celebrating. The phones were answered a little faster. Invoices went out the same day instead of sitting for a week. The customer database was cleaned up, recurring complaints were finally addressed, and a vendor contract that had quietly become expensive was renegotiated. An important operating process was documented for the first time, an employee received additional training, and every overdue receivable was followed up consistently. None of those improvements would have impressed anyone on their own. If you looked at the business after any single change, you probably wouldn't have noticed much difference. But as the weeks passed, the cumulative effect became impossible to ignore. Cash flow improved because invoices were collected sooner. Employees spent less time putting out preventable fires. Customers became easier to serve because the same problems stopped repeating themselves. Margins improved a little at first, and then a little more. By the third quarter, the business looked noticeably healthier than it had on the day he bought it. That's when the buyer realized something that has stayed with him ever since. Value creation rarely feels exciting while it's happening. Most of the work is repetitive. It doesn't generate headlines, and it certainly doesn't make for dramatic stories. It's simply the result of applying operational discipline day after day, long after the excitement of closing has worn off. The previous owner had learned to live with dozens of small inefficiencies because each one seemed insignificant in isolation. The buyer created value by refusing to view them that way. He understood that while each leak was small, together they were quietly holding the business back.

1-10 of 97

Active 2h ago

Joined Mar 1, 2026