Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Owned by Rebecca

Go from 'bad with money' to proud of your progress! Build better habits, talk money, upgrade your money mindset, heal your money story (shame-free!).

Memberships

Start a Business with No Money

487 members • Free

Focused Founders™

615 members • Free

Build Your Online Business

1.5k members • $9/month

💖 Soul-First CEO LaB ⭐

35 members • Free

REVENUE REVOLUTION

10.4k members • Free

The Art Of Going Live

236 members • $35/month

Your First $5k Club w/ARLAN

32.6k members • Free

BYOB: $25K BLUEPRINT™

40 members • $1,111/month

Skooly: Tools for Skool

251 members • $9/month

19 contributions to Financial Clarity Club

Jun 1 •

Paying Early Beats Paying More on Simple Daily Interest Car Loans

Are you a car owner? Have you been fighting with your car note and watching the loan hoover at it's balance for what feels like forever? For years I paid "on time" and "over-payment" just to watch everything go "nowhere" (right to interest) In today's video I show you how not only did I lower my car payment, lowered my daily interest, AND got my loan to budget by just paying the note EARLY. Do you pay your car note early? On time? If you are multi-car owner like myself this hack will save you a lot! This information is for educational and illustrative purposes only and does not constitute professional financial, tax, or legal advice. Every loan agreement is unique, and you should review your specific contract or consult with a qualified financial advisor before making decisions regarding your debt strategy. I am showing you my strategy so you can see if a strategy like this can work for you.

🔥

1 like • Jun 1

Yes! Great tip

🔥

1 like • Jun 1

@Lees Garcia

May 21 •

A Gift for You 🎁

I have a consultation call tomorrow focusing on business names and lowering risk for the best chance of funding. I put together a new module inside of the credit academy, and updated the business name generator with my new found knowledge! You can try the updated generator here and see how your business fares against underwriting guidelines. https://app.gohighlevel.com/v2/preview/M1Bv1PnCX8UTmm7Q6CXf?notrack=true Visit the Course Classroom: https://www.skool.com/skool-of-financial-literacy/classroom/db9e1ad6?md=17ddc7a45a864b929aae0c8a42ea772e Let me know what you think!

🔥

1 like • May 21

oooo so fancy

🔥

1 like • May 21

@Lees Garcia Lol I wish you luck on that.

May 17 •

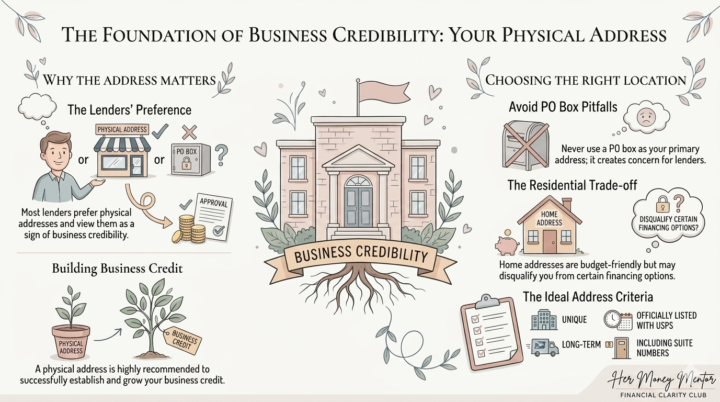

Is Your Business Address Secretly Sabotaging Your Funding?

Did you know that something as simple as your mailing address could be the difference between an approval and a decline? Many entrepreneurs believe a PO Box is sufficient, but in the eyes of a lender, it can be a major red flag. While a physical address isn’t strictly required to start building credit, it is a powerful tool to increase your business’s credibility. Lenders often feel concerned when a PO Box is the only address on file, and they prefer to see an actual physical location where your business operates. But wait—before you just use your home office, there are a few things you need to consider: - The Residential Risk: Using a residential address is a common way to save on costs, but you should be aware that some lenders may not be interested in financing a home-based business. - The USPS Standard: Your address needs to be recognized as an actual physical location by the United States Postal Service, including any applicable suite numbers. - The "Shared" Trap: Using an address that is shared with other businesses can be dangerous. It can lead to misreporting your payment data, which could damage your credit profile before you even get started. Your business address should be a long-term foundation for your brand, not just a temporary fix. Are you sure yours meets the standard lenders are looking for? Ready to build a foundation that lenders can’t ignore? 🚀 Join our NEW lesson in the Corporate Credit Academy to master the art of business credibility and ensure your business is positioned for maximum funding. Explore Where you are right now > https://tinyurl.com/fccaddress Visit The Classroom > https://www.skool.com/skool-of-financial-literacy/classroom/db9e1ad6?md=a8db78ad75184c8db3a437e66318d492

🔥

0 likes • May 18

@Lees Garcia Yeah so hoping once I get it locked down, (It is currently being renovated) I can start the paperwork process to be legit and googleable I guess.

🔥

1 like • May 18

@Lees Garcia I have a few things I want to trademark haha but was told to wait until I had the business first and not to register for it under just me.

May 14 •

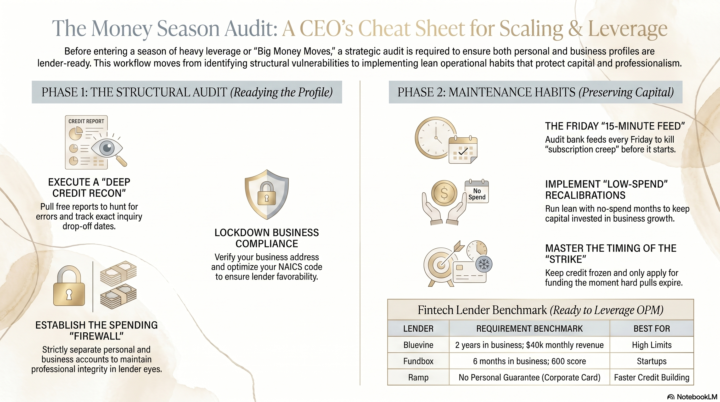

Post-Tax Strategy: Big Money Moves 📈

Now that tax season is behind us, I’m shifting gears. I'm preparing for Big Money Moves, this is usually a time where I sell or purchase a vehicle or property, I just haven't quite decided the direction yet. I wanted to share how I’m auditing my own setup to prepare for more funding and better leverage: - I’m pulling my report from annualcreditreport.com (it’s 100% free). I’m not just glancing at the score. I’m hunting for errors and tracking exactly when old inquiries drop off. This tells me exactly when I’m ready to strike for that next $0% interest card or commercial property. I believe my last inquiry falls off next week! In the meantime, the credit stays FROZEN to avoid any unplanned credit pulls. - I’m auditing every single expense. If I’m not using a subscription, it’s gone. Planning a "low-spend" month helps me keep the capital where it belongs: invested back into my business or paying me first. If I don't recalibrate with a no spend month before getting access to capital I could easily lose track of "expense" creep as it pertains to my business. Running lean is my priority! - I’m currently restructuring to ensure I’m seen favorably by lenders. Unfortunately, my old business address went "bad" (it happens), so I’m locking in a new, compliant one to keep my profile solid. Did you know that when this happens your bank could shut you down? I had a horrifying moment where I woke up to a zero bank account, and it was all thanks to my address getting flagged on a short notice. My goal right now is simple: Map out whether I need to Restructure debt, use OPM (Other People’s Money), or leverage personal credit to scale. Do you have a big money move coming up? How are you preparing yourself and your business?

🔥

1 like • May 15

@Lees Garcia Haha I have had it for a while.

🔥

0 likes • May 15

@Lees Garcia Random question. Are you using a registered Agent?

Apr 26 •

Add to Cart

What are you adding to cart this weekend? I found this on an influencer site (@jodie.thedesigntwins) and thought it was the perfect folder for the untangle your money challenge! What do you think? I added to cart immediately! https://amzn.to/4mU93l5 What have you added to cart lately?

🔥

1 like • Apr 26

Oooo that is super interesting. Time to check out reviews

1-10 of 19

🔥

@debttale

I help people unmute their money, build confidence with their money decisions, and feel safe talking finances with anyone.

Active 6h ago

Joined Jan 11, 2026

INFP

Clarksville, Tennessee

Powered by