Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Memberships

LetsGetFunded PRO

664 members • $63/m

LetsGetFunded Inner Circle

1.7k members • $63/month

LetsGetFunded Starter (Free)

18.3k members • Free

53 contributions to LetsGetFunded Starter (Free)

4d •

Avoiding Personal Guarantees for Business Owners

One purpose for establishing business credit is to obtain credit lines without providing a personal guarantee (PG) and not having a personal credit check. Many vendor accounts can be obtained via EIN only with no personal credit checks or personal guarantees that can help your cash flow. The more of these you can obtain the better it will be for your business. All business owners should be doing this. NET 30 and revolving accounts help with cash flow. But it’s a fallacy to think every credit line you ever obtain will require no personal credit check or personal guarantee. From a lender’s perspective, why would anyone give you thousands if not hundreds of thousands of dollars with no guarantee of repayment? That is not a good business model. Lenders aren't in business to make our dreams come true. They loan money with interest to make more money than lend it out again. That is their business model. Money is their product. Lenders will share in the risk of loaning money to you but they won't take on 100% of the risk. If you are not willing to take a chance on you and your business, why should anyone else? For most of us, your personal credit is going to be looked at and you WILL provide a personal guarantee as the business owner. But if you do things the right way, you WILL obtain those cash credit lines attached to your entity and it's EIN#. The credit lines WILL NOT show up on your personal credit reports. When you use these credit lines, they WILL NOT affect your personal credit. That is a huge advantage. I tell all my clients don’t be afraid of providing a personal guarantee (PG). By all means try to limit the number of times you provide a personal guarantee, but don’t be afraid to provide it. If the capital you can acquire by providing the lenders required personal guarantee moves your business forward, why wouldn’t you provide it? Just be sure it will not show up on your personal credit report, and only report to the business credit bureaus.

5d •

Do You Have Congruent, Accurate and Verifiable Business Information?

Do you know what your business looks like in a simple online search? Is your business easily found in an online search? It better be or that is a RED flag to lenders. Is all the information you see congruent? You want to have accurate and congruent business information starting from the Secretary of State website, your website, business bureau files, and on online directories. You want to use that same information on all credit applications. Do you know what business address the Secretary of State has for your business? Check here: https://www.secstates.com/ Is this the address you are placing on credit applications? Is this the address business bureaus like Dun & Bradstreet have for you? Is this the address you use on your website and marketing pieces? It is vitally important to be easily found and have all the information the same. You don’t want to confuse lenders that are verifying the business information you place on your credit application. Make sure you are “funding” compliant. Join me each Thursday at 2pm PST/5pm EST for my “Path to Capital” presentation. If you are not an Inner Circle Member yet why not? If not, join us now, https://www.skool.com/100k/about?ref=388020e1932a41bc89d72f691110f1ec Learn what it takes to be fundable.

2

0

9d •

The Three Major Business Credit Bureaus

Before we get into who are the three major credit bureaus let’s get this one fact straight. Business credit bureaus are not our friends. They report good, bad, and ugly information on us. Business credit is not covered under the Fair Credit Reporting Act (FCRA). As a result, business credit reports are not private. Anyone can view any business credit report, although there is often a charge for this information. So, who are the “big three” business credit bureaus? Dun & Bradstreet (D&B) Of the big three, D&B is the only credit bureau that focuses exclusively on business credit. They report primarily on how a business interacts with vendors and other suppliers, which is why potential suppliers often look at your D&B reports before they offer your business trade credit. In addition to business-to-business data submitted by suppliers, D&B also looks at public records, industry data and other historical data in your D&B profile to compile their credit scores, of which the PAYDEX Score is the best-known. PAYDEX Score: The 100-point PAYDEX score reflects how reliably you’ve paid your bills and kept your financial obligations to vendors and suppliers that report to D&B. Unfortunately, if you are current with suppliers who don’t report to D&B, that information won’t be included when calculating your PAYDEX score. Because the PAYDEX score is so important, you should encourage current vendors that don’t report your credit history to D&B to do so. You may even want to switch to vendors who do. Other D&B business credit scores include: - Delinquency Predictor Score: This score measures whether or not a business is likely to pay their bills late or go bankrupt over the next 12 months. - Failure Score: This score is designed to predict the possibility that a company will seek legal relief from creditors or go out of business and leave creditors unpaid in the next 12 months. - Supplier Evaluation Risk Rating: This rating predicts the likelihood that a business might stop delivering its goods and services over the next 12 months. - D&B Rating: This rating relies upon company financial statements and other public information to develop an overall rating for a business’s creditworthiness. Making sure that your D&B profile includes accurate, up-to-date financial statements can greatly improve your D&B rating. - Credit Limit Recommendation: Banks and creditors may look at this recommendation, which is based on a business’s size, industry and payment history.

6

0

10d •

Are You Ready for Your $150K Cash Credit Line?

I talk with a lot of real estate investors and start-ups looking for capital. One major issue I run into is the lack of planning on how to use the credit lines. The fact is if you work with Evan and his team, you WILL obtain these credit lines. They know how to position YOU to obtain these credit lines if you follow their instructions. While you are working on your personal credit, entity structure, and business credit, be sure you are ready with a solid plan to utilize the credit lines to produce revenue. This is where I see many people fail. They are not ready to implement the credit lines to produce revenue. Many of my real estate investors have not even decided if they are flippers or long-term rental holders. They have not learned anything about the market they plan on investing in. They have not joined a local real estate club (https://reiclub.com/real-estate-clubs/) to find partners, mentors, contractors, title companies, real estate agents, or lenders. They just want the Benjamin’s ($$$$). Many of my start-ups are the same. They want the money……………then they will decide what business they will conduct or buy an existing business. Say what? I am always baffled by this. Have a plan in place to immediately implement that will generate revenue once you get the credit lines you are seeking. Otherwise, what is the point of having access to capital? Evan and his team can get you there—the only question left is: Are you ready? Join the Inner Circle Now – Lets go! https://www.skool.com/100k/about?ref=388020e1932a41bc89d72f691110f1ec

4

0

11d •

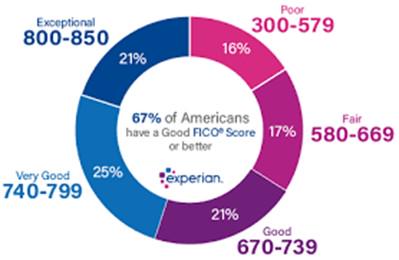

Do You Know You Have Many Different FICO Credit Scores?

Did you know there are multiple versions of FICO scoring models currently being used? Did you know you have many different credit scores? One for credit cards, one for mortgages, one for auto loans, etc. The most popular credit scoring model currently used most is FICO Model 8. Do you know what your FICO score 8 is with Experian, TransUnion, and Equifax credit bureaus? Your credit score is not static. It changes constantly. It changes as more information is updated to your file. The credit bureaus do not receive the same reporting data as not all lenders report to all three credit bureaus. Your credit score is a snapshot of your credit data at the moment in time it is viewed. Your credit score is one of the most important numbers in your personal financial life. When you apply for a personal loan or business loan of any kind, lenders will reference your credit score to get a feel for how big a credit risk you might be. A higher score = less of a risk. Lower risk results in better rates and higher credit line offers. Credit bureaus are not our friends. They report good, bad, and ugly information on us. They make money by selling your credit reports to banks, credit unions, credit card companies, vendors, and other lenders. You must monitor your credit reports and credit scores. If you are not doing so today, make it a priority. https://www.smartcredit.com/?PID=73743

4

0

1-10 of 53

@dan-ollman-4226

20 Years Experience as a Business Credit and Funding Coach. Help business owners establish funding tied to their entity and EIN#, not your SSN.

Active 37m ago

Joined Nov 28, 2025

Powered by