Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Owned by Angela

Build your business like a real “CEO” get official, get organized, and get fundable with clear steps and real support. Join the “No Hustle Zone”

Memberships

The eRide Repair Academy

246 members • Free

E-bike and Scooter Repairs

4 members • $5/month

6 contributions to Financial Clarity Club

May 2 •

Gas Cards Under Your Business

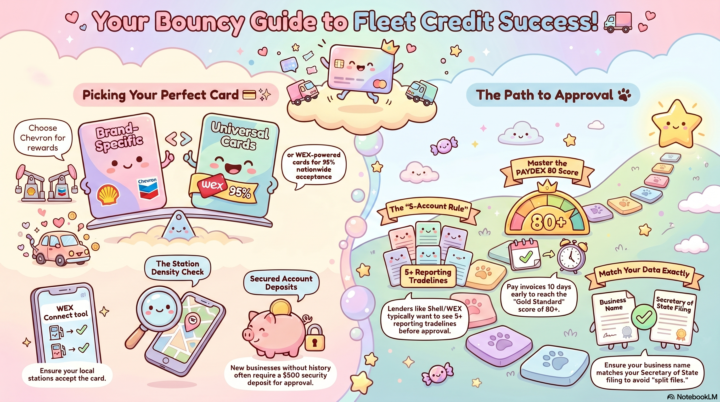

I am starting to work on building out a credit strategy for businesses, and I want to provide a specific update on managing a fleet credit strategy for those thinking about it. I recently conducted a deep-dive audit with the underwriting team at WEX, which is the primary underwriter for major brands like Shell, ExxonMobil, BP, 7-Eleven, and the Phillips 66 family (Conoco/76). Here are the key takeaways to ensure your next application is successful: There are two ways to approach fuel credit. Your choice should be based on your business’s actual footprint: - Brand-Specific Cards: (e.g., a "Chevron" or "Shell" card). These often offer specific rebates or incentives but are best if your fleet operates near those specific stations. - Universal Cards: These are powered by the WEX network and are accepted at over 95% of retail fuel locations nationwide. If you need flexibility, this is the route to take. If your business is still in the "building" phase or does not yet have a robust reporting history with all three bureaus, it is highly standard for the credit department to request a $500 security deposit for a secured account. - Before applying, they recommend checking your local zip code for station density. You can use the WEX Connect tool to see which stations near you accept these cards to ensure the line of credit is actually useful for your daily operations. Want to learn more about it? Check out the Corporate Credit Academy

3 likes • May 2

@Lees Garcia I try and stay away from funding fun stuff 🤪 because my community people get excited and try and skip the basics but often times won’t make sure their ein and llc address matches and still using their cell phone number as their business point of contact. But I’m re doing somethings this month to engage movement

1 like • May 2

@Lees Garcia lol yes it all needed for sure. I want to create my ideal client. Over the years I have worked with people that I wished I had of said no too just because they thought they were ready but it wasn’t the season for them. So I almost purposely detour you so much that you second guess “am I really ready lol” 🤣

Mar 24 •

How are you feeling about Ai?

Many people are complaining that Ai is making people dumb because they "aren't thinking." But I want to challenge that. What if they are rewiring their brains to think differently. We all know that effort doesn't equal money and you can work smarter instead of working harder. The mind can work exactly the same way. Instead of taking up capacity to look at our calendar and "power up" to decode the day we need to plan, we can free up space and let our Ai help us with it. We use our brain power for more elaborate and aligned tasks and begin to process things much differently. Maybe I am wrong, but the better I get at Ai, the more confident I feel about my ability to think through problems, those problems just look different now. 🤔 I'm curious to know how you feel about Ai + personal finance... do tell...

1 like • Mar 24

@Cleveland Sparrow III

1 like • Mar 24

@Justin Saffel these are things that we forget as a business owner evolution will happen with or without you.

Jan 22 •

Tomorrow's Co-Working

Hey Club Members! Tomorrow Co-Working Session Agenda -Consolidating the rest of 2025 -Paying Yourself With a "New" Business -Updating our January Expenses It will be co-working, so you do not have to have finished this particular dashboard. If you are wanting to catch up with your own systems in good company, hop in and we can work through financial clarity together. Event posted on the Calendar! 📆 Friday 10AM EST.

Poll

3 members have voted

2 likes • Jan 22

@Lees Garcia I know right we’re going to have to hope on a call

1 like • Jan 22

@Rebecca Bautista hi friend. I need to post my referral links so I can make sure I spread the wealth and testimonies of good people I have meet on skool…. I’m doing business all wrong 😑

Jan 6 •

Your money habits aren't going to fix themselves. (Hack it with Ai)

Here is the thing I really want you to hear: Personal habits always spill over into business habits. If you can’t prove your income to yourself, you’ll never be able to prove it to a lender. The good news? With the help of Ai, your role just got an upgrade. You are no longer the person who manually types numbers into a spreadsheet for four hours, or the person that is putting off logging into their account because they are scared of what they will find. Now, it’s a job for Ai and you are a System Supervisor. Today on the channel I shared Why You're Missing Wealth Opportunities and I also wanted to put together some Homework for Friday and demo what Step 3 Looks Like. I did this for myself, and again for "Sarah," and the exercise took about 30 minutes each time. 🔔 Set aside 30 minutes to input your data into the account tracker by Friday Demo: Gathering Sarah's Data with Ai As promised: Sarah's Account Tracker

1 like • Jan 6

This was a good video thanks

Dec '25 •

Untangle Your Messy Money Challenge Poll

Hello Members I am thinking of structuring the challenge in a very easy to follow way. Providing two simple, powerful measurements to track your progress and keep you engaged: 1. Did You Show Up? 2. See how your progress stacks up against others. A little friendly competition is great motivation! The Question for You: What area you'd be most interested in tackling first in this challenge: - Option A: The Wealth Folder Overhaul 🗄️ (Organizing foundational categories like insurance policies, household documents, taxes, etc.) - Option B: Personal Finance Deep Dive 💰 (Focusing on active financial management tools like your balance sheet, budget sheet, cash flow tracking, etc.) Comment below with A or B to tell us where you want to start! Let's conquer the financial habits that lead to success!

Poll

2 members have voted

1 like • Dec '25

I think both would be a great things to tackle but gathering al those documents would be bigger for me

1 like • Dec '25

@Lees Garcia I do excel but want to use notions more but not sure 🤔 if it’s the season to implement it…..

1-6 of 6

@angie

I lost $500k so you don't have to. I teach founders how to build a bulletproof foundation from day one. The goal is peace of mind, not panic.

Active 8h ago

Joined Nov 20, 2025

ATL, Georgia, USA

Powered by