Activity

Mon

Wed

Fri

Sun

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

What is this?

Less

More

Owned by Deji

The #1 System & Blueprint to build your credit, structure your business, and get access to OPM to grow or start your biz & investments 💰🚀

The #1 System & Blueprint to build your credit, structure your business, and get access to OPM to grow or start your biz & investments 💰🚀

Memberships

Business Credit Accelerator

1.3k members • $49/month

Financial Management Academy

84 members • Free

Skoolers

164.1k members • Free

OPM Mastery Funding

3.5k members • Free

212 contributions to FundFlow Mastery

11d •

The Funding Stack: How to Layer 0% Business Credit Cards to Access $50K–$150K in Capital

Many business owners think they need one large loan to fund their growth. In reality, the most effective strategy is often building a funding stack—combining multiple 0% introductory APR business credit cards to maximize available capital. A well-structured funding stack can help qualified borrowers access $50,000 to $150,000+ in available credit, depending on factors such as: - Personal credit profile - Income - Existing debt and utilization - Business structure and financial strength - Approval criteria of each lender Here's how it works: ✅ Apply with multiple lenders using a strategic sequence—not all at once. ✅ Mix issuers to avoid internal lending limits and increase total approvals. ✅ Take advantage of 0% introductory APR offers to finance growth without immediate interest charges (for the promotional period). ✅ Use the capital strategically for inventory, marketing, payroll, equipment, or business expansion—not unnecessary expenses. The key isn't simply applying for more cards—it's applying in the right order and understanding each lender's underwriting guidelines. A poorly planned approach can lead to unnecessary denials or lower approval amounts. A properly executed funding stack helps preserve cash flow while giving your business access to flexible, low-cost capital during critical growth phases. Remember: Results vary. Not every applicant will qualify for $50K–$150K. Funding amounts depend on your individual credit and financial profile, and responsible repayment is essential to maintaining strong credit. This is why strategy matters just as much as your credit score.

0

0

18d •

🚀 FFM WINS OF THE WEEK 💎

Real results. Real execution. 📈 Another incredible client win! ✅ Credit scores increased from the 490s to 657 (+85 points) ✅ Reduced 11 negative accounts down to just 5 ✅ Removed 28 hard inquiries — from 31 down to just 3 remaining ✅ Multiple negative items successfully removed ✅ We're still actively disputing the remaining accounts to keep building momentum This is proof that credit repair is a process—not an overnight fix. Every deleted inquiry, every removed negative account, and every score increase brings our clients one step closer to achieving their financial goals. This is what happens when you: 👉 Follow and Join FundFlow Mastery 👉 Stay consistent through the process 👉 Execute step-by-step (no shortcuts) If you're just getting started, let this be your proof that the process works. Results come from consistency, strategy, and trusting the process. We're not done yet. With only 5 negative accounts and 3 hard inquiries remaining, we're continuing to push for even better results. Your turn is coming. Stay locked in. 💪🏾 Drop a 🔥 if you're next up!

0

0

23d •

Why Your Credit Age Matters More Than People Think

Most people focus on their credit score, inquiries, and utilization—but credit age is one of the most overlooked factors in building a strong credit profile. Your credit age refers to: ✅ The age of your oldest account ✅ The average age of all your accounts Lenders view longer credit history as a sign of stability and responsible credit management. That's why someone with a lower utilization and a 10-year credit history may be viewed more favorably than someone with the same profile but only 1-2 years of credit history. A few mistakes that can hurt your credit age: ❌ Closing old accounts unnecessarily ❌ Opening multiple new accounts at once ❌ Constantly replacing older tradelines with newer ones The key is building credit strategically—not just adding accounts, but maintaining strong, seasoned accounts over time. Remember: Strong credit isn't built overnight. The longer you manage credit responsibly, the more valuable your profile becomes to lenders. 👇 Have questions about your credit profile? Drop them below and let's discuss!

0

0

29d •

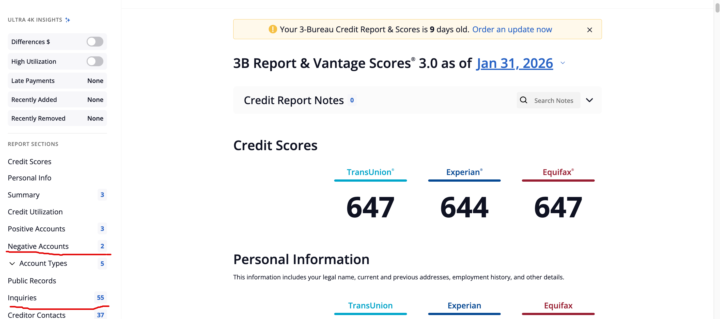

🚀 CLIENT WIN SPOTLIGHT 🚀

Back in January, this client came to us with: 📊 Credit Score: 647 ❌ 2 Negative Accounts 📌 55 Inquiries Fast forward to today: ✅ Credit Score: 672 (+25 Points) ✅ Negative Accounts Reduced to 1 Inquiries Reduced from 55 to 27 This is a perfect example of how credit repair is a process, not an overnight event. Every deletion, every inquiry removal, and every score increase brings our client closer to their financial goals. The best part? We're not done yet. 💪 Our team is continuing to work diligently to remove the remaining negative account and drive those inquiries down even further. Every profile is different, but consistent action and the right strategy produce results. Congratulations to our client on the progress so far! 🎉 Your credit journey doesn't have to stay where it started. Small wins compound into major transformations. #CreditRepair #CreditWins #FinancialFreedom #CreditScore #CreditTransformation #FFMWins

0

0

Jun 15 •

0% Interest Windows — How to Deploy Capital Before It Expires 💳⏳

A 0% interest offer is more than just free financing, it’s a strategic opportunity to put capital to work. The key is using that window to acquire assets, generate revenue, or improve cash flow before the promotional period ends. ✅ Invest in income-producing activities Fund marketing campaigns with measurable ROI ✅ Purchase equipment or software that increases efficiency ✅ Consolidate higher-interest debt when appropriate ✅ Maintain a repayment plan before the 0% period expires The biggest mistake? Treating a 0% offer like free money instead of a temporary tool. Smart entrepreneurs use leverage to create returns. The goal isn't to carry debt, it's to create more value than the cost of capital before the clock runs out. Question: If you had access to a $25,000 0% interest line today, where would you deploy it first? COMMENT YOUR ANSWERS BELOW. 👇 📈 #FundingStrategy #BusinessCredit #LeverageSmartly

0

0

1-10 of 212

@deji-hambolu-6784

Deji helps business owners secure funding to grow their business and create passive income through real estate

Active 2d ago

Joined Oct 18, 2024

Powered by